Landing in Erbil (Hewler), capital of the Kurdistan region of Iraq, one of the first things that strikes the visitor is the role of Turkey. Western oil executives and Iranian traders are prominent, but Turkish businesses, visitors, engineering and construction companies, restaurants and products are ubiquitous. Kurdistan’s energy resources make it an important economic and strategic partner for Turkey in the region, but also involve Ankara in the complexities of intra-Iraq politics.

A complicated three-way chess game is being played out here between Erbil, Baghdad and Ankara. Yet even the pieces on this chessboard—Iraqi, Kurdish and Turkish politicians, western oil companies, and ordinary Iraqis—have their own agendas. Outside powers such as Iran and the US are also watching the game carefully, perhaps even moving pieces of their own. Turkey has a lot to gain from engaging with the Kurdistan region, and can improve its own energy security, particularly in the area of gas. Nevertheless, it also has major long-term interests in the rest of Iraq, and has to play carefully to avoid compromising these.

Meanwhile, Erbil is seeking to use its oil and gas to secure its own economic future and political autonomy from Baghdad. Given the realities of politics and geography, this makes it dependent on Turkey for export routes.

Erbil is seeking to use its oil and gas to secure its own economic future and political autonomy from Baghdad. Given the realities of politics and geography, this makes it dependent on Turkey for export routes

Kurdistan: An Emerging Hydrocarbon Power

Kurdistan’s oil and gas reserves are relatively modest compared to those of “federal” Iraq (the country excluding the autonomous Kurdish region). Federal Iraq’s reserves are put at 143 billion barrels (bbl) of oil, the fifth largest in the world (and likely to grow further, to 200 billion barrels or more), and 127 trillion cubic feet (Tcf) of gas (12th largest in the world, but also likely to increase).

By contrast, the Iraqi Kurds hope to find some 30-60 billion bbl; excluding the Kirkuk field, which remains in disputed territory, they currently have some 12 billion bbl of oil and 22 Tcf of gas. Amongst the largest fields so far are the Shaikan field with potential for 3.3 billion bbl of oil reserves, Bardarash with 1.2 billion bbl, and Khor Mor and Chemchemal with some 10 Tcf of gas between them. The most advanced in development are DNO’s Tawke field (771 million bbl in reserves), Taq Taq (647 million bbl) held by the Turkish company Genel, and Khor Mor which is supplying gas to local power stations.1

Although the Kurdish region’s oil resources are only a tenth or so of Iraq’s total, this is still highly significant in the context of a population of almost 5 million. Current discovered resources are probably larger than the reserves of OPEC member Ecuador (population 15 million) or major exporter Azerbaijan (9 million). The Kurdistan Regional Government (KRG) plans to reach a production capacity of 1 million barrels per day (bpd) by 2016,2 also larger than Ecuador or Azerbaijan. This would generate revenues of around $35 billion per year at current oil prices,3 compared to the current Kurdish share of the national budget which amounts to around $12 billion. This does indicate that Kurdistan’s oil and gas could be the foundation for a viable economy.

These resources have largely been discovered since 2005 by a variety of international oil companies (IOCs), initially small but now joined by several large IOCs. The Kurdistan Ministry of Natural Resources (MNR), under Minister Ashti Hawrami, has carefully selected its partners to give a wide variety of representation, including Turkish, European, Canadian, American, Chinese, Indian, Russian, Emirati and other companies. Not all have been successful, and some have withdrawn, including the Korean National Oil Company and India’s Reliance, but the overall geological success rate has been impressive.

Kurdistan Regional Government Natural Resources Minister Hawrami shakes hands with Turkey’s Energy Minister Yildiz during a joint news conference in Arbil. | REUTERS/Azad Lashkari

Kurdistan Regional Government Natural Resources Minister Hawrami shakes hands with Turkey’s Energy Minister Yildiz during a joint news conference in Arbil. | REUTERS/Azad Lashkari

One dramatic difference between Kurdistan and the rest of Iraq is in the provision of electricity. Kurdistan has some 650 MW of hydroelectric capacity, but it has augmented this in recent years with gas-fired power plants contracted with independent power producers (IPPs), and now has almost 24-hour electricity. By contrast, generation in the rest of Iraq has expanded too slowly to keep up with demand, and grid electricity is available for only some 8-12 hours per day, depending on the province and season. The KRG has been supplying some electricity to Kirkuk and other bordering areas, partly to extend its political influence.

The energy resources of northern Iraq outside the Kurdistan region are also very significant. The Kirkuk field, although old (it was discovered in 1927), is still the cornerstone of northern oil production, with several other important fields such as Jambur, Khabbaz and Bai Hassan nearby. The Kurds are developing the northernmost part of Kirkuk, the Khurmala Dome. From Kirkuk, the main export pipelines run north, crossing the Turkish border in KRG territory at Fishkhabour, and terminating at the Mediterranean port of Ceyhan. The twin pipelines have a theoretical capacity of 1.6 million bpd, but sabotage and lack of maintenance limits this to around 0.3-0.4 million bpd.

The Shaky State of Baghdad-Erbil Relations

Relations between the federal government in Baghdad and the KRG in Erbil have long been problematic. Two of the major problem areas are the status of the “disputed territories” in Kirkuk, Ninewa, Salahaddin and Diyala provinces, and the right of the Kurds to sign independent oil exploration contracts, with the associated questions of oil exports, payments to the IOCs operating in the KRG, and the KRG’s share of the national budget.

In the energy context, the disputed territories are significant because of their oil and gas resources, notably the Kirkuk field, though the question of political control is separate from that of oil operations and revenues. Several of the contracts signed by the Kurdish authorities with IOCs cover the disputed areas. The Kirkuk issue is also complicated by the presence of an ethnic Turkmen population backed by Turkey. In November, confrontation flared in Tuz Khurmatu in Salahaddin province between Baghdad’s “Dijla Force” and the Kurdish peshmerga forces. However, the US intervened to encourage the sides to cool off, and Iran’s Qassem Suleimani, commander of the Qods Force, reportedly reassured both KRG President Barzani and Iraq President Jalal Talabani that Iran would not allow military conflict between the peshmerga and Iraqi army.

The Kurdish authorities take the view that under the Iraqi constitution they are entitled to sign contracts for “future fields” (essentially all fields, as only the Taq Taq, Chemchemal and Khor Mor fields were known prior to the approval of the constitution and they had not been developed). The IOCs in Kurdistan operate under Production Sharing Contracts (PSCs), unlike the service contracts favored by Baghdad.

Baghdad’s position is that PSCs are forbidden by the constitution. There are also accusations that the Kurdish PSCs are too generous, leading theoretically to an IOC share of some 20 percent of profits,4 as compared to Baghdad’s service contracts which typically pay $1-2 per barrel (i.e. 1-2 percent of profits at $100 per barrel oil price). However, any view of the “generosity” of the KRG’s contracts has to be tempered by the geological risk in Kurdistan, the generally smaller size of the Kurdish fields compared to the giant discovered fields in south Iraq, and the continuing political and payment risks.

At the moment, exports through the federally-controlled pipelines to Turkey are intermittently allowed by agreement with Baghdad, such as in early 2011 and again in September 2012, but these accords have repeatedly broken down. Revenues are remitted to Baghdad, which then pays the KRG a share to cover the costs (but not the profits) of the IOCs. In the absence of consistent exports, IOCs in Kurdistan have to sell much of their production locally for a price currently around $60 per barrel. It is then used in small-scale local refineries or, reportedly, exported via Turkey and Iran, considered to be smuggling by the federal Iraqi authorities.

Turkey is the key transit route for Kurdish hydrocarbons to world markets, and for supplies to enter the Kurdish region. This gives Turkey leverage over Erbil

Ultimately, whatever the legal arguments on either side, these questions are not susceptible to a legal resolution—the constitution is too vague and the outcome too important to both sides. Iraqi Prime Minister Nouri Al Maliki has relied on Kurdish support at various times in the past, notably during 2008’s “Charge of the Knights” operation against militias in Basra, and when scrambling to assemble a majority following 2010’s parliamentary elections. It remains to be seen what type of coalition he will attempt to gather for the 2014 polls. But at the moment, the Kurds have a significant political role in Baghdad via their members of parliament, and leading officials including Iraqi President Jalal Talabani (head of the Patriotic Union of Kurdistan party) and foreign minister Hoshyar Zebari.

Maliki has also used crises, often ones which he himself has instigated, to preserve his role as the indispensable arbiter. Both sides have shown a preference for maximalist negotiating positions, encompassing a swathe of other issues. These stances also play well to nationalist political supporters on both sides: the Kurds in the KRG, and the Sunni Arabs in the disputed territories who are not natural Maliki voters, but who may be drawn to him by a strong stance against the Kurds.

A compromise could be reached: for instance, it should be possible to separate the issue of oil resources from territorial control, and oil resources in the disputed territories could be developed jointly. A national oil and gas law, long discussed, could be passed which legitimizes the KRG’s PSCs, perhaps in return for some legal and fiscal adjustments. An agreement on oil and gas export infrastructure from the KRG could be reached, while further electricity exports would help ease the situation in federal Iraq.

In the absence of a resolution, deputy prime minister for energy (and former oil minister) Dr Hussein Al Shahristani has adopted a policy of blacklisting IOCs which sign contracts with the KRG, preventing them from bidding for contracts in the south. Initially this applied to companies with contracts in Kurdistan, such as Sinopec (after its acquisition of Addax) and Hess. In October 2011, ExxonMobil upset this policy by signing for six blocks in Kurdistan, while already the operator of the West Qurna-1 project near Basra, a cornerstone of Baghdad’s production growth plans. As the “blacklist” was an Iraq Ministry of Oil (MoO) policy, not a legal or contractual principle,5 Baghdad’s options for retaliation were limited.

However, it now seems (as of November 2012) that ExxonMobil, finding the contractual terms and government support in West Qurna-1 disappointing, will sell its share, hence avoiding problems without resolving the underlying issue. Gazprom and Total are in a similar position, having signed contracts with the KRG while having deals in the south of Iraq, and while there have been threats by the MoO against Gazprom, it remains to be seen whether either will be forced to leave. There are also persistent rumors that other companies in the south, notably Shell and BP, may also enter Kurdistan. There are now relatively few open opportunities, so future new entrants would be likely to have to acquire the shares of existing smaller players.

The KRG has also succeeded in attracting several other notable companies—supermajor Chevron (which was not active in federal Iraq), Chinese national oil company Sinopec (via its acquisition of Addax), Spain’s Repsol, Canada’s Murphy, the US Hess and Marathon, Austria’s OMV and Hungary’s MOL. This gives it a good technical and financial basis for developing its resources. However, some of the smaller companies with large discoveries, notably Gulf Keystone (developing the Shaikan field) will probably need partners or will be acquired. Conspicuous by its absence from the Kurdish energy scene is Iran,6 which offers little technically or financially.

In September, Genel CEO (and ex-BP CEO) Tony Hayward suggested that “The scale of the opportunity for Kurdistan and for Iraq is so large that there will be a resolution. Over the next year or two, Kurdistan production capacity will grow towards 1 million barrels a day—that’s too much oil to be shut in as a consequence of a political dispute. So one way or another, it’s going to get resolved.”7

But it is far from clear that his optimism is warranted. The required investment to reach 1 million bpd of production capacity will not be made without a clear right to export, and the relatively small companies that have made most of the large discoveries to date—Genel, DNO, Gulf Keystone and Afren—will find it difficult to finance development on their own. Baghdad is aware of the leverage it holds by controlling the Kurds’ export route.

In July 2012, Turkey and the KRG reached a deal, denounced by Baghdad, to export crude (initially by tanker) in return for refined products, of which the KRG complains of an inadequate allocation from Baghdad. Tanker exports are expensive and limited in volume, and therefore cannot provide a large-scale, long-term solution.

However, Turkey has not so far chosen to break with Baghdad by sanctioning an independent Kurdish oil or gas pipeline. On December 4, 2012, Turkish energy minister Taner Yıldız was expected to make a major announcement on Turkish energy investment and perhaps export pipelines from the KRG at a conference in Erbil; however, the Baghdad government prevented his flight from landing (or indeed, taking off). The substance of this announcement therefore remains unclear, though the central government’s opposition to it is clear.

The Five Pillars of the KRG-Turkey Energy Relationship

Iraq’s Kurdish region is significant to Turkey for five main energy reasons (apart from, of course, non-energy considerations).

Firstly, the KRG is a potentially significant supplier of oil and gas which would transit via Turkey and/or could be sold in the Turkish market. Oil is normally a fungible commodity; however, it is arguable that, having no other geographic outlet, Kurdish oil is a captive source of supply for Turkey in the event of disruptions elsewhere.

Securing Kurdish gas would be of considerable value to Turkey in its negotiations with Russia, Iran and Azerbaijan

It would be in Turkey’s interest to provide Iraq with alternative export routes. This is partly because it would earn some transit fees, and partly because it would gain some political leverage over Baghdad. But most crucially, it would reduce the threat of a cut-off of Iraqi oil exports, a possibly unlikely scenario but one which would drive up oil prices for all consumers, including Turkey. Alternative export routes serve as a deterrent to any country (most likely Iran) that might seek to block Gulf shipping lanes. This should not be confused with any physical security of oil supply to Turkey, although it is worth noting that Turkish oil consumption of around 700 thousand bpd could be entirely met by a rehabilitated Kirkuk-Ceyhan pipeline, or a new Kurdish pipeline of 1 million bpd capacity.8 In the event of a crisis blocking exports through the Gulf, Ankara’s control of Iraq’s only remaining export route would give it major leverage.9

However, Turkey realizes that permitting an independent Kurdish oil export route in defiance of Baghdad would be an extremely provocative move. Even at a time when it is far from happy with the Maliki government, it seems unlikely to break relations so dramatically. This might also meet with substantial opposition from anti-AK Party media and political groups in Turkey, which would present it as encouraging Kurdish independence and other separatist movements, notably in Syria.

Turkey’s interest is clearer in the case of gas, where it is in a position to negotiate favorable terms for the supply of Kurdish gas, which could be aggregated with other supplies (from Azerbaijan, Russia and Iran) and supplied to European markets. It was hoped that Kurdish/Iraqi gas would be a foundation source of supply for the Nabucco pipeline, intended to diversify European supplies away from Russia.

Nabucco will now not go ahead, at least in its original form, due to delays in securing supply commitments. Russian progress on the South Stream pipeline (which runs under the Black Sea) also raises the possibility that the European gas market will be oversupplied, and due to recession and lack of gas competitiveness versus coal, European gas demand is unlikely to recover to its 2005 peak level before 2020. Nevertheless, Turkey is making progress on the Trans-Anatolian Pipeline (TANAP) which then leads to a number of options for supplying south-eastern and central Europe and perhaps Italy. Kurdish gas is therefore of potential significance to Europe, even if not of the importance that it appeared a few years ago.

Reliable gas supply from Iraq would strengthen Turkey’s negotiating hand with Azerbaijan, Russia and Iran. Iranian supplies in particular are unreliable, often cut off during winter when Iranian domestic demand increases. Turkey has found it difficult to pay for its gas deliveries from Iran due to the growing strength of sanctions against the Iranian financial sector, leading to a “gold-for-gas” trade,10 itself targeted by further US Senate-led sanctions proposed in December 2012.

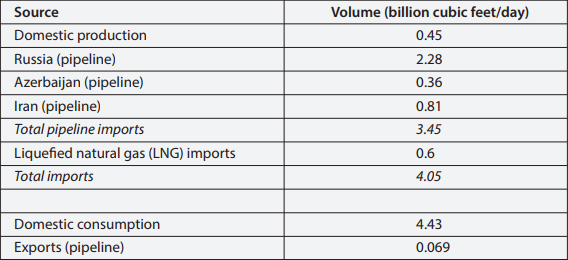

Turkish gas consumption, of 4.4 billions of cubic feet (Bcf) per day in 2011, is the fourth largest in Europe,11 and growing exceptionally rapidly, at a compound annual growth rate of 11 percent since 2001. By contrast, most other large gas markets in Europe are shrinking.

Turkey’s gas balance in 2011 was as follows:

In this context, possible Kurdish exports of around 1.45 Bcf per day would be highly material, more than enough to replace Iran, or to meet three years of demand growth at the prevailing rate of around 10 percent. Since the only route to market for Kurdish gas, barring a major improvement in relations with Baghdad, is via Turkey, the Turks should be able to extract a favorable price, and/or reduce the price they have to pay to another supplier. Indicatively, a discount of $1 per million British thermal units (MMBtu) for the Kurdish import volumes would save Turkey more than $500 million per year (European gas import prices are currently about $12 per MMBtu).

Secondly, the Kurdish region is an important market for Turkish companies. The head of the economic committee in the province of Sulaimaniyah (Slemani), Ahmad Haj Rashid, put KRG-Turkey trade at $12 billion in 2011.12 Total Turkish trade with Iraq was $7.5 billion in 2010, of which 70 percent was with the Kurdish region, and the Turkish consul-general in Erbil stated that business with the KRG exceeds that with Syria, Lebanon and Jordan combined.13 Turkey’s Genel Enerji was one of the early leaders in developing Kurdish oil and has continued to increase its footprint following its acquisition by ex-BP CEO Tony Hayward’s corporate vehicle. Turkish engineering companies are important players in developing the energy sector. Strong economic growth in the Kurdish region is driven by oil and gas revenues (mostly remitted from Baghdad), and policies friendly to trade and foreign direct investment generally.

Thirdly, Turkey is the key transit route for Kurdish hydrocarbons to world markets, and for supplies to enter the Kurdish region. This gives Turkey leverage over Erbil and underpins its policy of constructive economic and political engagement. The Erdoğan government appears to have taken the view that a stable, prosperous Iraqi Kurdistan region, economically dependent on Ankara, is the best outcome in dealing with its own Kurds. Turkey has also sought to work with KRG President Massoud Barzani to moderate the behavior of the Kurdish parties in the north-east of Syria (itself an important oil region) in the continuing civil war against President Assad. Were Assad to be overthrown, the regional picture would change sharply and unpredictably, perhaps, though this is far from certain, giving the KRG other options for hydrocarbon exports.

The key aim for the KRG is to secure export routes for oil and gas independent of Baghdad’s control, but these would still be reliant on Turkey

Fourthly, relations with Erbil are a source of Turkish leverage against Baghdad. Turkey has not wished to break relations with the government of Nouri Al Maliki, but relations have deteriorated over factors including Baghdad’s perceived support for the Assad government in Syria; Turkish foreign minister Ahmet Davutoğlu’s visit to the disputed city of Kirkuk, made without informing the Baghdad government; and the presence in Turkey of former Iraqi vice-president Tareq Al Hashemi, sentenced to death in absentia in Baghdad on charges of running a murder squad. However, Davutoğlu has come under domestic pressure recently as his policy of “zero problems with neighbors” has run aground with the Syrian civil war, the breakdown of relations with Israel, and disputes with Baghdad.14The continuing conflict in Syria has, of course, both ethnic and sectarian dimensions, with Shi’a governments in Iran and Iraq supporting the Assad regime,15 the Gulf states and Turkey backing the largely Sunni Arab opposition, and the (predominantly Sunni) Kurds playing an ambiguous role in the middle.

Fifthly, the KRG has significance for Turkey’s relationship with its own Kurdish population. As well as the Kirkuk-Ceyhan pipelines, the 1 million bpd Baku-Tbilisi-Ceyhan oil pipeline and Baku-Tbilisi-Erzurum gas pipeline from Azerbaijan run through Kurdish areas and have been attacked by the Kurdish separatist group the PKK. The spill-over of prosperity into south-eastern Turkey would help improve conditions in a historically deprived part of the country.

Turkish direct interest in federal Iraq’s energy is less, though its global importance is much greater. Turkish state oil company TPAO has significant involvement in federal Iraq, with a 10 percent share in the Badra oil-field development on the Iranian border, 11.25 percent in the Missan oil-field, 40 percent in the Siba gas field near the Kuwaiti border, and 50 percent (where it is also the operator) in the Mansuriya gas field in Diyala. Siba and Mansuriya total some 3.6 Tcf of gas reserves with estimated investment at $3.9 billion. In November, however, TPAO was expelled by the MoO from the Block 9 exploration project in southern Iraq against the backdrop of worsening Turkish-Iraqi relations.

The direct energy importance of federal Iraq to Turkey is debatable. Iraq has not shown particular urgency to rehabilitate or expand the Kirkuk-Ceyhan pipeline, nor the north-south “Strategic Pipeline” which would allow for moving oil from south to north (or vice versa). This is surprising in view of Iraq’s near-total dependence for its current oil exports on the facilities around Basra, which are vulnerable to bad weather, accidents and sabotage, and on free passage through the Persian Gulf and the Strait of Hormuz. Iraq has also moved slowly on gas exports, partly due to a mistaken perception that it has only limited volumes available for export after satisfying domestic demand.

However, Turkey clearly recognizes that federal Iraq, with 25 million people against the Kurdish region’s 5 million, and oil resources probably ten times greater, is a more important long-term prize. And Kurdistan has no other natural regional allies, while Iraq is close to Iran and has improved relations with Kuwait and Jordan. The KRG does therefore run the risk of being taken for granted by Ankara, or even cast aside as part of a larger game, as the Iraqi Kurds were by the Shah of Iran in 1975. It is possible that Baghdad could make a more tempting offer to Turkey, recasting its tough fiscal terms, to wean it away from the KRG. However, Turkey would always have to be skeptical of the Baghdad government’s will and ability to deliver. And, given the poor and deteriorating state of Ankara-Baghdad relations, this appears more of a long-term eventuality.

Conclusion

Iraq’s energy resources are of potentially global importance, particularly in oil. The Kurdistan region’s oil and gas is much less significant on the world stage, but is very important for the future of the autonomous region itself. Securing Kurdish gas would be of considerable value to Turkey in its negotiations with Russia, Iran and Azerbaijan. Kurdish economic and political stability is also valuable to Turkey as it seeks to manage its relationship with its own Kurdish population and that in Syria.

Turkey has so far balanced carefully between Baghdad and Erbil. Similarly, the Maliki government in Baghdad, though enduring a number of crises with the KRG, has always managed to reach temporary solutions. This dynamic might persist for an extended period. The key aim for the KRG is to secure export routes for oil and gas independent of Baghdad’s control, but these would still be reliant on Turkey. A decision by Ankara to deal directly with the KRG on oil and gas exports, and to pay for them without the intermediation of Baghdad, would have momentous implications for Turkey’s implicit recognition of the KRG’s sovereignty, for its relations with its own Kurdish population and the Kurds of Syria, and for the continuing integrity of a united Iraq.

A grand bargain within Iraq itself, including a federal oil and gas law, would be a less inflammatory and more satisfactory and durable solution, but awaits a major political realignment.

The energy triangle between federal Iraq, the Kurdish region and Turkey thus presents a fascinating situation in which oil and gas resources—as yet only at a very early stage of exploration and development—have become a key economic and political tool for each player. The weakest participant, the KRG, has played its pieces skillfully so far. This game greatly needs a resolution, but the logic of the struggle does not allow either Ankara or Baghdad a swift checkmate.

Endnotes

- All of these reserve estimates are likely to increase as appraisal and field development work progresses.

- “Kurdistan aims for one million barrels of crude per day by 2016”, IJK News, retrieved from http://ikjnews.com/?p=2091.

- Minus production costs, perhaps on the order of $3-6 billion per year though higher initially.

- Though the KRG retains a 20-25 percent carried share in most blocks, and depending on the costs and bonuses paid, the IOCs’ share may be as low as 7 percent.

- Though the 4th Round contracts mention it explicitly.

- Though Iran is heavily involved in the economy and politics of both the Kurdish region and the rest of Iraq.

- Peg Mackey, “Iraq’s Kurd oil row too big

to last - Genel’s Hayward”, Reuters, September

7, 2012, retrieved from http://uk.reuters.com/

article/2012/09/07/uk-genel-kurdistan-

idUKBRE8860K320120907. - Turkey, of course, also transits some 1 million bpd in the BTC pipeline, and some 2.9 million bpd of mostly Russian and Caspian oil via the Bosphorus Straits.

- Iraq is considering developing alternative oil export routes, with a pipeline via Jordan the most likely medium-term option.

- For example see Daniel Dombey, “Turkey: so it is gold for gas after all”, BeyondBrics Blog, Financial Times, November 23, 2012, retrieved from http://blogs.ft.com/beyond-

brics/2012/11/23/turkey-so-it- is-gold-for-gas-after-all/# axzz2DGk08HSs. - Excluding the former Soviet Union. Only Germany, the UK and Italy have larger consumption.

- “Kurdistan Region to Reduce Trade With Iran and Turkey,” IJK News, retrieved from http://ikjnews.com/?p=142. Trade with Iran was $10 billion.

- “Open for business: Turkey’s bankers tap into Kurdish boom,” IJK News, June 21, 2011, retrieved from http://ikjnews.com/?p=881.

- See for example, Tulin Daloglu, “Turkey’s Davutoglu Under Fire For Failed Mideast Policies”, Al Monitor, November 29, 2012, retrieved from http://www.al-monitor.com/

pulse/originals/2012/al-monitor/davutoglu- blame-fail.htmlutm_source=&utm_medium=email& utm_campaign=5385. - Though both have hedged against his eventual downfall.