Turkmenistan, with the world’s fourth largest reserves of natural gas, is destined to play a crucial role in Eurasian energy security calculations. Future natural gas exports from Turkmenistan to Europe will not only bring about some technological advancement such as a platform ‘tie-in’ pipeline connecting two fields in the Turkmen and Azeri sectors but will also stimulate the conclusion of a long-term contract for building the Trans-Caspian Pipeline project and compressed natural gas (CNG) and liquefied natural gas (LNG) transport options. The equation of Turkmenistan’s natural gas relations with regional powers has somewhat changed after the Turkmen-Russian gas crisis in 2009, which led to new dynamic market relations in the Caspian Sea region. Turkmenistan has launched a novel energy policy focusing on diversifying energy export routes and encouraging foreign direct investment to explore its vast natural gas resources.

This paper will first review Turkmenistan’s energy picture and present Azerbaijan’s position as “a transit country” for Turkmen and possibly for Kazakh natural gas. This paper also recognizes Georgia’s essential network role for Azerbaijan, and for the Baku-Tbilisi-Erzurum (BTE) pipeline project. Even though Azeri gas will be transported in additional volumes from Shah Deniz Phase I and II (SD-1 and SD-2) and then Turkmen gas will be added to the Southern Corridor, this is still a small portion of the Caspian Sea region production; however, this gas supply plays a critical role in boosting Eurasian energy supply and also assigns to Azerbaijan a transit country role.

Secondly, the paper emphasizes how the Euro-Atlantic vision of Turkey will materialize in three projects, namely Nabucco, the Interconnector Turkey-Greece and Italy (ITGI) and the Trans Adriatic Pipeline (TAP). The European Union also presents the White Stream natural gas sea-bed pipeline project going through Azerbaijan-Georgia and the Ukrainian transit networks to Europe as a “counter-balance” to “the Turkey factor.” Similarly, the Azerbaijan-Georgia and the Costanzia LNG trade are designed to by-pass Turkey by using transport on the Black Sea to reach the European energy market.

Thirdly, the paper gives an insight into how the relative geopolitical gains of Turkey are going to be checked against the long-term contract opportunities between natural gas suppliers and transit countries. For instance, the recent natural gas agreement between Azerbaijan and Turkey provides a new vision to Ankara as “an energy hub” country in the Eurasian energy environment.1 Turkey already does transport natural gas from the Caspian region to the European energy market.2 We will outline the role of the Caspian Sea natural gas supply and its transport security on the grounds that efficiency and the mutual dependency regulatory principles support the role of Turkmenistan and Azerbaijan as transit countries to Europe. The paper gives some implications on the EU’s Caspian Development Corporation, which could be one feasible option to bring Turkmen gas to Europe. Finally, the paper will introduce the five possible scenarios which basically give realistic options for natural gas supply and transport to EU.

Turkmenistan’s Natural Gas Outlook

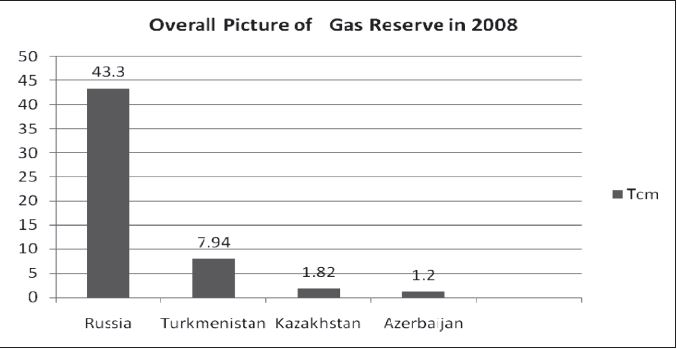

Despite ongoing discussions about the exact size of Turkmen gas reserves, the country has undoubtedly significant gas resources – the highest in the whole region after Russia. Further exploration offshore in the Caspian Sea should further add to reserves in the future.3 The majority of reserves are located in the east (72%), but there are also sufficient reserves in the west (28%) of Turkmenistan. The proven natural gas reserve of the country is approximately 7.94 trillion cubic meters (TCM) in 2008.4 The largest natural gas fields are in the Amu Darya basin, with perhaps half of the country’s natural gas reserves located in the giant Dauletabad-Donmez field. In addition to Amu Darya, Turkmenistan contains large natural gas reserves in the Murgab basin, particularly the giant Yashlar deposit. During the last 10 years, Turkmenistan also has discovered 17 new natural gas deposits in the Lebansky, Maryinsky, and Deashoguzsky regions of the country.5

The problem for Turkmenistan is that the areas are not linked by pipelines and serve different markets. Therefore, the East-West Pipeline project is an important one to connect the east and west of Turkmenistan.

Source: BP Statistical Review (proven resources at end 2008)

Source: BP Statistical Review (proven resources at end 2008)

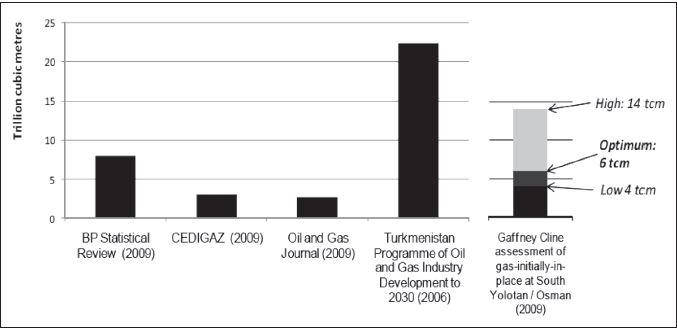

There was a speculative dispute in the Gaffney, Cline and Associates’ (GCA) report on the estimation of Turkmenistan’s South Yolotan-Osman gas field, one of the world’s largest. The consulting firm’s low estimate for the field as 4 TCM and the high estimate was nearly 14 TCM.6 The optimum estimate of 6 TCM would make South Yolotan-Osman one of the five largest gas fields on earth. It would also make it approximately five times larger than the Dauletabad gas field, previously believed to be Turkmenistan’s largest, with 1.4 TCM.7 However, the Russian newspaper Vremya Novostey criticized the report as GCA did not actually produce their own data but based their estimations on the same possibly spurious Turkmen data.8

The World Energy Outlook 2009 report evaluates the new discoveries in the South Yolotan-Osman and Yashlar fields as the most significant reserve reappraisals, amounting to over 6 TCM. In addition, CEDIGAZ provides a figure of 3 TCM for Turkmenistan gas reserves in 2009 (up from 2.68 TCM in 2008) while BP in 2009 revised its estimate from a similar starting point up to 7.94 TCM; these are still lower than Turkmenistan’s own estimates, which are in excess of 20 TCM.9

Source: Ambassador Richard Jones “The Politics of Central Asian and Caspian Energy” Chatham House, February 23-24, 2010.

Source: Ambassador Richard Jones “The Politics of Central Asian and Caspian Energy” Chatham House, February 23-24, 2010.

The World Energy Outlook 2009 also projected that Turkmenistan will likely supply 2.4% of the world’s natural gas production in 2007-2030.10 The production of natural gas in the four Caspian producers (Azerbaijan, Kazakhstan, Turkmenistan and Uzbekistan) is projected to grow from 180 billion cubic meters (BCM) in 2008 to almost 220 BCM in 2015 and 310 BCM in 2030, making a significant contribution to production growth in Eurasia.

According to the World Energy Outlook 2009, Azerbaijan, Kazakhstan, Uzbekistan and Turkmenistan produced 11 BCM, 30 BCM, 65 BCM and 69 BCM of natural gas respectively. Natural gas reserves in Turkmenistan are more than sufficient to support an expansion in gas production and export in comparison to the other Central Asian countries.11

Due to free consumption in the domestic market of Turkmenistan, the country has had the fastest consumption growth in the region, averaging 16.1% annually from 2000 to 2006, as compared with 6.3% per year for the rest of Central Asia. For instance, in the high case, consumption grows from 16.9 BCM in 2009 to 21.9 BCM.12 Of the 71 BCM produced in 2008, just over 50 BCM was exported, primarily to Russia but also to Iran. The Turkmenistan government has ambitious targets to raise production to 250 BCM per year by 2030, of which 200 BCM would be exported. Turkmenistan’s total revenue from gas export in 2008 was $6.2 billion in 2009 and this is the main source of Turkmenistan public sector spending.13

The Turkmenistan government has ambitious targets to raise production to 250 BCM per year by 2030, of which 200 BCM would be exported

Russia provides the route to market for over 85% of the gas exported from Kazakhstan, Turkmenistan and Uzbekistan. This dependency relationship between Russia and Central Asian natural gas suppliers has become a major source of contention on the pricing issue when European gas demand is weak.14 Turkmenistan was a substantial natural gas producer under the Soviet Union, but after the country became independent, Turkmen natural gas became a competitor with Russian natural gas. Since Turkmenistan’s only natural gas export routes ran through Russia, Gazprom limited Turkmen natural gas exports, and as a result Turkmenistan’s natural gas production sagged throughout the 1990s. Following the resolution of a pricing dispute with Russia in 1998 and the construction of an export pipeline to Iran, Turkmenistan’s natural gas production began to climb steadily.

It should be noted that although Turkmenistan has huge reserves, another key problem is how production will be mobilized. The current investment regime is not so conducive to foreign investment. International oil companies (IOCs) are allowed to have production sharing agreements (PSAs) only on offshore fields – which are not as attractive – while onshore fields are open to technical service contracts only.

Turkmenistan’s Energy Economy

The proven and otherwise probable hydrocarbon riches of Turkmenistan, spanning from the sizeable offshore Caspian fields in the west to the Amu Darya basin reserves bordering Uzbekistan in the east, are by now quite clear. The worldwide exploration and production (E&P) industry has been entering this new game with enthusiasm.

There is indeed little reason to doubt the intention of the new Turkmen leadership to boost the country’s revenues from the exploration of its vast gas reserves. The key question is not the gas extraction in itself but its transportation to markets. Turkmenistan’s government is under a pressure to choose between a Russian-sponsored Caspian pipeline and the EU-advocated Trans-Caspian pipeline, in addition to the existing outlets to Russia and soon China. The new government apparently hopes that the country’s gas resources will allow it to tread a middle path, as Kazakhstan is striving to do; others must be hoping for that, too.

Turkmenistan’s government is under pressure to choose between a Russian-sponsored Caspian pipeline and the EU-advocated Trans-Caspian pipeline

Foreign investment in Turkmenistan on a large scale is needed in order to raise gas production to the point that would justify the construction of new pipelines, although potential Western investors, in particular, will want to see a trans-Caspian route in place before they invest so that they have some assurances of being able to monetize their gas production.

Turkmenistan is not only a gas producer but is also the fourth largest producer of oil and condensate in the former Soviet Union after Russia, Kazakhstan and Azerbaijan. From the mid-1980s to the late-1990s, its liquids production averaged around 100,000 barrel per day (b/d). Since 1998, it has been increasing production, although not as quickly as official targets. The state sector’s contribution has been in steady decline since 2003 and based on current developments, this is likely to continue. In 2007, Turkmen oil production was expected to total just over 200,000 b/d.

Turkmenistan plans to become one of top 20 world oil producers by 2030. According to its development program, reserves would be increased by 26 billion barrels and crude output increased 11-fold through hugely expanded development and exploration programs. Such an aggressive plan does not stand up to critical assessment. Turkmenistan’s ambitious forecast will inevitably be constrained by a range of factors, including basin geology, exploration risk, drilling capabilities, export capacity and a much slower pace of investment.

Turkmen President Berdymukhammedov repeatedly refers to the oil and gas sector’s 2030 Development Plan., a throwback to the former president Niyazov era – it was first presented in 2006 as an offshoot of the “Economic, Political and Cultural Development Strategy to 2020”. President Berdymukhammedov sees the 2030 Plan as a valuable policy guidance tool.

There are two strategic priorities set out in the 2030 program:

- Ensuring Turkmen energy resources have access to new markets (including refined products) through a multi-vector gas transportation system;

- Implementing modern technologies to improve oil and gas production. The Turkmen government acknowledges the need to import expertise and machinery for exploration and deep drilling to meet production targets.

The 2030 program explicitly states that the Caspian Sea shelf with be developed jointly with foreign companies through PSAs “under the supervision of Turkmenneft”, the state oil company. The onshore priority regions for technical assistance service contracts are in western Turkmenistan (the Keimir area, Kum Dag, and Esenguly) and southeastern Turkmenistan (Dauletebad, Yashlar, the right bank of the Amu Darya, and Yoloten-Osman). The government stated that IOCs would be able to develop oil deposits onshore, but not gas deposits. How will this differentiation be upheld in practice? This rule was the basis for the Sinopec, Changsi Oil and Chalyk Energy contracts to drill at Yoloten.

Macroeconomic Context

Turkmenistan’s future economic growth is undoubtedly dependent on the new government’s success in exploiting the country’s energy potential. Regional examples show the impact of successful development of the oil and gas sector on the standard of living and GDP of Kazakhstan and Azerbaijan. Berdymukhammedov’s new policy of welcoming foreign investors and opening Turkmenistan for business is a step towards attracting the external investment that could revitalize the sector.

However, major challenges remain in creating a workable legal framework, transparent legislation and a true market economy. While the state program, which outlines the government’s strategy for the industry’s development, is useful in mapping the high-level objectives for the energy sector, the production targets are generally unrealistic. Turkmenistan has a track record of setting over-ambitious targets for oil and gas output and this appears to be more of the same. Already, delays in securing agreements and investments for large-scale exploration and development projects are causing the plan to fall behind schedule.

Despite this, Turkmenistan has good prospects for new discoveries and continued growth in oil and gas production, beyond the levels promised by current developments. International companies recognize this potential and are expected to invest if the right legislation and fiscal systems are in place. Their ambitions are likely to be far more modest than those in the official development plan.

Turkmenistan has made the slowest transition progress in reforms of all the countries in the region. Following independence in October 1991, the Turkmen economy contracted sharply at an annual average rate of 9% until 1998, when positive growth was first recorded because of the resumption of gas exports to Russia. The Asian Development Bank, one of the few international organizations active in the country, estimated that GDP is growing at around 6–9% per year.

The economy remains heavily centralized, and although the new president Berdymukhammedov has shown some signs of slowly shifting course from that of Niyazov, the implementation of any sort of substantial market-oriented economic policies is not to be expected in the foreseeable future.

Turkmenistan is vulnerable to fluctuations in world cotton and grain markets and has periodically been heavily affected by the non-payment of gas exported to Ukraine. Turkmenistan’s isolated position and limited range of export products has restricted its participation in international trade; however, the main basis for vigorous growth in the country has been the development of energy production, in particular natural gas.

Only a few state-owned enterprises have been privatized, and the government remains in firm control of production and exports of gas, oil, and cotton, as well as some other industries. Foreign competition is hampered by significant non-tariff barriers, and as such there is little space for private business interests.

Modernization and expansion along the main routes and in the most visible urban centers is under way, but these showcase projects do little to hide inadequate infrastructure in other parts. Operations are complicated by the fact that 90% of the country is desert. The workforce is cheap and quite highly skilled, though education levels have dropped dramatically since the country’s independence from the Soviet Union.

Investment Climate Issues

Until December 2006, oil and gas policy in Ashgabat tended to be made by presidential decrees issuing from the reclusive and idiosyncratic Niyazov. Now there are positive signs of change, with the advent to power of Berdymukhammedov. It seems that the new Turkmen administration is considering new policy options in its gas production and marketing strategy.

But there is clearly a long way to go to eliminate operational difficulties. Bureaucracy, high-level corruption and the need for “inside contacts” are day-to-day elements of business life, although one should recognize that the investment climate has visibly improved in a short space of time, albeit only in comparison to the low standards of the Niyazov regime.

Although modest steps have been made in addressing these shortcomings thus far, more substantial non-retractable structural reforms are not yet on the immediate horizon. The authoritarian nature of the Turkmen leadership, the country’s distance from lucrative markets in Europe, its limited energy export options, and lack of institutional/human capital development remain major deterrents to foreign investors.

Turkmenistan’s track record for licensing new exploration acreage is poor. Its most recent official offering in October 2001 included 15 onshore and 32 offshore blocks but resulted in no license awards. Between 1996 and 2006, only one license was awarded on an ad hoc basis (offshore Blocks 11 and 12 to Maersk in 2002). This ad hoc licensing policy is continuing under Bermukhammedov, with a recent award to CNPC for gas exploration and production in the Amu Darya region.

Many of the prospective offshore blocks lie in the areas disputed by Azerbaijan and Iran. Although Turkmenistan has recently begun negotiations with Azerbaijan concerning the status of the Serdar (Kapaz) prospect, it is unlikely to reach an agreement with Iran in the foreseeable future.

On the surface, Turkmenistan’s legal framework is friendly to investors, but in fact most deals are still done on a personal basis and corruption remains a problem. Foreign investment legislation has evolved much more slowly in Turkmenistan than in other former Soviet republics. The main laws relevant to foreign investment are:

- The Law on Foreign Investment, amended in 1993, protects investors which own at least 20% of the capital in a company for a minimum of 12 months.

- The Law on Foreign Concessions was introduced in 1993 and covers the exploration and development of natural resources such as oil and gas. Concessions from five to 40 years are granted on a competitive basis.

- In addition, foreign investors also enjoy a number of privileges, such as tax holidays, freedom from currency surrender requirements and settlement in free economic zones.

Berdymukhammedov has vowed to accelerate economic reforms. He said at a government meeting on September 10, 2009 that Turkmenistan needs “an absolutely different pace of growth” in order to “move closer to developed countries and give our people a better life.”15 He urged his cabinet to stimulate economic growth and restructure state corporations. His election platform included promises to create a friendly environment for foreign investors. Among his plans was the construction of a natural gas pipeline to China by 2009, the creation of free-trade zones in border areas in the southern Balkhan Province, and the completion of the Amu Darya railroad bridge in Lebap Province.

It is still not clear how genuine Berdymukhammedov’s intentions to liberalize the economy are and how far he can go in his reformist attempts within the current political system. Experts note that many members of the Turkmen political elite have benefited from the current economic system and therefore will try to maintain the status quo. So far, few — if any — foreign companies dealing with the Turkmen government have shown an inclination to insist either on adherence to free-market principles or respect for human rights.

Political Context

It is highly likely that Turkmenistan will continue developing along an authoritarian path, but international relations will depend on how the new leadership will play a balancing act between China, Russia, Iran and the West in order to maximize the benefits (as Kazakhstan is currently doing through its multi-vectoral policies) and preserve the country’s neutrality.

The new government’s rhetoric is a cause for hope, although it is too early to say to what extent this rhetoric will be put into practice and at what speed. It is unclear exactly how the new government will organize itself, what sort of decisions it will take, and how it will move forward. Policy and decision-making are in a constant state of flux. Despite multiple scare-mongering reports by media outlets and political risk consultancies, some of whom grossly overestimated the potential for violence immediately following Niyazov’s death, the fact that consensus-based negotiation takes place on most issues is positive. This suggests a more realistic approach to the creation of policy and engagement with the outside world.

Regarding the prospects for the new regime becoming more democratic, outward looking and progressive, this remains unclear, but Berdymukhammedov’s new government has thus far adopted a style which eschews Niyazov-style excesses, and is progressing through a gradual but slow down-shifting process from dictatorship to authoritarianism. The government is sending out the right signals, saying the right things, and making positive overtures. The bottom line is that there is far more chance of a more progressive and relatively liberalized Turkmenistan today than there was on December 20, 2006.

It would be a mistake to assume a quick and easy transition to economic and political reforms or to assume inevitable state collapse or revolution. Berdymukhammedov has already moved to consolidate his own power in what has proved a smooth leadership transition, yet there is hope that the situation will change for the better, as the new president seeks to push through some limited reforms. Constitutionally, the power of the president is very strong in Turkmenistan. Written under the supervision of Niyazov, the constitution grants the president the role of prime minister and control over the armed forces. All legislation must be ratified by the president, and he is entitled to legislate by decree.

There are two parliamentary bodies, the unicameral People’s Council (Halk Maslahaty), the supreme legislative body which meets at least once a year, consisting of up to 2,500 delegates, some of whom are elected by popular vote and some of whom are appointed. Secondly, there is the Assembly (Mejlis), whose members are elected by popular vote to serve five-year terms. The ruling party continues to enjoy an overwhelming majority in both legislative bodies, due to elections that are usually undisputed and allegedly rigged. In practice, the democratic aspects of the constitution are not applied, and the president’s power is foremost.

The main source of uncertainty in the country at present is the divisions within the ruling elite, and the competition between regional and ethnic clans, which are likely to transpire in the medium term. Opposition parties are outlawed, but some continue to work in exile, notably the United Turkmen Opposition and the National Democratic Movement of Turkmenistan, headed by Boris Shikhmuradov and Abdy Kuliyev respectively.

The question is whether and how fast the old guard will be replaced by new young personnel who have experience of international business standards, the rule of law, and good governance. The pace of future change will be determined by the rate of installation of new young outward-looking officials. Sackings and appointments should therefore be used as signposts for future trends.

Key Energy Organisations and Executives

The governmental institutions charged with managing the energy sector are:

- The State Fund for the Development of the Oil and Gas Industry and Mineral Resources: Oversees investment and receives a substantial share of revenues generated by the sector.

- The State Agency for Oil and Gas Management and Use: The key intermediary for foreign investment. Negotiates and approves licenses, and enters into exploration and production-sharing agreements. Replaced the previously dissolved Competent Body for the Exploitation of Hydrocarbon Resources.

- The Ministry of Oil and Gas Industry and Mineral Resources: Plays a supporting role in the development of strategy for the sector.

- Turkmenneftegaz: Controls the export, domestic marketing and distribution of natural gas. Also responsible for oil refining, domestic petrol distribution and the export of oil and oil products. Purchases gas from Turkmengaz and oil from Turkmenneft.

- Turkmenneft: Produces oil in the west of Turkmenistan

- Turkmenneftegazstroi: The construction company for the oil and gas sector

- Turkmengeologi: Deals in hydrocarbon exploration

The Caspian Sea Dispute

Following the breakup of the Soviet Union, a dispute began over the maritime borders of the Caspian Sea. Turkmenistan, Russia, Iran, Kazakhstan and Azerbaijan, the littoral states surrounding the Caspian Sea, have yet to come to an agreement over the borders. The dispute essentially revolves around whether or not the Caspian has the legal status of a lake or an inland sea; the former implying that the waters should be divided out in their entirety in proportion to coastline length, and the latter denoting that there should be a central area of the Caspian which has international status.

Turkmenistan’s dispute with Azerbaijan over the Serdar/Kapaz field in the southern Caspian is one example of how the lack of agreement on maritime borders has kept fields from being developed. Azerbaijan has chosen to proceed with hydrocarbon resource exploitation in its national sector of the Caspian regardless, having recently drilled the deepest gas well in the waters at its Shah Deniz field. Turkmenistan will need to strike a deal with Azerbaijan on their maritime border in the Caspian before any subsea pipeline linking the two countries is built, and even then Russia and Iran may raise objections if there still is no multilateral agreement on the division of the sea’s resources and its legal status. A resolution to the dispute is still a long way off, but until then Turkmenistan will be deprived of its proposed new export route.

Courting International Investors

Many foreign companies have expressed interest in investing in Turkmenistan’s energy sector, most recently during the Turkmenistan International Oil & Gas Conference

- Dragon Oil (UAE): has a 100% interest in, and is both operator of and the holder of the PSA for the offshore Cheleken Contract Area, with an average production of 28,321 b/d in the first half of 2007. The company has four wells completed, three development wells and one appraisal well. A further development well was to be completed in July 2007. The company’s total capital expenditure stood at over $100 million in the first half of 2007, which includes expenditure on infrastructure development and drilling. Dragon Oil has exported some of its crude oil production through a swap deal with Iran since 1998, and in April 2000 the company signed a new 10-year swap agreement with Iran.

- Burren Energy (UK): is producing oil from its onshore Nebit Dag block. Gross production in the first half of 2007 was 21,800 b/d compared with an average of 19,940 b/d in 2006. Three drilling rigs are currently in operation (two deep, one shallow) alongside four workover rigs, all owned by Burren. An additional workover rig has been purchased.

- Maersk Oil (Denmark): In 2002, Maersk Oil, entered into an exploration and production sharing agreement for Block 11-12, covering some 5,700 square km offshore Turkmenistan in the Caspian Sea. Exploration activities are in progress. Maersk Oil holds an interest of 80% and is the operator and Wintershall holds the remaining 20%.

- Petronas (Malaysia): has interest in Block 1, south Caspian Sea. It is involved in exploration, development and production. Petronas began producing around 10,000 b/d from the Diyarbakir field in mid-2005.

- Mitro International (onshore): established in 2000 to operate in the oil and gas sector, particularly in deposits scanning and exploration development. The company has contractual rights and obligations on the PSA Khazar project, and became a full member of the long-term oil and gas project.

- Buried Hill Energy (Canada): expects to enter into a PSA with the government of Turkmenistan.

- Shell: Shell and OMV have teamed up with the International Petroleum Investment Company — the investment vehicle of the Abu Dhabi government — to investigate the possibility of conducting exploration in Turkmenistan. Shell has recently opened an Ashgabat office.

- BP, Glencore International, Swiss Vitol, Argomar Oil of Austria and the Japanese heavyweight Itochu have also expressed interest in doing business in Turkmenistan. BP intends to enter in a big way and was the principal sponsor for TIOGE. BP executives undertook four missions in 2010 this year to Ashgabat.

The Russia-Turkmenistan Natural Gas Crisis

The Turkmen-Russian gas crisis on April 9, 2009 started after an explosion took place at kilometer 487 of Central Asia Centre (CAC)-IV pipeline, just inside Turkmenistan close to the Uzbek border, and has changed Turkmenistan’s energy strategy. The some 27 hours after Russia first called for a reduced flow, the pipeline burst. Although Turkmen technicians fixed the line within a few days, Russia […] declined to resume deliveries through the line.16 Turkmenistan claims that due to Turkmen’s unwillingness to give up on the East-West pipeline, Russia stop taking natural gas from Turkmenistan, then the CAC-4 exploded with the high pressure gas being pumped along the Turkmenistan-Uzbekistan border. Russia does not accept the accusation of Turkmen side.17 They argue that there is a need to make a proper investigation into the incident and that it was a technical problem as Turkmenistan’s pipeline system is too old and does not have enough capacity to pump the large amounts of gas that was being sent.18

Turkmenistan infrastructure has no capacity to transfer its gas from the east (Yolatan) to the west (Caspian Sea). According to the Gazprom-Turkmenistan gas deal in 2003 and 2005, Russia guaranteed to buy 80 BCM, plus an optional 10 BCM, of natural gas from Turkmenistan. Due to low demand in the EU, Russia halted its gas trade with Turkmenistan. It was resumed on January 9, 2010, which meant there was virtually 0 BCM off-take by Russia in the aftermath of the explosion. The new agreement only guarantees 30 BCM of natural gas from Turkmenistan until 2028. However, Russia can only buy 10-12 BCM in 2010.19

Due to the April 2009 incident, Turkmenistan refrained from developing a further dependency relationship with Russia. For instance, Turkmenistan does not want Russian investment in its domestic trunkline East-West pipeline project (900 km) from Yolatan to the Caspian Sea. In addition to this, due to the distrustful relationship between Russia and Turkmenistan, the new project deal in 2007 on the East Caspian Pipeline known as the Prekaspiiski project was postponed. The project was aimed at increasing the capacity of the pipeline from 20 BCM by 10 BCM. In addition to CAC-1, CAC-2, CAC-3, and this new pipeline was needed to pump the 80 BCM to Russia under the earlier contract.

The incident made the Ashgabat government look at the other transportation options in the region. Two regional players, Iran and China, have enhanced their regional influence and their ties by signing long-term contracts with Turkmenistan. In the Caspian region the two parties have either expanded the capacity of existing pipelines, especially for Iran, or built new pipelines, such as by China.20 A renewed pipeline system could transport 80 BCM to Russia if the project became reality.

Before the April 2009 gas crisis, Turkmenistan exported 52 BCM natural gas to Russia (45 BCM) and Iran (7 BCM). During 2009, Russia only bought 12 BCM while Iran remained a reliable customer. After the gas crisis, natural gas trade with China started. The Central Asia-China pipeline is expected to deliver 5.5 BCM in 2010 and will be increased to a maximum capacity of 30 BCM (plus 10 BCM from Kazakhstan) by 2020. In addition to Chinese involvement in the region, the capacity of the Western Iran pipeline, 8 BCM, was increased. The inauguration of the Eastern Iran connector, 6 BCM, in December 2009 increased the Turkmenistan-Iran natural gas trade to 14 BCM in 2010.21

Turkmenistan-China Gas Relations

The natural gas relations between China and Turkmenistan started with signing of pipeline construction project for a long-term gas supply deal on April 3, 2006. The Turkmenistan-China gas pipeline measures about 1,833 km (188 km in Turkmenistan, 530 km in Uzbekistan, and 1,115 km in Kazakhstan), connecting the Bagtyyarlyk, Saman-Depe, and Altyn Asyr gas fields in Turkmenistan to Alashankou in China’s Xinjiang province, where the pipeline connects to China’s partially completed Second West-East Gas Pipeline. At the plateau level China will import 30 BCM of Turkmen gas (plus 10 BCM Kazakh gas) from the Amu Darya field in the east of Turkmenistan. The Turkmen president defined the project as the “pipeline of the century”.22 The implementation of the Turkmenistan-China pipeline project serves as an example of relations based on equality and a mutual awareness of the benefits that will be created from the start of the practical implementation of this project. Turkmenistan agreed to award the $10 billion contract to develop the South Yolotan field to China, South Korea, and the UAE).Sohbet Karpuz stressed that “Southern Corridor has not started to play the opera in western Caspian but we already hear Chinese symphony from eastern Caspian”.23

The high dependency on Turkmen gas in China and Iran will allow Turkmenistan to set a price in line with European market prices for these countries as well

Russia’s gas relationship with Central Asian is changing dramatically. The Kremlin would rather Turkmen gas went to China than to Europe, but Russia’s future exports to China may compete with Central Asia’s gas on price. Karbuz emphasizes the role of new regional actor, China in Central Asian natural gas market. He said that “Instead of talking the talk, China was walking the walk”.24

Turkmenistan-Iran Natural Gas Relations

Turkmenistan will increase gas sales to neighboring Iran to 14 BCM a year from the current 8 BCM after the building of the Devletuabad Serakhs-Khangiran pipeline in the east which increases export capacity by 6 BCM a year. The two sides have also discussed the possibilities of further increasing supplies to Iran to 20 BCM. The capacity of the Korpedje-Kord Kuy pipeline in the west will reach at least 14-14.5 BCM, from the current capacity of 8 BCM. Iran wants to sell Turkmen gas to Turkey by using the existing natural gas pipeline which has a 27 BCM transport capacity: Turkey is only buying 8 BCM from Iran, which will increase to 10 BCM. It is important to note that the Turkmenistan-Iran trade from the western pipeline is equally balanced, 8 BCM from Turkmenistan to Iran and 8 BCM from Iran to Turkey.25

In conclusion, Turkmenistan’s role in supplying gas to China and Iran will grow this decade. China will meet 4.6% of its natural gas demand with Turkmen supplies in 2010, increasing to nearly 15.4% in 2015. Iran will also depend heavily on Turkmen gas imports during 2010-15, with almost all new Iranian gas projects, especially in the South Pars, delayed.26 The high dependency on Turkmen gas in China and Iran will allow Turkmenistan to set a price in line with European market prices for these countries as well. High-priced Turkmenistan gas will signal to other Central Asian gas producers such as Uzbekistan and Kazakhstan to expect a higher value for their gas in Asia as well, prompting them to set higher gas prices on any potential export projects.

It is clear that the new export plans and agreements have changed the geopolitical power balance in the region. While China and Iran have strengthened their positions, Russia struggles, and the West is losing. At the one end, the strategic engagement of Russia and China in the region serves their geopolitical interests, which rejects the unipolar world under US domination. In the Caspian Sea region, their interests in the region will not clash as long as China’s main priority remains economic and Russia’s political.

The geostrategic position of Azerbaijan gives it the ability to develop a significant gas export capability to Europe via Turkey

Azerbaijan as a Transit Country

According to the Oil and Gas Journal, Azerbaijan has proven natural gas reserves of roughly 850 BCM as of January 2009. In 2008, Azerbaijan produced 12.5 BCM of natural gas and consumed 9.15 BCM, almost all being produced from offshore fields.27 Azerbaijan became a net exporter of natural gas in 2007 with the start-up of the Shah Deniz natural gas field; previously it had been importing natural gas from Russia. In 2008, Azerbaijan exported an estimated 3.35 BCM, mostly shipping it via the South Caucasus Pipeline (SCP). The main conduit for Azerbaijan’s natural gas exports is the 429-mile SCP, also known as the Baku-T’bilisi-Erzurum pipeline (BTE), which runs parallel to the BTC oil pipeline for 429 miles, before connecting to the Turkish gas pipeline network at Horasan. The pipeline was commissioned in 2007 with an initial capacity of 8.8 BCM per year, which is to be increased in the future to 20 BCM with the addition of compression stations.

Azerbaijan is Turkey’s most promising source of new pipeline gas. In 2007 BOTAŞ imported 1.28 BCM of Azeri gas and re-exported 0.25 BCM to Greece via the TGI. Most of Azerbaijan’s gas exports are due to come from the 1.2 TCM Shah Deniz field in the south Caspian Sea. Phase One of the Shah Deniz project, expected to reach its production plateau of 8.6 BCM by 2009, is fully contracted until 2027; all of the gas from this stage of the project will be consumed in Azerbaijan or exported to Georgia and Turkey, or re-exported from Turkey to Greece. Phase Two, which has yet to be sanctioned, will not come on stream before 2012 or 2013, perhaps bringing total field production to 14–16 BCM by 2020.28

Overall regional gas demand in the South Caucasus and southern Russia is projected to grow by roughly 23 BCM between 2005 and 2025. If Gazprom is willing to purchase gas from Azerbaijan at European prices, minus transportation charges (known as netback prices), it could purchase gas from Phase Two of the Shah Deniz project and pipe it north through existing infrastructure to southern Russia. In June 2009, Gazprom Chairman Aleksey Miller met with Azeri President Ilham Aliyev and offered to purchase Azeri gas at “market prices” in a long-term contract. Gazprom reportedly defined market prices as the price of gas in Europe minus transportation costs and a “reasonable profit.” The Azeri-Russian deal is only about 1 BCM in 2009. However, all of the Shah Deniz Phase Two gas will flow west to Turkey. This phase is expected to provide a plateau volume of 16 BCM a year (first gas in 2016 with a plateau in 2017/18). There is considerable competition for this gas – Turkey, Nabucco, IGI, TAP, Iran, and Russia. The geostrategic position of Azerbaijan gives it the ability to develop a significant gas export capability to Europe via Turkey.

In order develop as a demand aggregator to secure gas demand and supply from this region, the EU Commission’s Second Strategic Energy Review announced a commission report that the establishment of a “Caspian Development Corporation” (CDC) has been proposed by the European Commission on 13-14 November 2008. The report introduces the concept of a Caspian Development Corporation (CDC) which is defined as a gas purchasing company combined with an obligation to sell to others at pass through or other prices.29 It is the fact that the CDC’s goals will focus on the development of Turkmen gas reserves and subsequent delivery of that gas to Europe through a dedicated infrastructure in the Southern Corridor.30

Even though Turkmenistan and Azerbaijan are competitors in the view of the market and in the legal status of the Caspian Sea, Turkey can contribute to a convergence of mutual interest for both parties to enter the international energy market as either suppliers or transit countries. Turkey supports the possible scenarios of Caspian natural gas export strategies presented in the following section.

The Scenarios for Turkmen Gas Exports to the European

Energy Market

The scenarios for Turkmen gas exports to Europe give insights into long-term supply contracts and the needed investment for both parties. Jonathan Stern provides the basic principles for the traditional approach to European energy security in his article which looks at natural gas supplies to Europe.31 The question is which transport option for the Caspian Sea region is feasible enough to attract the international gas companies’ investment into the region. It is the fact that Caspian energy producers wish to sell their oil and gas directly at market prices to have security and continuity of demand and to diversify their export sources and routes to maintain balanced energy geopolitics. Caspian energy producers do not want the militarization of energy security nor to rely on one single foreign country poking their nose in their domestic affairs. Transit countries (Georgia, Turkey and Azerbaijan) also want to stimulate their interests to strengthen their bargaining position with the West by becoming an energy hub, and to enjoy the economic benefits from the Azeri oil and gas production which will peak in this decade.

With the signing of the Turkey-Azerbaijan natural gas agreement in July 2010, Ankara loudly repeated its goal of becoming a future “energy hub” by allowing the creation of a Southern Corridor

Stern’s article offers five different scenarios on Turkmen gas export to the European energy market. The first scenario looks at the Trans-Caspian Pipeline, a 300 km shore-to-shore pipeline connecting Turkmenistan and Azerbaijan natural gas networks. The SCP, which has operated since 2007 with a 7 BCM capacity transporting gas from the Shah Deniz first field (SD-1) to Turkey, could be increased to a technical maximum of 20 BCM to allow Azerbaijan to transport gas from the second Shah Deniz field (SD-2) to the west through Turkey and Nabucco. For any additional transit gas from Turkmenistan a new pipeline is required to increase transport capacity to 31 BCM. It is important to note that expanding capacity on current pipelines is far cheaper than building new pipelines, especially if the SD-2 export gas volumes remain only at 13 BCM. The option to transit gas from Azerbaijan via Iran to Nabucco is not considered by European companies.

The second scenario needs technological advancements. European companies have tie-in solutions for offshore transport between two platforms. A tie-in solution can interconnect Turkmen and Azeri gas production platforms using the existing offshore pipeline grid. The concept consists of the tie-in pipeline itself, and a subsequent landfall pipeline to the Azeri shore, which can draw on existing pipelines and routes. This solution through the Caspian Sea is seen as technically and economically the most realistic option in terms of implementation. The offshore connections between two platforms could comprise more than 2,000 km of oil and gas pipelines, but it requires a solution to the problem of defining national sectors in the Caspian Sea. The third scenario, which uses the traditional natural gas transport solution of shipping gas across the sea in CNG and LNG vessels, is not economical due to the short distance of transportation. The fourth scenario involves the rehabilitation and extension of the existing pipeline from Iran to the Turkish border and uses that to transport gas. European companies are still refraining from involving Iran due to the international political environment. In addition to this, Turkmen gas can be transported from Russia to Turkey by increasing the capacity of Blue Stream pipeline. Rather than compete, Turkey has maintained good relations with Russia over the last few decades.

Concluding Remarks

With the signing of the Turkey-Azerbaijan natural gas agreement in July 2010, Ankara loudly repeated its goal of becoming a future “energy hub” by allowing the creation of a Southern Corridor. This is one of the EU’s highest energy security priorities. While Azeri gas supply contracts with Russia and Iran are similar to the Turkish one,32 Europe has not been ready to see Turkey’s new opening as an act of a regional power. Turkey gives unconditional support to most of the projects, sharing common interest of Caspian region and EU countries and applies EU laws on Turkish territory that would primarily serve to EU interests; however, the EU has lacked long-term coherent policies on supply security. Turkey and EU have failed to complete all regulation in regard to 35 chapters of the EU’s acquis so far. Thirteen chapters, including energy, are still blocked by the EU commission which self-interest attitude towards Turkey’s new energy policy. For instance, European Coordinator Van Aartsen defined Turkey’s role as an ‘interconnector’ and also wrote that Turkey should act as a bridge. He presumes that rather Baku, Romania, Greece, Italy can be more potential to be an energy hub.33Besides that some energy lobbies undermines Turkey’s geostrategic position in energy transport. It is deniable the fact that Turkey’s development as a European energy hub looks natural, given its lucky location between countries that harbour over 70 per cent of the world’s oil and gas reserve to its east, north and south, and one of the world’s biggest energy markets in the west.

On the other hand, Turkey’s role as regional facilitators, and rhythmic diplomacy coupled with the zero problems with neighbors policy have helped improve its relations with neighbors especially Armenia. In the Caucasus region, Turkey’s initiative increased the following the “football diplomacy” in September 2008 which has helped in the creation of the Caucasus Stability Platform.34 However, this rapprochement does not affect Turkish-Azeri relations.35 The question still remains of how practical the protocols which were signed by Turkish and Armenian government will develop a secure energy corridor from Caspian Sea to the EU.

The article had reached the conclusion that Turkmenistan has the necessary resources to provide Europe, Russia, Iran and China with gas. The main obstacle for Europe, unlike the other three export outlets, is the lack of a reliable transportation route. The only way that Turkmen gas can reach Europe is via Russia, Iran-Turkey, or Azerbaijan-Georgia-Turkey. This is the biggest challenge because both Russia and Iran will be unwilling to let their current and future domination of Turkish and European gas markets be captured, even in a small measure, by Turkmenistan. Hence, the option for transport via Turkey through Azerbaijan is the most desirable from a security of supply perspective.

Endnotes

• The opinions expressed in this article are only those of the authors.

- “Turkey’s gas deal with Azerbaijan fuels hopes in EU”, Euro Active, May 17, 2010, retrieved May 5, 2010 from http://www.euractiv.com/en/energy/turkey-s-gas-deal-azerbaijan-fuels-hopes-eu-news-494198.

- Brenda Shaffer, “Turkey’s Energy Policies in a Tight Global Energy Market.” Insight Turkey, Vol. 8, No. 2, (April-June, 2006), pp. 97-104.

- Mehmet Ogutcu, Gelecek Hikayeleri “Turkmenistan: Dogal gaziyla yeniden “Buyuk Oyun”u tetikledi (September 23, 2009) retrieved 10 May, 2010, from http://www.abvizyonu.com/guncel/mehmet-ogutcu-yeni-enerji-duzeni-ulusal-sampiyonlar-ruslar-ve-siyasetciler.html.

- World Energy Outlook 2009 (WEO-2009), International Energy Agency, retrieved from http://www.iea.org/W/bookshop/add.aspx?id=388.

- Ibid.

- “Turkmenistan Energy Profile 2009,” US Energy Administration Energy 2010, retrieved May 14, 2010, from http://tonto.eia.doe.gov/country/country_energy_data.cfm?fips=TX.

- Peter C. Glover, “Turkmenistan Joins the Natural Gas Elite: The South Yolotan-Osman Gas Field is one of the World’s Largest”, Energy Tribune, (December 8, 2008), retrieved May 10, 2009, from http://www.energytribune.com/articles.cfm?aid=1046.

- Vremya Novostey, “Turkmenistan gas reserves exaggerated”, December 13, 2009. The original article in Russian can be found below. Indra Øverland 14 Oct. 2009 NUPI / University of Tromsø.

- WEO-2009 and and CEDIGAZ News Report Vol. 48, No. 29, (December 23, 2009) retrieved May 10, 2010, from www.cedigaz.org.

- WEO-2009.

- Ibid.

- Ibid.

- CERA Eurasian Gas Export Outlook (May 2009) retrieved May 10, 2010, from https://www.cera.com/aspx/cda/client/report/reportpreview.aspx?CID=11235.

- WEO-2009.

- We thank Mehmet Ogutcu for sharing with us his personal archive and knowledge on energy profile of Turkmenistan in this section.

- John Roberts, “Energy in East Europe,” Platt Energy News, Issue 181 (January 15, 2009) retrieved May 12, 2010, from http://www.platts.com/Products.aspx?xmlFile=energyineasteurope.xml.

- Simon, Prani, “The impact of the economic CIS on Russian and crisis gas markets” Oxford Energy Institute, (November, 2009).

- “Turkmenistan: Gas Blast Ignites Turkmen-Russian Row”, Eurasia Net (April 9, 2009) retrieved May 12, 2010, from http://www.eurasianet.org/print/58908.

- Vladimir Socor, “Russia Resuming Gas Imports from Turkmenistan on a Small Scale” Eurasia Daily Monitor, Vol. 7, Issue 1 (January 4, 2010) retrieved May 12, 2010, from http://www.jamestown.org/single/?no_cache=1&tx_ttnews%5Btt_news%5D=35866.

- Sergie Blagov, “Russia Struggles to Revive Energy Ties With Turkmenistan”, Eurasia Daily Monitor, Vol. 6, Issue 230 (December 15, 2009).

- WEO-2009 p.474.

- “Turkmen leader visits China” The Times of Central Asia, May 7, 2010.

- Karbuz, Sohbet “The key determinant of future energy transit routes to Europe from Caspian region,” Chatham House conference on the Politics of Central Asia and Caspian Energy, London, (February 24, 2010).

- Ibid .

- “Turkey’s Minister in opening of Turkmenistan-Iran pipeline”, World Bulletin (January 6, 2010), retrieved May 10, 2010, from http://www.worldbulletin.net/news_detail.php?id=52264.

- Elin Kinnander, “The Turkish-Iranian Gas Relationship: Politically Successful, Commercially Problematic”, Oxford Energy Institute, Report No: NG 38 (January, 2010), retrieved May 12, 2010, from http://www.oxfordenergy.org/gasresearch.php.

- “Azerbaijan”, Oil and Gas Journal, (January, 2009).

- “Cracks in The Bridge: The Uncertainties of Turkish Gas Transit: The Uncertainties of Turkish Gas Transit”, CERA Advisory Service Private Report-2008, retrieved May 23, 2010, from www.cera.com/aspx/cda/client/report/report.aspx?CID=9624.

- Vladimir Socor “Increased Western Involvement in Caspian Sea Energy Transport”, Eurasia Daily Monitor, Vol. 6, Issue 2.

- Platts Insight (November 21, 2008). See: http://www.platts.com/InsightandAnalysisHome.aspx

- Jonathan Stern. “Security of European natural gas supplies,” Royal Institute of International Affairs, London (July, 2002); See also J. Stern “UK gas security: time to get serious* 1.” Energy Policy, Vol. 32, No. 17, (2004), pp. 1967-1979.

- Simon Pirani, “Russian gas, Central Asia and the Caspian”, Chatham House (February 23, 2010).

- JoziasVan Aartsen, “European Coordinator for Southern Corridor,” Activity Report (Sept. 2007-Feb. 2009).

- Bülent Aras and Hakan Fidan, “Turkey and Eurasia: Frontiers of a New Geographic Imagination,” New Perspectives on Turkey, No.40. The Special Issue on Turkish Foreign Policy (2009), pp. 195-217.

- F. Yesim Akcollu,”Major challenges to the liberalization of the Turkish natural gas market”, Oxford Institute for Energy Studies, Report No: NG 16 (November, 2006), retrieved May 9, 2010, from www.oxfordenergy.org/pdfs/NG16.pdf.