Modern countries need ever increasing amounts of oil, gas and other fuels to run their economies. It is the life-blood. As globalization lifts millions out of poverty, the demand for energy worldwide will continue to grow, and we risk ending up with a volatile, “beggar thy neighbor” style of competition between countries to control sources of supply, especially in the developing world.

Even casual newspaper readers have become aware that there are very strong links between growth in energy demand, economic development, security, and foreign policy. Precisely what these links comprise is not always clear. The problems of energy “dependence,” “independence,” and “interdependence” are being debated in a burgeoning literature for both laymen and specialists. The deployment of oil as a political weapon occurred most manifestly during the 1973-74 Arab embargo. More recently, Iraq’s invasion and Russia’s use of gas as the Kremlin’s instrument of choice in relations with other C.I.S. countries and the EU came to the spotlight, as did China’s expanding acquisitions of energy assets worldwide1.

Between 2002 and July 2008, prices more than trebled, to $147 a barrel. Among other events related to energy and foreign policy were: blackouts in California, a standoff between the West and Iran over Iran’s nuclear program, frequent attacks on oil facilities in Nigeria, politically driven interruptions in Venezuela’s production, the occurrence of Hurricane Katrina in 2005, Iraq’s slip into civil anarchy and the subsequent delay in the return of its production to pre-Saddam era levels, and general concerns over terrorist attacks on energy facilities.

The current power struggle has now been directed towards maximizing economic interests, gaining commercial advantage on technologies, and securing scarce resources (i.e. energy, water, food and metals) in a highly competitive, global environment. Possession, financing, production, transportation, and marketing of energy have become key determinants in international relations among nations, which seek either demand or supply security2.

Energy at the Center of Foreign and Security Policy

The world energy is by definition both an above-ground and below-ground system. What makes it somehow unstable are the “above-ground factors”, such as technological developments, war, civil unrest, energy policy, investment decisions and a host of other human actions, rather than the “below-ground realities”. This kind of thinking should not also ignore the climate change implications of burning the earth’s existing inventory of hydrocarbons and downplay the geologic constraints on oil and other fossil fuel supplies.

Geopolitics often takes a back seat when confronted with the choice of advancing business, commercial, energy and technological interests vis-à-vis vaguely defined political interests3. Moreover, we are witnessing the inexorable rise of the new Asian great powers, China and India; by 2020 these and other “giants” will be flexing their economic muscles to the east of Turkey. They are among the largest energy-deficit nations. The relativities of power are changing with the erosion of America’s margin of superiority in economic, military, and ‘soft power’ terms. Few financial concepts have caught on as quickly as “BRICs,” a term coined by Goldman Sachs, which stands for Brazil, Russia, India, and China, the “Big Four” fastest-growing economies in the world today.

By dint of their sheer size and population – and their collective decision to embrace their own particular brand of capitalism – BRICs are the economic future of the world. Together, the BRICs encompass more than 25percent of the world’s land mass and 40percent of the world’s population. Thanks to their anticipated, rapid growth, by 2050 the BRICs could eclipse the joint economies of the current, richest countries of the world. China and India will become the dominant global suppliers of manufactured goods and services. Brazil and Russia will be the world’s leading suppliers of commodities. The BRICs today already account for a combined GDP of $15.435 trillion on a purchasing power basis4. By that measure, they are already collectively larger than the U.S..5

For the first time in recent memory, BRICs are growing not by borrowing, but by investing. China has the world’s highest savings rate. Brazil and Russia are sitting on huge foreign currency reserves, thanks to windfalls from oil profits. Soaring commodity prices have put more money in BRICs’ pockets than ever before. That means much less danger of a financial meltdown like those that Brazil and Russia experienced in the 1980s and 1990s. A decade after defaulting, Russia has a higher credit rating than the EU economies of Greece and Portugal.

Energy supplies are likely to get tighter in the next few decades for all economies, unless massive investments and new technologies are mobilized. The root-causes for most geopolitical tensions are the scarcity of resources that fuels competition among nations for a bigger pie, particularly in energy, water or food. Our generation never had to bother much about turning out the lights, heating our homes, or driving our cars. But our children’s will. Today, Europe imports around 50 percent of the energy it consumes. By 2030 this could be around 64 percent6. There is nothing wrong with importing energy per se, provided that we are talking about open, transparent, and competitive global markets. However, in today’s world, we are often not. Increasing our energy imports, therefore, calls for a full assessment of risks.

The global energy scene is going through a fundamental transformation and powershift that will not only change the rules of the game; it will also change the game itself, and its players

For Europe, the particular concern relates to gas imports. Following the abrupt weakening of Saakashvili manu militari in the summer of 2008 and, more recently, the democratic installation of President Viktor Yanukovich in Ukraine, Russian hegemony in the C.I.S. region has been restored to levels unprecedented since the fall of the Soviet Union. With Europe busy trying to solve its debt and currency crisis, Moscow has not hesitated to monetize its political gains, seeking long-term control of the energy sector in Ukraine, as well as strengthening its influence on those of Azerbaijan, and – to a lesser extent – Turkey7.

However, the EU’s situation might not be as gloomy as it appears, mainly because Europe’s energy security is not seriously endangered. Russia still provides the majority of natural gas imports in most EU countries, but alternatives abound. The little-publicized GALSI pipeline between Algeria and Italy will be operational in 2014, while Libya and Nigeria are two other good candidates for gas supplies. Rapid technological developments in liquefaction technology and shale-gas extraction also provide Europe with options it did not have only a few years ago.

Further, the strong bargaining power currently enjoyed by gas producers may not be a permanent condition. Prices for natural gas have never been so low on the spot market, and a recent attempt by producers to establish a price floor by cutting production failed miserably at the Gas Exporting Countries Forum summit in Oran, Algeria. It bears noting, too, that nuclear and solar power are rapidly increasing their share in Europe’s energy mix.

Nevertheless, the EU should still reassess the objectives that inform its energy policy. Trying to guarantee the security of supplies by battling with Russia for influence in the post-Soviet space is a costly strategy, one that inevitably puts Europe in a disadvantaged position, given the deep political, economic, historical, and cultural ties that Moscow enjoys with local leaders and populations. Moreover, the control of energy networks lies at the core of Russia’s statehood, and as a result is accorded the highest priority in Moscow. By contrast, energy security will always be merely one among many items on Europe’s agenda.

Profound Changes in World Energy

As a result of these developments, the global energy scene is going through a fundamental transformation that will not only change the rules of the game; it will also change the game itself, and its players.

First, volatile prices have, together with many other factors, shifted power significantly to producing countries, especially a few large ones, where the majority of remaining reserves are located, such as the Gulf, Russia, and Central Asia. These countries seek a changing or reshaping of the traditional rules of the game for the benefit of their national interests.8 They have the political will to use energy as an instrument to advance their economic and political interests.9Aware of their increasing power, many of the resource-rich countries either have re-nationalized their oil industries, or have established strategic control through further transfer of power into the hands of governments.10 Production sharing contracts are in the process of being transformed into technical service contracts.

Second, there is an increasing concern over the security of the energy supply on the consumer’s side. Due to increased demand and depletion of domestic reserves, major consumers will have to rely more on imported oil and gas, from a few politically instable regions such as the Middle East, Africa, Russia and Central Asia, through long-distance pipelines, and vulnerable sea routes11. This, combined with the fact that the international market is less stable and more prone to the disruptions of natural disasters, terrorist attacks, and isolated geopolitical acts, has increased the vulnerability of these consumer countries. Yet, suppliers are also concerned about demand security given the depressed prices and demand in most OECD economies as a result of the economic recession.

Third, although the OECD countries are still the largest oil consumers, the current increase in demand for oil and gas is mainly driven by fast economic development in developing countries such as India and China, which account for one-third of the world population but only consume 17 percent of world energy. In order to access the new and prosperous market, government-to-government relationships are not only necessary, but essential12.

Fourth, a rising concern for security of demand among major producer countries may prevent large scale of investment from happening. To meet the rising energy demand, a huge amount of investment is needed.13. Energy investment worldwide has plunged over the past year in the face of a tougher financing environment, weakening final demand for energy and lowering cash flow. It is estimated by IEA that global upstream oil and gas investment budgets for 2009 were cut by around 19 percent compared with 2008 — a reduction of over $90 bn.14 The 2010 figures are not encouraging, either.

Turkey, poor in energy resources, and one of the high growth energy markets, also commands major chokepoints and transit routes for energy shipments

The uneven distribution of energy resources among states, and the critical need to access those supplies by all states, leads to significant vulnerabilities15. The coercive manipulation of energy supplies, competition over energy sources, the tendency of energy producing countries to political instability, attacks on supply infrastructure, competition for market dominance, accidents, and natural disasters are all adding significant risks to global energy security16. Increased competition over energy resources may also lead to the formation of security compacts to enable an equitable distribution of oil and gas between major powers.17

Concerns over energy security are not limited to oil. Power blackouts on both the east and west coasts of the U.S., in Europe, and in Russia, as well as chronic shortages of electric power in China, India, and other developing countries, have raised concerns about the reliability of electricity supply systems.

Western countries are producing less and less of their own energy, and are therefore having to import more and more. This is having a massive impact on the transfer of wealth. The energy guru, Daniel Yergin, has estimated that, at early 2008 prices, the U.S. is currently transferring about $1.3 billion to the oil-producing countries every day – or if you prefer, $475 billion a year. If we include China, the EU, India, and Japan in this calculation, every year the major oil consumers are transferring over $2.2 trillion to the oil producers18. What we know is that these massively increased energy revenues not only mean more economic power for the oil producers, but also, of course, increasing political power and influence in shaping the new global security order.

Just consider one fact. The US consumes 25 barrels of oil per capita annually and Europe ten barrels. Each Chinese, however, consumes only two barrels a year, so even a small increase in Chinese consumption could have a massive impact on the market. Therefore, this is not the time to slacken our efforts to find ways to use oil and gas more efficiently. We must push ahead with our conversion to alternative fuels, and seriously look at ways of diversifying our energy supplies to reduce our vulnerabilities.

This brings us to the third concern. As the world’s need for energy grows, the ability of the traditional suppliers to continue to meet the demand is far from certain. Europe, for example, is increasingly dependent on Russian oil and gas. But Russia’s currently exploited energy reserves are depleting fast. Russians now consume more and more of their own gas at home and the country’s energy output is shrinking due to a lack of investment in new technology, and in developing new fields.

Another concern is the protection of critical infrastructure. As western, domestic sources of energy start to dry up, oil companies are drilling in much more isolated and hostile environments, because technology makes extraction more commercially viable. More oil and gas is extracted from under the sea rather than from under the land. Tankers criss-cross the oceans delivering these products from one continent to another. Pipelines are getting longer and often pass through unstable areas19. Over the past few months we have seen several examples of how easily these sophisticated supply networks can be threatened – in the Nigerian Delta, off the coast of Somalia, and in the Southern Caucasus.

As climate change impacts on energy exploration and transit routes, it will also increasingly impact our security. As the polar icepack melts, and the Northwest Passage to Asia opens up, an increasing amount of shipping will pass through one of the most remote and inhospitable parts of the world. Intervening in the event of an environmental disaster or even a terrorist attack would be very difficult indeed.

Turkey as a Major Actor in International Energy Diplomacy

In this changing world energy landscape, Turkey has emerged as one of the newest, and most dynamic and proactive players in ensuring secure, uninterrupted, clean, and reasonably priced energy resources. As a significant emitter of carbon dioxide and an ideal ground for solar, wind, hydro, geothermal and (perhaps) nuclear energy, it is also set to become a major player on the world’s increasingly important climate change and green energy stage.

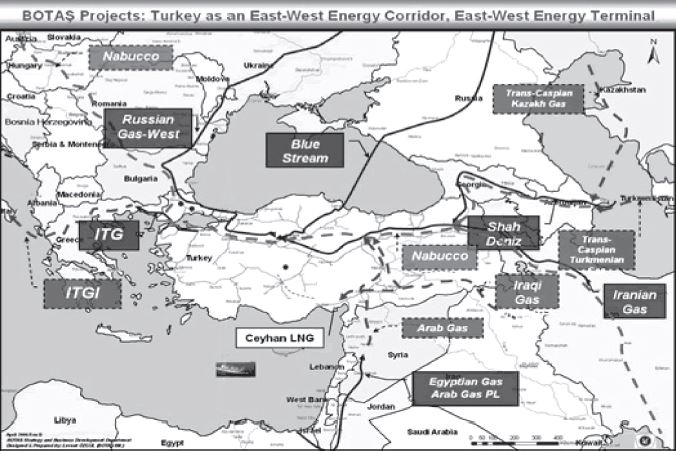

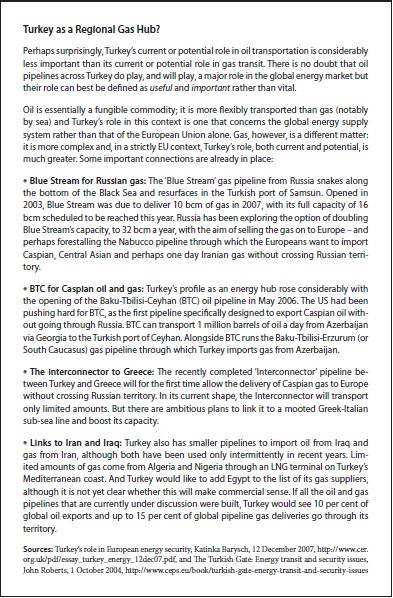

A key transit/terminal hub of both oil and gas to the heavy consumer nations of Europe, Turkey is a nexus of multiple important pipeline projects and provides access to the Bosporus Strait and the eastern Mediterranean via the Ceyhan terminal. Not only a significant consumer in its own right, Turkey is also geographically close to 72 percent of the world’s proven oil and gas resources, and thus is a natural energy hub between major oil-producing areas in Russia, the Caspian Sea basin, and the Middle East, and European consumer markets and has thus become the “Silk Road of the 21st century.”

Turkey, poor in energy resources, and one of the high growth energy markets, also commands major chokepoints and transit routes for energy shipments. In natural gas, Turkey is Gazprom’s second largest market in the world after the EU. Despite difficulties in sustainable supply, Turkey is the only market for Iranian gas exports to date. It is the major outlet for Azerbaijani oil via BTC, and gas via the TGI Interconnector and the South Caucasus Pipeline. Iraq’s entry to the Mediterranean markets is through Turkey’s Yumurtalik deep-sea port. Russia plans to send gas beyond Turkey through Blue Stream-II.

Turkey is not blessed with its own domestic energy resources, and imports more than 60percent of the energy it consumes. The Turkish government predicts that energy needs will increase 10 percent each year for the next 20 years. Energy supply security20 is of prime importance to the country’s sustainable growth and development. Russia plays a critical role in Turkey’s energy supply security, as it provides around 68 percent of its natural gas supply, and 50 percent of crude oil imports. Azerbaijan has emerged as a key supplier of oil and gas. Iran has the largest potential, if its domestic production can be mobilized. Iraq and the Arab peace pipeline coming from Egypt could also be other potential insurers of Turkey’s energy security.

Turkey’s domestic supplies, particularly in oil and gas, are miniscule. Its own oil and gas reserves account for only a tiny fraction of its rapidly rising demand. Oil consumption, at 35 percent, accounts for the majority of Turkish energy consumption (675,000 barrels per day - bpd) while crude production stood only at 48,000 bpd in 2009, This is followed by natural gas at 29 percent, coal at 25 percent, hydroelectric and renewable consumption at 11 percent. Nuclear electric energy consumption is for the time being zero – two nuclear power plants are under consideration with Russian and Korean support.

The expected growth in oil consumption is expected to continue at a rate of about 2-3 percent per year. Turkey’s oil consumption, 76 million tonnes of oil equivalent in 1998 and 179 Mtoe now, is expected to reach 319 Mtoe by 2020. Turkey’s natural gas consumption is expected to grow rapidly, quadrupling within the next 20 years, with 1,400 bcf gas consumption projected for 2020.

Russia is currently Turkey’s top supplier of oil, followed by Iran and Saudi Arabia, with lesser volumes supplied by Libya, Iraq, and Syria, among others. Turkey is playing an increasingly important role in the transit of oil supplies from Russia, the Caspian region, and the Middle East to Europe. Growing volumes of Russian and Caspian oil are being sent by tanker via the Bosphorus Straits to Western markets, while a terminal on Turkey’s Mediterranean coast at Ceyhan allows the country to export oil from northern Iraq, via a pipeline from Kirkuk and from Azerbaijan, via the Baku-Tbilisi-Ceyhan pipeline.21 To ease increasing oil traffic through the Bosporus Straits, a number of Bosporus bypass options are under consideration in Bulgaria, Romania, Ukraine and Turkey itself (i.e. Samsun-Ceyhan).22

Russia plays a critical role in Turkey’s energy supply security, as it provides around 68 percent of its natural gas supply, and 50 percent of crude oil imports

While Turkey gets oil from a variety of sources, more than 60 per cent of its gas needs are met by just one supplier: Gazprom23. At the moment, Turkey is not short of gas. On the contrary, the long-term contracts that it has signed with Russia, Iran, Azerbaijan, and other suppliers including LNG commit it to buying more than it actually needs. This leaves it potentially liable to pay penalties for breaching the take-or-pay contracts. So Turkey needs to build infrastructure for storing gas, for re-exporting surpluses to the EU and, most importantly, for distributing the gas imports around the country so that factories, power plants and households can use it.

Turkey is positioned to play an even bigger role linking gas producers in the Caspian and Middle East to consumers in south-eastern and central Europe with the proposed Nabucco gas pipeline project and a potential Iranian gas transit deal. The Nabucco project is geopolitically significant as it will secure access to new gas supplies from new sources in the Caspian region as well as the Middle East. For this reason it has been regarded as vital for the EU’s long-term strategy to boost supply security, yet it suffers from a couple of problems including the lack of an exclusively dedicated reserve base24.

For Turkey to function as a gas transit state, it must be able to import enough gas to satisfy both domestic demand and any re-export commitments, as well as provide enough pipeline capacity to transport Caspian and Middle Eastern gas across Turkey to Europe.

A Genuine Regional Powerhouse and Energy Hub?

By any objective criteria, Turkey is a regional power with which to reckon. A country of 780,576 square km, Turkey is almost the size of Germany and France put together. What opponents of Turkey’s EU accession complain most about is that its population is too poor, and too big (at 73 million today and 80 million by 2015), although they are increasingly better educated and prosperous. If calculated in terms of purchasing power parity, Turkey is among the world’s top 17 economies, with a GDP size of around $750 billion (the largest in its region and 7th largest in Europe), with a total trade volume of $243 billion in 200925 and F.D.I .inflow of $18 billion in 2008 (stock value: $85 billion).

Added to these facts are Turkey’s huge military power (second largest in NATO after the US and biggest in its region), world class manufacturing and construction capacity, its status as a cultural center of attraction, and vast tourism potential. These facts imply a medium-size, global, economic, and military power. Turkey can do much better over the longer term, judging from the performance of dynamic Asian economies, if it can pursue a “high growth” (i.e. 7-8 percent per annum) path.26

Conscious of its unique assets in hand, Turkey pursues a long-term strategy of becoming a major Eurasian energy hub.27 Better connections with both supplier countries and energy consumers not only serve to increase Turkey’s geopolitical standing, they also bring lucrative business opportunities in the form of transit fees, or through new refineries, LNG terminals, and trading facilities. Another value is to diversify Turkey’s own energy supplies and to re-export any surplus gas it may have.

Yet, whether the Turkish goal of becoming an energy bridge along east-west and north-south axes (and serving not only as a transit country, but also as an aggregator and center of trade) is a realistic one remains largely unanswered. True, Turkey is located at the crossroads of regions possessing three-quarters of the world’s oil and natural gas reserves – sandwiched between major centers of energy production and consumption. Oil is fungible and could easily find its way to international, high-value markets, once it is loaded on a tanker. The critical fuel is natural gas.

If Turkey becomes a transit country for Russian gas only, its value will be rather insignificant. Turkey could become a critical energy hub if its supplies of gas were to originate from multiple sources, such as Russia, Turkmenistan, Iraq, and Iran. If Turkey could offer access to Russian and non-Russian gas supplies to European markets, its role as an integral part of the European energy structure would be secured.

In many ways, Turkey already fulfils the role of an energy hub. It does so in transporting oil through the Bosphorus strait and through several new pipelines linking it to Russia and the Caspian. Every year, some 10,000 tankers pass through the Bosphorus strait, which connects the Black Sea with the Mediterranean. Traffic keeps growing rapidly, and today a tanker maneuvers through these narrow, busy waterways every 20 minutes during the daytime.28

EU Accession and Energy Linkage

The EU agreed to begin membership talks with Turkey in 2004, some 50 years after the country first expressed interest. But the talks have gone slowly, as the EU has frozen a third of the so-called negotiating chapters, mainly over Turkey’s refusal to open its ports to recent EU entrant Cyprus. France, Germany and several other current members have repeatedly said they don’t believe Turkey belongs in the bloc

Can Turkey live up to its own rhetoric of being an energy hub? There are three projects on the drawing board. Nabucco, an ambitious scheme to pipe up to 30bn cubic metres of gas to central Europe, is competing for supplies with two simpler schemes using Turkey’s existing infrastructure: the ITGI project to connect Azerbaijan to Greece and Italy, and the TAP project linking Albania to Italy. Although Nabucco aims eventually to bring gas from Turkmenistan, Iraq and even Iran, none of the three projects will get off the ground without supplies from Azerbaijan’s Shah Deniz II fields, set to come online in 2016 and produce up to 16 bcm a year29.

Agreements between Baku and Ankara pencilled in June 2010 may determine which of the projects wins out. The neighbours signed MoUs which, once details are finalised, will set transit tariffs for gas shipped across Turkey, and decide if Shah Deniz II gas sold to Greece will be marketed by Azerbaijan, or sold on by Turkey. The impact on Nabucco of the final terms reached is indirect, but crucial, as it will enable Azerbaijan to define the economics of using ITGI and TAP and compare them with the economics of transiting gas through Nabucco.

But Europe’s willingness to back Nabucco may be wavering as the urgency of tapping new supplies lessens. Gas consumption could take years to match pre-crisis levels; North African supplies will rise; and the EU may opt for gradual improvements over grand schemes: increased storage, reverse flow capabilities, small interconnectors. Ankara is certainly juggling plenty of projects. Besides Nabucco, ITGI and TAP, Russia is looking at routing its South Stream gas pipeline - a rival to Nabucco - through Turkish exclusive economic zone. Moscow is also backing a pipeline intended to cut traffic through the Bosphorus, and preparing to build Turkey’s first nuclear power plant.

In comparison to Russia, the EU in terms of population is three-and-a-half times as big. Its economy is 15 times that of Russia. Its defense spending is 10 times higher. True, the EU is dependent on Russia for gas and oil imports but Russia is equally dependent on the EU for its energy markets. Gazprom’s biggest and highest purchasing customer is the EU, followed by Turkey.

But the EU is concerned over its growing dependence on Russia. And Turkey’s development as an European energy hub looks natural, with vast oil and gas reserves lying in the countries to its east, and one of the world’s biggest energy markets to its west. It is anticipated that six to seven per cent of global oil supply will transit Turkey by 2012.30 Ceyhan, on the Mediterranean, is already the terminal for a pipeline from Iraq’s Kirkuk oilfields , another one from Baku and with a planned line from the Black Sea city of Samsun, it is expected to account for 8 percent of global crude trade. Energy policy co-operation would give Europe a “reliable alternative supply route” and offer Turkey “the opportunity to prove that it is an indispensable partner” for the EU.31 Better connections with both supplier countries and energy consumers would increase Turkey’s geopolitical standing and generate “lucrative business,” such as transit fees as well as new refineries, terminals and trading facilities.

For its part, Turkey appears to be pursuing a two-pronged energy strategy. First, it seeks to diversify its own sources of imported fuel. Second, the Turkish strategists see the turning of their country into an east-west energy corridor as part of a broader plan aimed at enhancing Ankara’s geopolitical role in the region. Indeed, the main components of the Turkish energy corridor are the Straits, the Baku-Tbilisi-Ceyhan crude oil pipeline, the Shah-Deniz natural gas pipeline (Baku-Tbilisi-Erzurum), the Blue Stream, Iraq and Iran pipelines and the Trans-Caspian/Nabucco Gas Pipeline projects.

Some EU officials say that energy is too pressing an issue to wait for the accession talks to make progress. They add another argument for decoupling energy from the enlargement process, namely that Turkey should not be allowed to use its strategic location to get concessions from the EU. This, they fear, could set a dangerous precedent: once Nabucco and other energy links are in place, Turkey could try to use them to get ahead in negotiations with its EU partners in unrelated areas. Such fears are probably exaggerated. They certainly should not be used as an argument for not opening the energy chapter. If the EU is serious about the diversification of its energy supplies, it needs to do its utmost to unblock the accession talks in this area.

Turkey’s accession to the EU will only make progress if both sides keep reminding themselves of the benefits that deeper integration and closer co-operation would bring for both parties. Energy is an area where early gains are available. The fact that Turkey is negotiating for membership should help, not hinder, progress in this area. The evolving nature of the EU’s energy policy gives Turkey a great opportunity to make sure that its own energy policy contributes to Europe’s energy security, without neglecting its own strategic energy and security interests.

Energy policy co-operation would give Europe a “reliable alternative supply route” and offer Turkey “the opportunity to prove that it is an indispensable partner” for the EU

The possibility of Turkey shifting its focus in favour of Russia and the Middle East, as it now seems to be in the process of doing, despite denial by Turkish leaders that there is no change in the axis of the country’s foreign policy, can easily be explained as a kneejerk reaction to the continuing saga of Turkey’s long-standing application for EU accession. Turkey feels it has met all the requirements put forward by the EU, but that Brussels keeps moving the goal posts while the game is underway. Prime Minister Erdogan, in fact, compared the E.U’.s attitude towards Turkey to “changing the rules for the quarterback in a football game in the 36th minute.”32 In its own region, Turkey is regarded as a regional powerhouse and a force to be reckoned with, as opposed to the West, where many Turks are fed up with being treated like a second-class, poor man trying to gain entry into an elite club.

Growing (Inter)dependency with Russia?

Turkey’s closer association with the EU on energy matters should not come at the expense of its mutually beneficial partnership with Russia. Over the last decade, some very significant shifts have taken place in Eurasia’s geopolitical landscape, with Turkey and Russia moving away from Cold War era animosity and toward what seems to be ever closer cooperation. Analysts and politicians in the two countries have advanced a set of similarities that account for the ongoing rapprochement between Ankara and Moscow.

The Turks and the Russians were perceived as “significant Others” in the process of the construction of European identity and to this day have remained largely uncertain as to how they relate to Europe. Once the worst of enemies, involved in 12 wars in three centuries, Turkey and Russia have suddenly become the best of friends, forging strong bonds to advance their own economic and geopolitical interests in Eurasia, and often turning a blind eye to the concerns expressed by Brussels and Washington.

It is becoming increasingly evident that Moscow matters to Turkey more than ever. Russia has become Turkey’s biggest economic partner, replacing Germany; trade between the two countries reached $40 billion in 2009, an eightfold increase in eight years, and is expected to reach the $100 billion mark in the next four years. Turkish construction firms are omnipresent all over Russia. Millions of Russian tourists flock to Turkish resorts every year – 3 million last year. There are tens of thousands of intermarriages.

The two countries’ growing closeness is probably helped by the similarities between Putin and Erdoğan: Both come from humble origins; both seem ready to bury historical enmities; and both are seen as strong leaders, firmly entrenched in power for years to come. “If there is the touch of a Czar in Putin, there is a Sultan in Erdoğan.”

Turkey, conscious of its critically important role as a corridor for energy, has been flexing its muscles, indicating its growing assertiveness and autonomy as a regional power to be reckoned with. This is happening at a time when Turkey’s accession process is faltering in the face of opposition from several EU countries. Ties with Washington are yet to be reconsolidated after painful, Bush-era insensitivities towards Turkey’s vital interests.

Russia’s energy engagement with Turkey is based on several pillars supporting an overall “win-win” strategy. The Kremlin tries to capitalize on its energy “weapon” as a source of comparative advantage in the global system, trying (successfully or unsuccessfully) to combine the maximum efficiency of a private management with state control of the “critical industries.” Therefore, Russia is seeking control over the three major elements of the “energy chain” – production, transit and processing/distribution – by supporting the international expansion of Russian energy companies, (i.e., the acquisition of assets and the control of existing and prospective energy resources) and alliance with other energy producing and transit states, and also with the national oil companies and international oil companies. It also supports Russian companies’ access to the downstream markets (and mid-stream facilities) of the energy consuming countries33.

In July, 2008, LUKOil significantly boosted its downstream presence in Turkey by buying a network of filling stations from Akpet. Russia also wants to play a lead role in Turkey’s lucrative downstream sector, the second pillar of the strategy. Gazprom is keen on bidding for major city distribution projects and gas-fired power plants, while Rosatom has offered to move ahead with a Russian-built nuclear power plant. Last but not least, Moscow managed to get Ankara’s permission for its South Stream pipeline to Italy to pass through Turkish waters in the Black Sea.

Turkey is not naive in its assumptions and has learned the game for an effective play on the crowded chessboard with Russia, EU, U.S., and other major energy powers

As a quid pro quo, Moscow offered to support and supply the Samsun-Ceyhan oil pipeline, which will connect Turkey’s Black Sea port at Samsun and an oil terminal at Ceyhan on Turkey’s Mediterranean coast. The pipeline is designed to ease the traffic going through the Bosphorus Straits, a bottleneck that handles about 3.7percent of the world’s oil supply. Gazprom also affirmed a commitment to expand the existing Blue Stream gas pipeline to Turkey.

The Turkish government, however, seems determined to go through with the Iranian gas deal, arguing that the country needs to diversify its sources of supply to avoid becoming over-dependent on one supplier

Turkey is not naive in its assumptions and has learned the game for an effective play on the crowded chessboard with Russia, EU, U.S., and other major energy powers. Ankara is confident that it can handle both the challenges and opportunities associated with Russia’s position as an energy power. Russia’s importance to Turkey is not new. It has traditionally been the biggest player in the region and it figures prominently in almost all of Turkey’s energy designs and geopolitical calculations. But Russia’s traditional dominance in the region is being challenged by China and other relative newcomers, primarily the U.S. and the EU Russia knows that. A desire to regain some of the influence it has lost has encouraged it to foster new partnerships, as in the case of Turkey. As energy looms larger in the domestic and regional calculus of both countries, especially with regard to their European. relationships, the strategic importance of the Turco-Russian rapprochement will undoubtedly grow stronger.

Eurasia, the Middle East and Energy Linkages

Under the Ottomans, Turkey was actively involved – indeed, was the dominant power – in the Middle East. Thus, in many ways Turkey’s more active policy in the Middle East of late represents a return to a more traditional pattern of behavior.34 The new Turkish foreign policy vocabulary in the region, according to Ian Lesser, a senior transatlantic fellow at the German Marshall Fund of the U.S.,35 now sounds very much like that of India, South Africa, Mexico, China, Indonesia, or Brazil. This kind of posture – not so much neo-Ottoman as neo-non-aligned – could well be the most important new dimension of Turkish foreign policy over the next decade, he says. It will shape the way the U.S. deals with Turkey. And it will influence and perhaps complicate Europe’s relationship with Turkey as an EU candidate. “Today’s Turkey brings a lot more foreign policy capacity to the table, but it may not be an easy fit with Europe’s interest in forging common strategies on key issues, including on Iran and Russia,” he argues.

Indeed, the region’s geopolitical and energy map is being redrawn. For example, the inauguration of the Dauletabad-Sarakhs-Khangiran pipeline in January 2010 connecting Iran’s northern Caspian region with Turkmenistan’s vast gas field went unnoticed. It followed Turkmenistan’s commitment of its entire gas exports to China, Russia, and Iran in a space of three weeks, indicating that Ashgabat has no urgent need of the pipelines that the U..S and the EU have been advancing westward. The 182-kilometer Turkmen-Iranian pipeline starts modestly with the pumping of 8 bcm of Turkmen gas. But its annual capacity is 20 bcm, and that would meet the energy requirements of Iran’s Caspian region, and enable Tehran to free its own gas production in the southern fields for export.

In this new pattern of energy cooperation at the regional level, Russia traditionally takes the lead, then China and Iran follow the example. Russia, Iran and Turkmenistan hold, respectively, the world’s largest, second-largest and fourth-largest gas reserves. And China will be consumer par excellence in this century. Russia does not seem perturbed by China tapping into Central Asian energy. Europe’s need for Russian energy imports has dropped and Central Asian energy-producing countries are tapping China’s market. From the Russian point of view, China’s imports should not deprive it of energy (for its domestic consumption or exports).

Russia has established a deep enough presence in the Central Asian and Caspian energy sector to ensure it faces no energy shortage. What matters most to Russia is that its dominant role as Europe’s number one energy provider is not eroded. So long as the Central Asian countries have no pressing need for new U.S.-backed trans-Caspian pipelines, Russia is satisfied. Russia is now planning to double its intake of Azerbaijani gas, which further cuts into the Western efforts to engage Baku as a supplier for Nabucco.

In tandem with Russia, Iran is also emerging as a consumer of Azerbaijani gas. In December 2009, Azerbaijan inked an agreement to deliver gas to Iran through the 1,400km Kazi-Magomed-Astara pipeline. In addition to Iran’s gas contract with Turkmenistan, Tehran recently offered to buy a 10 percent stake in the second phase of Azerbaijan’s Shah-Deniz gas field for $1.7 billion.

Turkey is not far off in this equation. Tehran claims to have a deal with Ankara to transport Turkmen gas to Turkey via the existing 2,577km pipeline connecting Tabriz in northwestern Iran with Ankara.36 Iran remains the single most important item on Turkey’s plate and Ankara is becoming a hub for Iranian efforts to communicate with the West in its attempts to end this isolation. As a historical adversary of Iran, Turkey indeed has managed to steer a remarkable course in foreign policy, but faces a host of new challenges to continuing its balancing role in the region. Iran’s push for nuclear weapons—which analysts fear could prompt such regional powers as Saudi Arabia, Egypt, and Turkey itself, to develop a nuclear deterrent—is a case in point.

Indeed, these economic ties have not quelled Ankara’s anxiety over a nuclear-armed Iran. Turkey and Brazil brokered an historic deal in Tehran on 17 May, 2010, by which Iran agreed to ship most of its enriched uranium to Turkey to ease the international standoff over the country’s disputed nuclear program and deflate a U.S.-led push for tougher sanctions. The U.S., along with several other Western countries, said, however, that the deal does not really change many things as Iran will continue to enrich its uranium.

Trade between Iran and Turkey surpassed $10 billion last year. The two countries are determined to increase it to $30 billion. They also plan to set up a joint industrial zone in a border area. Energy has been an important driver behind Turkey’s rapprochement with Iran, which is the second largest supplier of natural gas to Turkey, following Russia.37 In July 2007, Turkey and Iran signed a Memorandum of Understanding to transport 30 bn cubic meters of Iranian and Turkmen natural gas to Europe.38 The deal envisages the construction of two separate pipelines to ship gas from Iranian and Turkmen gas fields. TPAO has also been granted licenses to develop three different sections of Iran’s South Pars gas field, which has estimated total recoverable reserves of 14 trillion cubic meters.

The deal has been sharply criticized by the U.S., which opposes large investments in Iran’s energy sector.39 Washington is also concerned that the deal could undercut U.S.-Turkish cooperation to develop Caspian gas resources and construct pipeline infrastructure to transport these gas resources to Turkey and international markets. Instead of the deal with Iran, U.S. officials want Turkey to either intensify cooperation with Azerbaijan to transport gas from the Shah Deniz fields or to import gas from Iraq. The Turkish government, however, seems determined to go through with the Iranian gas deal, arguing that the country needs to diversify its sources of supply to avoid becoming over-dependent on one supplier.

Its partnership with the U.S., its prospective membership in the EU, its strong ties to Eurasia and the Middle East, make Turkey an irreplaceable partner on all regional energy and foreign policy matters

Ankara and Tehran signed $1.5 billion in agreements providing for the joint construction of three 2,000-megawatt thermal power plants – two in Iran and one in Turkey, and several hydroelectric plants in Iran with a total 10,000-megawatt capability. Under terms of the agreement, Ankara will import 3 billion to 6 billion kilowatt hours of electrical energy annually. At present, Iran exports electricity to Turkey through two transmission lines totaling 250 megawatts. In June 2007 Turkey and Iran signed a memorandum of understanding under which Turkish Petroleum Corporation (TPAO) will operate in Iran and exploit three natural gas areas in the South Pars region. The company plans to invest $3.5 billion to operate these fields. Moreover, the two countries will build a 2000-km pipeline between them to transport Iranian gas to Europe. Turkey also announced readiness to ink the required agreements on linking Trabzon port to Bandar Abbas.40

Two visits made in October, 2009, may serve to more vividly illustrate Turkey’s activist foreign policy in the Middle East. Prime Minister Erdoğan, accompanied by nine ministers and an Airbus full of businessmen, visited Baghdad, where he held a joint session with the Iraq government and signed no fewer than 48 memoranda in the fields of commerce, energy, water, security, forestry, the environment, and so forth. At almost the same time, Foreign Minister Davutoğlu was in Aleppo, where he signed another 40 agreements with Syrian Foreign Minister Walid al-Muallim, of which perhaps the most important was the removal of visas, allowing for a free flow of people across their common border.

Ankara, Erbil and Baghdad, with support from the U.S. and some EU countries, particularly the U.K., have been diligently working on a special plan to put the relationship between the three countries on a healthy footing. Energy cooperation remains one of the main drivers behind closer partnership. There are a number of issues to be resolved, such as how to phase out the P.K.K, and the status of the multi-ethnic Iraqi city of Kirkuk, and energy investment regime and transit routes. On the other hand, Ankara, Erbil and Baghdad feel that these issues need to be settled and energy cooperation should be dealt with separately. If the hydrocarbon law is adopted by the Iraqi government and Parliament, there will be significant exploration and production activity in the KRG area as well as in Basra and central Iraq. It is vitally important for Turkey to have its fair share of contracts, both in Northern Iraq and in the rest of Iraq.

In terms of energy security, Europe should be aware of the fact that it is indeed competing with China for Caspian/Central Asian energy supplies and not with Russia

Prospects and Options

As a pivotally located country, Turkey will continue to be an important partner to Western, Russian, Caucasian, and Middle Eastern energy and foreign policy initiatives. Its partnership with the U.S., its prospective membership in the EU, its strong ties to Eurasia and the Middle East, make Turkey an irreplaceable partner on all regional energy and foreign policy matters.

What Turkey has been doing systemically since 2002 in this most difficult part of the world is not a simple drifting away from the West and embracing “rogue” and “anti-Western” nations at the expense of its historical western vocation. Such criticisms result from a lack of faith in Turkey’s transformative power. It is also too early to judge Turkey’s multi-vectored drives as successful. Indeed, far from looking for a life without them, Turkey is looking for an upgraded relationship with the U.S. and the EU. Clearly, Turkey can hardly expand its influence without first having a firm footing in the West.

A more promising approach lies in better understanding Turkey’s drives, needs and priorities and seeking Western alignment for a durable, “win-win” relationship with Ankara as well as using Turks’ leverage in the broader Middle East, Eurasia and Southeast Europe to find solutions to protracted problems that the West has thus far failed to address.

Turkey’s respected and non-confrontational rise in that volatile, troubled region that is increasingly peaceful, with countries cooperating with one another, is good for the West and the world. This is an exceptional and unique role Turkey could play – as a regional “hub,” rather than a “bridge.” This is what Washington and Brussels should be supporting wholeheartedly, rather than getting worried about. The signature policy of Turkey’s new self-confidence is the policy of “zero problems with neighbors.” This marks a revolutionary change from the “siege mentality” that promoted the paranoiac view that Turkey was surrounded by enemy countries. One after another initiative has been launched to pave the ground for the settlement of the most historically deep-seated and complex problems.

Turkey could provide both a new and reliable transit corridor capable of transporting both Russian and non-Russian gas to Europe in the event of a supply crisis

In terms of energy security, Europe should be aware of the fact that it is indeed competing with China for Caspian/Central Asian energy supplies and not with Russia. There is little doubt that Russia’s energy overtures to Turkey have a strong geopolitical dimension. It wants to draw Turkey into a closer strategic alignment with Russia, but, primarily, they are designed to have an effect on Europe. That effect is both political and specific: Russia wants Turkish interests to be so intertwined with Russia’s that the E.U’.s southern gas corridor project, Nabucco, would be less of a threat to Russia’s interests.

But while Russia may see closer ties to Turkey as a means of limiting the increase in Europe’s role in the economies of the former Soviet Union, it would be an overstatement to say that Turkey is turning its back on Europe, or simply playing the Russia card against the West in order to strengthen its own hand. For Turkey – and, for that matter, Europe – a closer Turkish-Russian partnership in energy need not be a zero-sum game. Turkey could provide both a new and reliable transit corridor capable of transporting both Russian and non-Russian gas to Europe in the event of a supply crisis. Turkey therefore has a chance to turn this partnership into a win-win proposition. Its co-operation with Russia could benefit it, Russia and Europe. If so, it could help to allay deep-seated concerns in the Russian-European relationship.

Turkey’s rhetoric about being a regional energy hub and stepping up the efforts for transition to a clean energy economy needs to be effectively turned into tangible actions. How could this happen?

Alignment of foreign/security and energy policies. But being an energy hub is not having pipelines criss-crossing your territory. Turkey’s first priority must be to secure its own supply for its own citizens, uninterrupted, and with affordable prices41. The new Turkish interest in non-western directions has been the outcome of Turkey starting to ‘read’ its neighborhood and energy interests through its own lenses, from where it firmly dwells. Turks are not content only to be a simple “bridge” over which energy flows; they aspire to become a regional “hub,” extracting greater value for the crisscrossing oil, gas pipelines and power interconnections, and turn this role to foreign/security policy gains. Turkey’s external energy outreach starts from China’s north-west province of Xinjiang-Uyghur Autonomous Region and extends to the North African tip of the Mediterranean, as well as from the Straits of Hormous, all the way to the Arctic, where 22 percent of the world’s oil and gas reserves are located. As the virtual boundaries have been removed, Turkey is now facing the East, the North and the South directly. Those who define Turkey’s will to be part of the solution to the problems of the East with its self-formulated prescriptions as a ‘shift of axis in foreign policy’ are falling into the grave mistake of trying to read Turkey based on its erstwhile habits, both in foreign and security policy and in energy equations.

Being a reliable transit/hub country is of paramount importance. No matter what political or economic problems are, Turkey must maintain its credibility as a country over which energy flows will not be disrupted. It has become almost common place for Turkish government leaders to assert that energy transit to Europe via Turkey is not only an economic project but also a Turkish geopolitical project that strengthens Turkey’s hand strategically vis-à-vis Europe and producing regions around it42. Any misuse of Turkey’s energy transit role by the Turkish government for political leverage on the EU could diminish Turkey’s value to the EU43. Overplaying Ankara’s hand could, moreover, cast doubt on Turkey’s reliability as a transit country from a business perspective, quite apart from EU debates and European politics.

Moving towards smarter industries. Many alternative energy advocates claim that it is possible to replace our fossil fuel economy with a cleaner one that runs on a combination of nuclear power and renewable energy from the wind, the sun and the farm. Credible scientific estimates suggest that they are right. However, those advocates often fail to consider one critical issue that could derail their plans, the rate-of-conversion problem. How long will it take to make such a transition?In this context, we should ask ourselves: Is Turkey going to support some of the most effective policy that has yet been deployed for transitioning Turkish business and industry to a clean energy future and away from the dangers of fossil fuel, or will Turkey walk away from the green shoots of this economic recovery to let other nations lead in the coming low-carbon economy? What areas of renewables and alternative fuels can we focus on, and aim to be the leading player on the world stage?

Making important strategic investments in clean energy. Turkey should be a pioneer, rather than a follower, in solar, geothermal and hydro energy technologies. It should extend funding for short-term financing programs, which are proving their worth by jump-starting the development and construction of such clean energy projects. The need to incentivize private capital flow into clean energy development is greater than ever and will become more urgent with time. Financing mechanisms and incentives will evolve as the market demand for clean energy evolves. Exchanging investment risk for upfront cash grants to cover 30 percent of the clean energy project costs makes investing in the development of clean energy projects attractive to investors and is the right boost for the nascent clean energy industry. These short-term financing mechanisms that encourage private capital flow into clean energy must be complemented by policy to enhance domestic manufacturing capacity and productivity. Building a clean energy industry in Turkey not only means more electricity from clean, renewable sources. It also means more high-paying jobs in every region of the country, because clean energy will require us to get to work producing and assembling new technologies on a mass scale.

Energy efficiency improvements are the best energy security investment. We should retool Turkish industry progressively to compete in a low-carbon economy and move away from energy-intensive and “dirty” sectors, such as iron-steel mills, cement, fertilizer and aluminum. We should be able to adopt a specific target to reduce the energy intensity of our economy by at least 2.5 per cent a year. We need to increase the effectiveness of our capacity to implement robust policies, market-based mechanisms, business models, investment tools, and regulations with regard to energy use, and recognize that improvements in energy efficiency remain one of the most effective means of both cutting carbon emissions and improving access to energy. As the EU proposes tighter emissions caps and auctioning of allowances in Phase III of the EU E.T.S., energy intensive industries must demonstrate their level of exposure to external competition in order to qualify for protection, and avoid carbon leakage.

Creating Turkey’s own, internationally competitive “energy champions.” Turkey should re-energize its companies (on their own and in public-private partnership mode), its public energy policy management and external outreach to serve the ultimate goal of making Turkey a regional energy powerhouse in every sense of the word. There is a pressing need to, without further delay, create its own regional energy champions to operate both at home and in neighboring regions. Turkey needs to support the emergence of internationally competitive, corporatized, staffed and financed international oil companies in the style of Petronas, Petrobras, or E.N.I., T.P.A.O., and Botas should possibly be merged under a new corporate identity. Turks are much better placed than most international oil companies to operate in Russia and other countries in the region because of the close political ties at the highest level, and because they know the key drivers and the business culture in these geographies.

Hammering out an integrated energy management and vision. Last but not least, we should see Turkey’s energy policy as a sub-set of a wider government vision encompassing industrial, competition, tax, envrionment, foreign and security, and trade/investment policies. Management structures must be streamlined and made more effective and responsive to the needs of the energy economy, finance and geopolitics. The human capital, too, must be enriched, as at the end of the day, everything boils down to the quality of our people, who can invent new energy technologies and fuels, manage complex policies, and engage with the external world.

Endnotes

• The opinions expressed in this article are only those of the author.

- Russia’s rise as an energy superpower scares the West for the same reason China’s rise does. Both China’s and Russia’s images in the Western psyche as former Communist “red menaces” complicate the picture. Both China and Russia are also seen as abrogating Western notions of economic fair play in the global marketplace with heavy state intervention, as well as engaging in circumvention of international norms concerning contracts and physical and intellectual property.

- “Ensuring Energy Security”, Daniel Yergin, Foreign Affairs, (March/April 2006).

- But if we go back to the origins of diplomacy and the extensive trade that existed in subsequent centuries among the countries and civilizations of Egypt and West Asia, we see that trade provided the first motivation for inter-state contacts and agreements. Another example is provided in the spread of colonialism in Asia, following Vasco da Gama’s journey to India in 1498, and Europe’s “discovery” of the riches of the East Indies. Again the flag followed trade.

- Build Your Fortune BRIC by BRIC The Global Guru, www.theglobalguru.com/article.php?id=307&offer=GURU.

- But per capita income and military comparison will continue to give a different perspective. For example, this year the US defence budget will again be around $600 billion which is larger than the next ten countries combined. If all national security spending was included, that figure would rise to around $800 billion.

- New York - Speech by Benita Ferrero-Waldner, European Commissioner for External Relations and European Neighbourhood Policy, “Energy Security and Foreign Policy”, at the Foreign Policy Association, World Leadership Forum 2008, September 24, 2008.

- Andrea Bonzanni, “Paradigm Change Needed in EU-Russia Energy Relations”, World Politics Review, May 25, 2010.

- Mandil, C., The Energy Future International Oil and Gas: Financial Review 2007. M. Crisell, Euromoney International Investor PLC 1-3.P1.

- Lo, B. And A. Rothman, “China and Russia: Common Interests, Contrasting Perceptions Asia Pacific Strategy”, Asian Geopolitics Special Report, CLSA Asia-Pacific Markets: 1-31 p. 13, 21.

- “The new seven sisters: oil and gas giants that dwarf the west’s top producers,” Financial Times, March 12, 2007.

- According to EIA, the world oil demand could reach to 99million barrels per day in 2015, and 116 million per day in 2030, up from 84 million per day in 2005.

- A recent study measuring the shift in power in global energy markets revealed that seven major state controlled energy corporations from non-OECD countries (i.e. Saudi Aramco, Gazprom, PDVSA, China’s CNPC, Iran’s NIOC, Petrobras of Brazil and Petronas of Malaysia) presently control over 30 percent of global oil and gas production and over 30 percent of reserves, while the original seven (now four - ExxonMobil, BP, Chevron, Shell) OECD-based energy blue chips which have dominated global energy markets since World War II now control just 10 percent of production and 3 percent of reserves.

- Javier Blas and Ed Crooks, “Drive on Biofuels Risks Oil Price Surge”, Financial Times, June 6, 2007.

- The capital required to meet projected energy demand through to 2030 in the Reference Scenario is huge, amounting in cumulative terms to $26 trillion (in year-2008 dollars) — equal to $1.1 trillion (or 1.4 percent of global gross domestic product) per year on average.

- Sino-Indian cooperation in the search for overseas petroleum resources: Prospects and implications for India, J. Nandakumar, International Journal of Energy Sector Management, 2007, 1 Issue: 1, 84–95, Emerald Group Publishing Limited.

- “Power plays: Energy and Australia’s security”, Australian Strategic Policy Institute, October 11, 2007.

- “Climate change may spark conflict with Russia”, EU told, Ian Traynor, The Guardian, March 10, 2008.

- The Oil Drum, April 5, 2010, retreived from http://www.theoildrum.com/frontpage.

- Mathew Maavak, “Globocops of energy security”, The Korea Herald, July 18, 2006.

- Energy security may be achieved when a state is able to minimize vulnerability to resource supply disruptions, access reliably energy at reasonable and/or market-driven prices, and consume resources that least damage the environment and/or promote sustainable development.

- The port of Ceyhan has become an important outlet for both Caspian oil exports as well as Iraqi oil shipments from Kirkuk. Turkey is seeking to build up Ceyhan as a regional energy hub, with private investors receiving approval to build several refineries at the oil terminal. The Kirkuk-Ceyhan pipeline has a capacity of 1.65 mbd.

- Several other possible Bosporus bypass options are being examined, some of which do not involve Turkey. One proposal that has received significant attention is a pipeline that would pump crude oil from Bulgaria’s Black Sea port of Bourgas to Greece’s Mediterranean port of Alexandropoulos, known as the Bapline project.

- “Making sense of the current phase of Turkish-Russian relations,” Igor Torbakov, Jamestown Foundation Occasional Papers, October 2007.

- Mehmet Ogutcu, “Shall we carry on accession talks with the EU?”, Today’s Zaman, December 8, 2008.

- “2009 sees significant recovery in foreign trade deficit”, Today’s Zaman, February 5, 2010.

- See www.oecd.org/eco/surveys/turkey.

- In this part of the paper, much use has been made of “Turkey’s role in European energy security” by Katinka Barysch, CER, (December, 2007), retrieved from http://www.cer.org.uk/pdf/essay_turkey_energy_12dec07.pdf.

- Although Turkey has spent billions on high-tech navigation systems and other safety features, maritime experts say that it is only a matter of time before one of them spills its toxic cargo. This would be a disaster for Istanbul’s 13 million residents. And a big headache for the transporting companies that run up costs of tens of thousands of dollars for every day that one of their tankers’ crossings is delayed. Turkey and the other Black Sea countries have been looking at a number of bypass options.

- “Gates Says EU Pushed Turkey Away”, Wall Street Journal, June 10, 2010.

- EU-Turkey relations in the Field of Energy, Directorate General External Policies of the Union, Policy Department.

- Katinka Barysch, “Turkey’s role in the European Security”, CER, (December, 2007).

- “Is Turkey Shifting Alliances?”, Energy Hedge Fund Syndicate, December 15, 2009.

- Mehmet Öğütçü and Danila Bochkarev, “Turkey and Russia: Rivals become partners?”, European Voice, September 21, 2009.

- Stephen F. Larrabee, “How Turkey is re-discovering its Middle East role”, Europe’s World (Autumn, 2009).

- “Turkey broadens foreign policy vision beyond its region”, Today’s Zaman, May 30, 2010.

- M K Bhadrakumar, “Russia, China, Iran redraw energy map” Jan 8, 2010, retrieved from http://www.atimes.com/atimes/Central_Asia/LA08Ag01.html.

- In July 1996, the Erbakan government concluded a $23bn natural gas deal with Iran. The deal provided the framework for the long-term delivery of Iranian natural gas to Turkey for the next 25 years and created strains in U.S.-Turkish relations because it directly undercut U.S. efforts to constrict trade and investment with Iran. In the decade since then, energy ties have continued to expand.

- Mehmet Öğütçü, “Iran: Turkey’s next door, but far-away, neighbor (1-2)” Today’s Zaman, April 17, 2008.

- On other matters, especially the Iranian nuclear issue, U.S. and Turkish approaches are much closer. Like the United States, Turkey is opposed to Iran’s acquisition of nuclear weapons. While Ankara does not perceive a serious military threat from Iran, Turkish officials fear that a nuclear-armed Iran could spark a regional arms race and force Turkey to take compensatory measures to ensure its own security. In the short term, Turkish concerns about a nuclear-armed Iran could increase Turkish interest in missile defence. But if relations with the United States and NATO were to seriously deteriorate, Ankara might then feel the need to consider acquiring a nuclear deterrent of its own.

- “Turkey, Iran to expand gas ties”, Feb. 4, 2010, retreived from http://www.upi.com/Science_News/Resource-Wars/2010/02/04/Turkey-Iran-to-expand-gas-ties/UPI-39741265301600.

- Delphine Strauss, “Turkey needs suppliers to fuel energy hub role”, Financial Times, June 11, 2010.

- “Erdogan, Putin: Israel won’t get our gas”, Bloomberg, June 8, 2010.

- During one of his visits to Brussels, Prime Minister Erdogan implied that Turkish support for Nabucco would be conditional on the EU accelerating the negotiations toward Turkish membership in the EU. He even implied a possible linkage between Turkish support for Nabucco and the EU’s position on Turkey’s disputes with Cyprus. Most recently, Prime Minister Erdogan said that the government shelved a plan to export natural gas to Israel via a new Blue Stream-II pipeline, in retaliation to the Gaza episode. In Brussels, supporters and opponents of Ankara’s integration with the EU are bound to feel irritated by Ankara’s use of the “energy trump card.” Opponents, mostly in Western Europe, are growing more resentful over Ankara’s delusion that it can pressure the EU. Supporters, mostly in Central and Eastern Europe, are growing frustrated with Ankara’s stalling on the Nabucco project, which this group of countries particularly values.