Introduction

The Eastern Mediterranean Basin has become popular since the beginning of the 2000s, especially in the context of the potential energy resources in the region. Along with this potential, debates on discoveries, production processes, and transfer options of the resources have continued. Although the current situation in the region started 20 years ago, the historical process of offshore drilling in the Eastern Mediterranean goes back to the 1960s. During this period, Egypt and Israel carried out various drilling operations.1 However, success could not be achieved due to the technical deficiencies and conditions of that period. In the early 2000s, exploration activities in the Eastern Mediterranean Basin began again with the small-scale discoveries of Israel. The discoveries of Tamar and Leviathan fields located in Israeli territorial waters in 2009 and 2010 caused international attention to turn to this region. These two fields were the world’s largest deep-sea gas discoveries in that period. Later, the discoveries of the Aphrodite field in 2011 and the Zohr field in 2015 have moved the Eastern Mediterranean’s position from regional to a global level. In brief, the discovery of a substantial amount of energy resources overtime in the Eastern Mediterranean has turned the region into an environment of multidimensional competition.

As its name signifies, the Eastern Mediterranean Basin covers the area in the East of the Mediterranean Sea. This region’s western boundary starts from Sicily and Tunisia, while the eastern frontier extends to the coasts of Turkey, Syria, Lebanon, and Israel.2 In the Eastern Mediterranean, the exploration and drilling activities have been conducted intensively in the area between the South of Turkey and North of Israel, Egypt, and Libya. Therefore, Turkey, the Turkish Republic of Northern Cyprus (TRNC), the Greek Administration of Southern Cyprus (GASC), Syria, Lebanon, Egypt, Libya, Greece, Israel, and Palestine are the countries to have the inherent rights to explore and exploit the energy resources in the region. In this sense, some of these countries’ exploration and drilling activities have continued in the region for a long time. Turkey, Egypt, Israel, and GASC are the leading countries that have maintained drilling activities in the Eastern Mediterranean. Among these, while Egypt, Israel, and GASC have carried out several explorations, Turkey has recently started pursuing drilling operations. The countries that have not yet drilled are Syria, Lebanon, Libya, and Palestine. It is quite clear that ensuring energy independence and security by discovering and producing hydrocarbon resources has strategic importance for all countries in the region. Therefore, the resources discovered in the region in the last 20 years and waiting to be discovered in the near future are crucial for both the political and economic balances in the Eastern Mediterranean.

In addition to exploration and drilling activities, several technical, commercial, legal, and political challenges need to be overcome to extract and export the resources from the region. In this context, determining the maritime boundaries between the countries in the region is one of the main problems in the Eastern Mediterranean. This problem has caused certain delays and inconveniences in exploration and export operations. To solve the said problem, countries in the region need to meet on a common platform and design the maritime zones on an equitable basis. However, the maximalist attitudes of some actors in the region prevent the resources from being shared fairly and justly.

The resources discovered in the region in the last 20 years and waiting to be discovered in the near future are crucial for both the political and economic balances in the Eastern Mediterranean

On the other hand, the region’s hydrocarbon resource potential offers essential opportunities to enable local and global cooperation, increase energy supply security, and establish a stable political system.3 According to the latest estimates, the oil and gas potentials of the region are almost 5 billion barrels and over 13.5 trillion cubic meters, respectively. Moreover, the economic value of this potential is worth hundreds of billion dollars. For this reason, the region needs to transform into a geography that provides economic benefit rather than an environment of conflict. Therefore, a joint agreement platform is required in the region with the participation of all parties.

The main debate in the Eastern Mediterranean Basin can be categorized into three headings: economic, political, and judicial. These three fundamental issues are closely associated with the energy resource potential in the region. In this context, two major points become prominent: utilization of the hydrocarbon resource potential in the region and transferring the resources to the international markets. These matters lead to some political and judicial problems for both the countries and actors in the region. Therefore, several challenges must be overcome to allow optimal discovery and exploration activities in the Eastern Mediterranean. One of the first things to be done is to establish a cooperation organization encompassing all countries in the region.

Within the framework of the issues mentioned above, this research aims to analyze the competition in the Eastern Mediterranean from the perspective of energy resources. The structure of this article consists of three parts. First, the study focuses on the energy resource potential and discoveries in the Eastern Mediterranean Basin. The second part will present the production processes of the discovered gas resources and possible transfer routes of these resources. The final part includes a general evaluation and concluding remarks related to the energy competition in the Eastern Mediterranean.

The Energy Resource Potential and Discoveries in the Region

The debate on hydrocarbon potential in the Eastern Mediterranean has continued for a long time. One of the first studies about this subject was made by the U.S. Geological Survey in 2010.4 According to this study, the Leviathan Basin, which comprises the open sea of Israel, Palestine, the South of Cyprus5 Island, and Lebanon, holds approximately 1.7 billion barrels of crude oil and 3.5 trillion cubic meters of gas. In addition, it is estimated that there are 1.8 billion barrels of crude oil and 6.3 trillion cubic meters of gas reserves in the Nile Delta Basin, which is in the maritime zone of Egypt. Therefore, the hydrocarbon resource potential of only these two basins corresponds to approximately 3.5 billion barrels of oil and 10 trillion cubic meters of gas.

Apart from the abovementioned estimations, some researches show the existence of significant resource potential in the western part of the Eastern Mediterranean. However, detailed drilling operations have not been conducted as yet in these fields. On the other hand, a limited number of seismic surveys are being carried out, especially around the Crete (Girit), Rhodes (Rodos), and Kastellorizo (Meis) islands, to prove the actual hydrocarbon potential of this region. According to private research conducted by Flow Energy in 2012, the energy resource potential of this area is around 1.5 billion barrels of oil and 3.5 trillion cubic meters of gas.6

Since gas hydrates are mainly found in frozen soils and rock structures under the sea, they are considered an important energy resource for the future

Another energy resource in the Eastern Mediterranean is gas hydrate formations. Since gas hydrates are mainly found in frozen soils and rock structures under the sea, they are considered an important energy resource for the future. Gas hydrates are generally in crystal formations that consist of water and gas molecules at high pressure and low temperature.7 Only 1 cubic meter of this energy resource contains 164 cubic meters of natural gas.8 Therefore, gas hydrates have the potential to be a crucial energy source. However, there is currently no commercially viable way to extract them because the reserves are in solid form and therefore the extraction process cannot follow conventional gas drilling techniques. In other words, recent drilling technologies are not suitable enough to extract this energy resource.

Although there is no specific data about the gas hydrate potential in the Eastern Mediterranean, many predictions have been made on this issue. The producible gas hydrate capacity in the Eastern Mediterranean is estimated at around 98 trillion cubic meters.9 Considering the current global natural gas reserves, which are approximately 200 trillion cubic meters, it is noteworthy that the gas hydrate potential in the Eastern Mediterranean alone is roughly half of the world’s total reserves.10 In fact, this situation shows that the competition in the Eastern Mediterranean also includes the struggle to exploit the gas hydrate resources in the region.

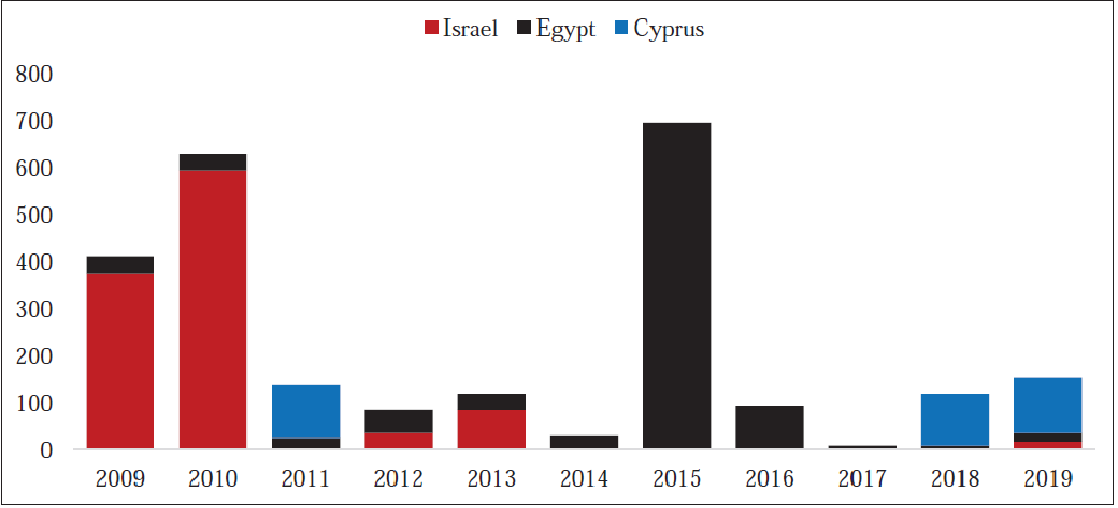

The estimated potential of the hydrocarbon resources in the Eastern Mediterranean is supported by the gas discoveries realized since 2009, making the region of great interest to the energy markets. Graph 1 details the amounts of gas discovered in the Eastern Mediterranean between 2009 and 2019. According to these figures, the first major gas reserves were discovered in Tamar and Leviathan fields offshore from Israel. These fields are the world’s greatest deep-sea gas discoveries in the period 2001 to 2010.11 In between 2011 and 2014, the modest but most significant development was the discovery of the Aphrodite gas field in the South of Cyprus. In August 2015, the Zohr field was discovered off Egypt’s coast by the Italian company ENI. This field is the most significant discovery ever made in the Eastern Mediterranean to date. Recently, a considerable amount of gas reserves was discovered in the Calypso and Glaucus fields located in the South of Cyprus. Along with the other discoveries, approximately 2.5 trillion cubic meters of gas reserves were found in the entire region between 2009 and 2019.12 Therefore, it can be seen that approximately 25 percent of the total natural gas reserve potential has been discovered in the Eastern Mediterranean over the last two decades.

Graph 1: The Natural Gas Discoveries in the Eastern Mediterranean (2009-2019, Billion Cubic Meters)

Source: Rystad Energy13

Source: Rystad Energy13

As can be seen from Graph 1, the discoveries in the region have largely been in the maritime territory of Israel and Egypt. Also, some important reserve fields being identified in the South of Cyprus recently. The discoveries in the Eastern Mediterranean between 2009 and 2019 have an economic value of approximately $460 billion, assuming the average gas prices as of 2019.14 Moreover, the estimated resource potential in the region corresponds to almost $1.8 trillion. Therefore, the economic magnitude of the region provides some clues as to why the Eastern Mediterranean zone has turned into a competitive environment in both local and global terms.

The discovered hydrocarbon resources in the Eastern Mediterranean constitute approximately 0.3 and 6.8 percent of the proven global oil and gas reserves, correspondingly

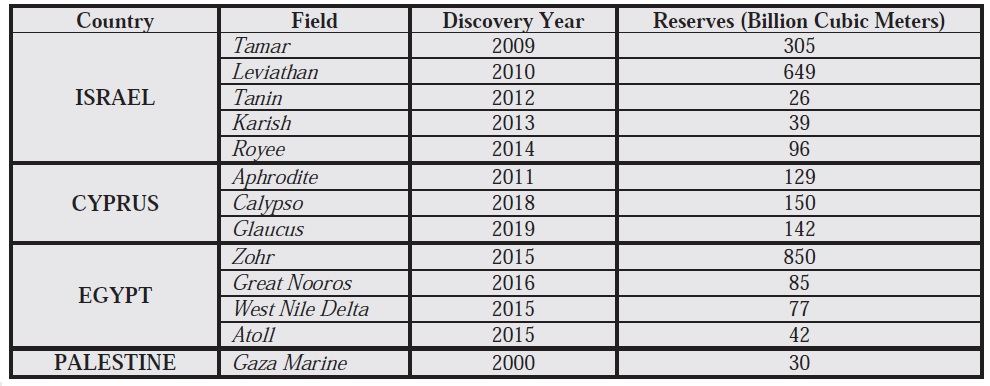

The information related to the location, year, and amount of the discovered natural gas reserves in the Eastern Mediterranean between 2000 and 2019 are given in Table 1. The first important gas discovery was in 2000 in the Gaza Marine field lying offshore from the Gaza Strip. There were no serious exploration activities in the region until 2009 since when the discoveries have increased gradually. The discoveries of Tamar and Leviathan fields in Israel and Zohr field in Egypt, especially, attracted the attention of the global energy markets.

On the other hand, it should be noted that the discoveries in the region to date have not significantly changed the global energy balances. This is because the Eastern Mediterranean Basin has not yet reached a sufficient reserve capacity when compared to the countries that hold a significant portion of global gas reserves. For instance, Russia and Iran have a total of 60 trillion cubic meters of gas resources, approximately 30 percent of the total global gas reserves.15

Table 1: Natural Gas Discoveries in the Eastern Mediterranean (2000-2019)

Source: Compiled by the author16

Source: Compiled by the author16

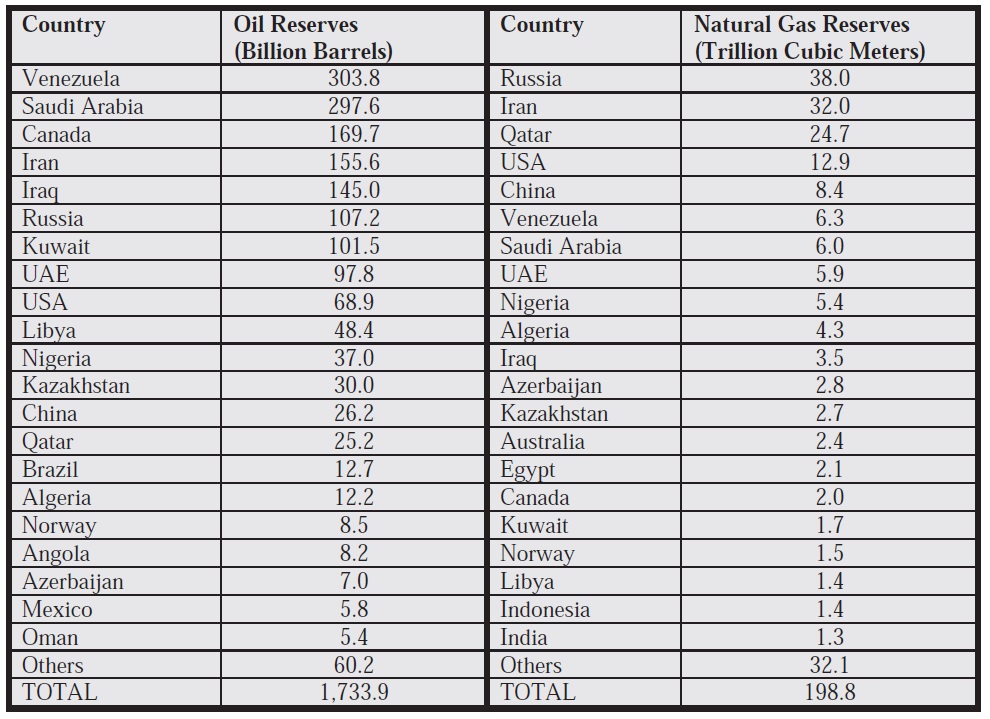

That being said, as of the end of 2019, the resources discovered in the entire Eastern Mediterranean region are equal to the gas reserves that have so far been discovered by Azerbaijan and Norway individually.17 However, as stated previously, the Eastern Mediterranean Basin’s reserve capacity is limited compared to the countries that hold a significant portion of the world’s gas reserves. As shown in Table 2, global proven oil and gas reserves are 1,733.9 billion barrels (244.6 million tons) and 198.8 trillion cubic meters, respectively.18 Hence, the discovered hydrocarbon resources in the Eastern Mediterranean constitute approximately 0.3 and 6.8 percent of the proven global oil and gas reserves, correspondingly.

Table 2: World Proven Oil and Gas Reserves by Countries (2019)

Source: BP Statistical Review of World Energy 202019

Source: BP Statistical Review of World Energy 202019

According to the data shared in this study, several discoveries have been made in the Eastern Mediterranean in the last two decades. However, fields are waiting to be explored, especially in the northern and southern parts of the region. Geological surveys show significant evidence in favor of the hydrocarbon source potential around the islands of Kastellorizo, Rhodes, and Crete.20 While the discoveries made so far confirm the region’s possible reserve estimates, they strengthen the Eastern Mediterranean position in the global drilling and production industry. Therefore, the region offers important opportunities in terms of increasing global oil and gas reserves.

As mentioned previously, the hydrocarbon resources discovered in the Eastern Mediterranean are important in terms of three factors. The first is the economic value of the energy resources in the region. When calculated at the current prices, this value corresponds to approximately $500 billion. Hence, the resource-owner countries will have the opportunity to generate significant financial returns.

As the expectations that the region’s hydrocarbon source potential is much higher than the calculated values, the exploration and drilling activities in this geography have continued for a relatively long time

The second factor is energy supply security. The energy resources in the Eastern Mediterranean provide a strategic advantage for the countries in the region. In general terms, these countries are dependent on external suppliers for hydrocarbon resources which generates economic and political risks. Therefore, they will gain an important advantage as well as reducing these risks, as will be analyzed in detail in this study. The third and last factor is the geopolitical advantage. It is a well-known fact that energy is crucial for the modern world. Therefore, having independent energy resources provides important regional and global advantages to any country.

The discoveries and reserve potential in the Eastern Mediterranean are extremely critical for the coastal states. It is evident that the quantity of gas reserves in the Eastern Mediterranean has the capacity to both support domestic consumption and contribute to the export revenues of the countries in the region. Consequently, there has been an ongoing competition among the parties in the region in terms of claiming the energy resources and transferring them to the foreign markets at the most affordable cost.

The Production and Transfer Processes of the Resources in the Region

Having the potential to create a significant economic benefit, the resources in the Eastern Mediterranean present a great advantage for both the countries in the region and the international energy companies. Currently, the actual production level of the discovered resources in the region is insufficient. However, several investment plans are in progress in order to increase the production volumes and transfer these resources to the energy markets. Terminal, floating platform, and pipeline projects are being conducted mainly in the Leviathan and Zohr fields, the largest discoveries to date, to transmit the resources to domestic markets. As the expectations that the region’s hydrocarbon source potential is much higher than the calculated values, the exploration and drilling activities in this geography have continued for a relatively long time.

Turkey, Egypt, Israel, Lebanon, Libya, Palestine, Greece, and Cyprus, as coastal states of the Eastern Mediterranean, have the exploration and drilling rights in their maritime zones. However, the problem of how these rights and powers will be used in Cyprus has not yet been resolved. Turkey acts with the impetus of all parties on the island should own the rights to these resources equally. On the other hand, other actors in the region claim that the whole island is represented by the GASC, and hence these rights should be used by the Greek Cypriot side. Until the disputes are resolved on a legitimate basis, the process of producing the discovered resources around Cyprus will be delayed.

In other respects, the production phase has started in some specific zones of the Eastern Mediterranean where there are no disputes on maritime boundaries. Israel, which has discovered significant gas resources in the region, started production activities in March 2013, 4 years after the discovery, in the Tamar field.21 Until now, approximately 60 billion cubic meters of gas have been produced from this field. While some of this production meets Israel’s domestic demand, the rest is exported. The first natural gas export from the Tamar field was made to Jordan in January 2017.22 As a result of the transfer agreement between the two states, Israel will supply annually 2 billion cubic meters of gas to Jordan’s domestic consumption for 15 years.23 In addition, as part of the EastMed Gas Submarine Pipeline Agreement signed between Israel and Egypt in 2005, a total quantity of 25 billion cubic meters of gas will be transferred from Tamar over 15 years.24 This pipeline agreement was updated in 2019, and the gas has started to flow to Egypt since the beginning of 2020.25

The Leviathan gas field, also located in Israel’s offshore, was discovered in 2010, and production started at the end of 2019.26 In the first stage, it is planned to produce 21 to 24 billion cubic meters of natural gas annually, with projections to increase the production capacity to transfer 45 and 60 billion cubic meters of gas annually to Jordan and Egypt, respectively.

In addition, the development activities have continued in the Tanin and Karish fields off the coast of Israel. Within the scope of these activities, establishing a Floating Storage and Regasification Unit (FSRU) in the region is on the agenda. Studies started in this region in 2019 to increase the reserve quantities for export, with the first gas production planned for 2021.27

As one of the important resource owner countries in the region, Egypt made the first gas discovery in 1969 at the Abu Qir-1 field.28 Thereafter, it continued exploration and drilling activities in the Eastern Mediterranean, however, since the discoveries were insufficient, they were only used to support the country’s domestic consumption. After 2014, with the discovery of further gas fields off Egypt’s coast, the production activities started at the Great Nooros in 2015, West Nile Delta in 2017, and Zohr in 2017. Among these fields, the Zohr is the largest discovery in the Eastern Mediterranean so far (see Table 1 for the details). The latest data show that this field’s supply capacity has increased gradually, and the daily production level has reached around 76 million cubic meters.29 Furthermore, the production margin of this field is targeted to reach about 90 million cubic meters per day. In addition to this, in 2019, 39 million cubic meters of natural gas were produced daily from the West Nile Delta field, which is approximately 20 percent of Egypt’s gas needs.30 Apart from the abovementioned fields, another reserve area discovered Egypt’s offshore is Atoll, located in the East Nile Delta field. The reserve potential of this field was announced as 42 billion cubic meters by British Petroleum (BP).31 In this field, the production started in 2018, and 10 million cubic meters of gas are planned to be transferred daily to Egypt’s national gas network.

Besides Israel and Egypt, another actor that carries out exploration and drilling activities in the Eastern Mediterranean is GASC. However, the activities of GASC in the region are regarded as unfair practices by Turkey and the TRNC. As a matter of fact, the Greek Administration has unilaterally signed Exclusive Economic Zone (EEZ) agreements with Egypt, Lebanon, and Israel in 2003, 2007, and 2010, respectively. Thereafter, acting as a sole representative of the island, GASC unfairly divided the maritime zones of Cyprus Island into blocks and initiated various exploration activities in these areas. The Greek Administration has also authorized several international energy companies to conduct the exploration and drilling operations around the island.32 With the discoveries of Aphrodite, Calypso, and Glaucus fields, the attention of actors in the Eastern Mediterranean has recently focused on this region. According to the estimates, the initial gas production capacity of the Aphrodite field is 22 million cubic meters per day and 8 billion cubic meters on an annual basis.33 On the other hand, there are still no production plans for the other gas fields discovered in the so-called EEZ of GASC. Moreover, it is not yet clarified when the gas production phase will start in these fields. The production plans for these fields have been postponed due to both the disputes on maritime boundaries and the financial losses of the companies during the COVID-19 pandemic.

The other countries of the region, Syria, Palestine, Lebanon, and Libya have not yet started the drilling and production activities. The political and military instabilities in Syria, Palestine, and Libya are the most important reasons for the delay. Lebanon, on the other hand, is in a better position with regards to the exploration of hydrocarbon resources in its maritime zones compared to the countries mentioned above. In 2010, Lebanon presented a map to the United Nations (UN) for determining its maritime zones.34 Subsequently, in 2017 the Lebanese government decided to begin exploration activities in the uncontroversial fields. However, they have not as yet started the exploration and drilling operations in the region.

On the other hand, Libya, one of the essential oil producer countries in the region, has continued the strategic moves, necessary to maintain its rights in the Eastern Mediterranean. Libya and Turkey signed a Maritime Delimitation Agreement on November 27, 2019. This agreement can be considered as a game-changer move for both Libya and Turkey in terms of the political balances in the region. Besides, as a result of this process, the way was paved for both countries to cooperate in the Eastern Mediterranean.

As an alternative to the EastMed project, a pipeline planned to pass over Turkey remains on the agenda. With this pipeline, it would be possible to transport the natural gas from the Eastern Mediterranean region to Europe via the Turkish territories

Turkey is yet another important actor in the Eastern Mediterranean. In recent years, especially, the country has conducted an active exploration and drilling policy in the region. In this context, a total of 8 wells (Alanya-1, Finike-1, Magosa-1, Karpaz-1, Güzelyurt-1, Narlıdere-1, Lefkoşa-1, and Selçuklu-1) have been drilled by the Turkish Petroleum Cooperation (Türkiye Petrolleri Arama Ortaklığı / TPAO) in the Eastern Mediterranean since 2018.35 Although there is no producible resource discovery from these wells, Turkey’s exploration and drilling activities have continued consistently in the region. As a matter of fact, it is highly likely that Turkey will explore new fields in the region and start production because, as a net importer of fossil fuels, the possibility of finding new hydrocarbon resources in the region provides an important motivation for Turkey.

Turkey’s foreign dependency on oil and gas is about 9336 and 9937 percent, respectively. Thus, Turkey’s hydrocarbon exploration activities are extremely important in order to decrease foreign dependency on fossil fuels and the economic risks arising from this high dependence. For this reason, the deepwater oil and gas exploration efforts of Turkey have accelerated since the beginning of the 2000s. In this context, by creating a domestic seismic and drilling fleet, Turkey has independently continued the exploration activities in the region.

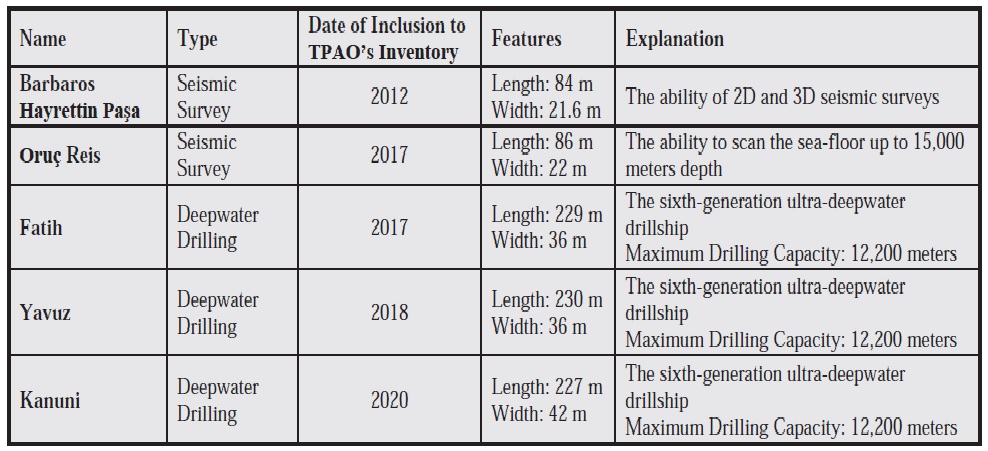

Since 2012, Turkey has followed an active exploration strategy in the Eastern Mediterranean. Initially, the Barbaros Hayrettin Paşa and Oruç Reis seismic survey vessels were included in the TPAO’s inventory in 2012 and 2017, respectively. Consequently, Turkey has become an important actor in the region with Fatih, Yavuz, and Kanuni deepwater drill-ships. These vessels constitute approximately 20 percent of the global deepwater drilling fleet.38 The main features of these vessels are outlined in Table 3.

Table 3: Turkey’s Seismic Survey and Drilling Vessels

Source: Anadolu Agency39

Source: Anadolu Agency39

These vessels provide significant advantages to Turkey in the Eastern Mediterranean, as exemplified by the increase in Turkey’s efficiency in the region, observed in the recent COVID-19 crisis. With the spread of the COVID-19 epidemic around the world, global oil prices declined sharply. As a result of these price movements, the major energy companies that continue their activities in the Eastern Mediterranean have faced some financial troubles.

In the first quarter of 2020, some of the leading international energy companies, such as ExxonMobil, TOTAL, and ENI that carry out exploration and drilling operations in the region, were adversely affected in financial terms. During this period, one of the most effective energy companies in the Eastern Mediterranean, ENI, declared a loss in profits of 44 percent compared to the first quarter of 2019.40 Moreover, the profit losses of Total and ExxonMobil are estimated approximately as 3541 and 1242 percent, respectively, for the same period. In the meantime, the profit rates of giant energy companies such as BP and Shell, which are two important actors in the global oil market, have decreased substantially.43 Therefore, the activities related to energy resources in the Eastern Mediterranean have lost their appeal of being a profitable investment for many oil companies during the COVID-19 process.

In this period, first, ExxonMobil decided to postpone its activities in the so-called Block-10 located in the South-West of Cyprus.44 Later on, ENI and TOTAL companies announced that they had stopped their drilling activities in the region until the first quarter of 2021.45 Thus, the exploration and drilling activities of these companies, which were planned to be carried out in 2020, were postponed for at least one year due to the risks and uncertainty in the global energy markets, due to the decrease in demand as a result of the COVID-19 epidemic.

The LNG option can be accepted as the optimal way for the short term in transferring gas resources from the Eastern Mediterranean to the international markets

Turkey, on the other hand, has continued its exploration and drilling activities in the region with its domestic vessels. Indeed, the temporarily suspended activities of relevant international energy companies have provided an important advantage to Turkey. In this sense, Turkey has focused on exploring new resource areas and expanding its dominance in the region. This process is accepted as extremely important in strengthening Turkey’s strategic position in the Eastern Mediterranean. At this stage, it can be said that Turkey’s competition capacity vis-à-vis the energy companies operating in the region has increased.

Potential Transfer Routes for the Energy Resources in the Region

Besides exploration, drilling, and production activities, the exportation of the energy resources in the region leads to several financial, commercial, legal, and geopolitical difficulties. In general, three scenarios become prominent within the context of transferring the energy resources from the region to the foreign markets. As can be seen from Map 1, the first and most popular of these transport options is the EastMed Natural Gas Pipeline project. The second is the Turkey route. The last one is transferring the resources by transforming them into Liquified Natural Gas (LNG) formation.46

Map 1: Possible Transfer Routes for the Eastern Mediterranean Gas Resources

Source: SETA

Source: SETA

The EastMed project has a total length of 1,900 km, including 1,300 km offshore and 600 km onshore. It starts from the Leviathan basin off Israel and follows a route as noted below:47

— 200 km offshore pipeline connecting the Leviathan basin and Cyprus,

— 700 km offshore pipeline connecting Cyprus and Crete,

— 400 km offshore pipeline between Crete and mainland Greece,

— 600 km onshore pipeline from the South to the North-West of Greece.

Through this project, the resources are planned to be transferred from the Eastern Mediterranean to Europe as well as to provide gas to the regions on the transit route. Eventually, 15 billion cubic meters of Europe’s gas need is planned to be met from the Eastern Mediterranean via this pipeline. The construction process of the EastMed Pipeline is envisaged to be completed by 2025.

On the other hand, this project is not regarded as a profitable investment in terms of the costs and the probability of increasing Europe’s gas supply prices.48 Compared to the other pipelines in the region, the EastMed project’s estimated investment cost is approximately $20 billion.49 Therefore, when this project is completed, it can be said that the construction costs will be reflected in the purchase prices of Europe, and it is expected that the natural gas will be provided at a more expensive price than desired.

As an alternative to the EastMed project, a pipeline planned to pass over Turkey remains on the agenda. With this pipeline, it would be possible to transport the natural gas from the Eastern Mediterranean region to Europe via the Turkish territories.50 Currently, the natural gas transfer infrastructure of Turkey is sufficient. Therefore, this situation provides an advantage to the country in terms of the transfer route in question. Furthermore, the achievements of transferring the energy resources by Trans Anatolian Natural Gas Pipeline (TANAP) and TurkStream projects are reference points for Turkey. Additionally, a pipeline that passes-through Turkey will be more cost-effective than the EastMed project51 because almost the whole part of the Turkey route will be constructed as an onshore pipeline. These calculations show that the Turkey route may be financially more advantageous than the EastMed project, which consists mostly of an offshore pipeline.

The third and last option discussed in the region is transporting the gas resources as LNG. The LNG trade has reached a significant level in today’s world. In fact, while 50.7 percent of global gas trade was conducted through pipelines, the remaining 49.3 percent was transmitted as LNG in 2019.52 The estimations show that LNG trade volume will continue to increase in the future, and its share in total gas trade will reach 75 percent by 2040.53

Unless the discovered reserves produce, they will just be hypothetical numerical values and the countries in the region will not receive an economic benefit from these resources

The LNG option can be accepted as the optimal way for the short term in transferring gas resources from the Eastern Mediterranean to the international markets.54 Since the Eastern Mediterranean Basin is close to the Asia-Pacific region and transferring the gas resources to this region is very costly, the Asian market can be an appropriate place for trading the resources in the Eastern Mediterranean. Today, the countries importing the most LNG in the world are, in decreasing order, Japan, China, South Korea, India, and Taiwan.55 Therefore, resources in the Eastern Mediterranean can offer an important alternative for these countries to enhance the source-country diversification in energy supply security. Transferring the resources in the Eastern Mediterranean as LNG is also considered a suitable option for the European gas market in the short term. Europe has been evaluating different scenarios for a long time to reduce its high-dependency on Russian natural gas. From this point of view, the LNG option provides crucial opportunities to Europe in minimizing the risks on energy supply security and ensuring continuous gas supply.

Among the existing LNG facilities located in the Eastern Mediterranean, the terminals in Turkey and Egypt attract attention. Egypt has two terminals in Idku and Damietta regions with a total gasification capacity of 19 billion cubic meters.56 On the other hand, with two LNG plants (Marmara Ereğli and EgeGaz Aliağa) and two Floating Storage and Regasification Units (FSRU) (Etki Liman and Hatay-Dörtyol), the top country in the region in terms of LNG facility capacities is Turkey. The country has a total of 45.6 billion cubic meters of gasification potential.57 This capacity means that Turkey has an apparent strategic advantage in the field of LNG facilities compared to other countries in the region. Currently, Egypt, Jordan, Malta, and Turkey have FSRU facilities in the Eastern Mediterranean.58 In addition to these, Israel plans to invest in the FSRU field soon.59 With these units, Israel’s gasification capacity is aimed to reach 3.5 to 7 billion cubic meters annually.

Natural Gas Consumption Tendencies of the Countries in the Region

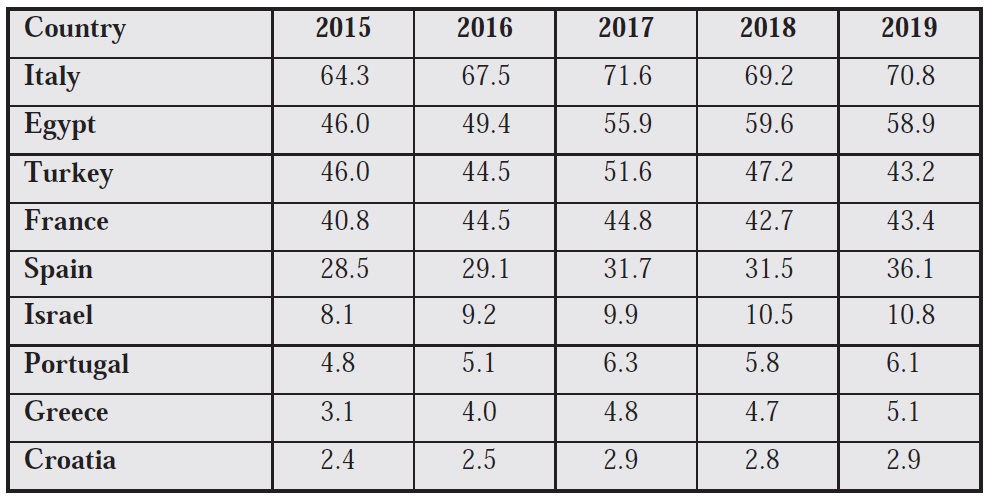

In addition to the transfer options and energy infrastructure, the natural gas consumption trend of countries in the region is also a significant point within the frame of the discovered resources in the Eastern Mediterranean. According to the data given in Table 4, the top three countries in annual natural gas consumption are Italy, Egypt, and Turkey, respectively. Moreover, the natural gas consumption tendencies of the countries in the region are gradually increasing. The predictions show that the energy demand of the countries close to the Eastern Mediterranean will increase by about 40 percent by 2040.60 Furthermore, the natural gas dependency rates of the countries in the region are extremely high, therefore the Eastern Mediterranean’s gas potential is of critical importance not only for the global energy markets but also for meeting the domestic demands of the countries in the region. Consequently, when the region’s general energy profile is examined, the efforts of securing gas resources and offering these resources to domestic consumption at the lowest cost are seen as strategic goals for all of the regional countries.

Table 4: The Annual Gas Consumption of Countries Close to the Eastern Mediterranean Region (2015-2019, Billion Cubic Meters)

Source: BP Statistical Review of World Energy61

Source: BP Statistical Review of World Energy61

On the other hand, the hydrocarbon discoveries in the region offer opportunities to countries with low gas consumption, such as Israel, to become exporters of gas. In this regard, it is clear that the energy resources in the Eastern Mediterranean will provide a significant economic benefit to the resource-owner countries in terms of meeting both the domestic demand and exportation. In fact, this situation can be accepted as the main reason for the competition of obtaining energy resources in the region. In other words, the energy equation in the Eastern Mediterranean will shape around owning the resources and transferring them to the foreign markets at a reasonable cost.

Conclusion

The amount of recent gas discoveries throughout the Eastern Mediterranean region equals the reserves that Azerbaijan, Norway, Kazakhstan, and Australia have discovered separately to date. In this respect, the discoveries in the region are important both locally and globally. On the other hand, unless the discovered reserves produce, they will just be hypothetical numerical values and the countries in the region will not receive an economic benefit from these resources. In this sense, since the region is a political and economic competition area, there are serious handicaps in obtaining a fully financial gain from the resources in the Eastern Mediterranean.

Considering the region as a whole, several areas are waiting to be explored as well as the fields where the drilling activities have been carried out. In the western parts of the region, it is estimated that there is a high hydrocarbon resource potential around the islands of Kastellorizo, Rhodes, and Crete. According to the seismic surveys, considerable amounts of gas hydrate reserves are detected in these fields. Moreover, the Eastern Mediterranean’s gas hydrate potential is predicted as approximately half of the current global gas reserves. Therefore, the competition of having the resources in the region is also shaped on the basis of gas hydrates, which are considered as the energy source of the future.

The quantity of reserves discovered so far in the region is one-fourth of the estimated potential. The current production volume, on the other hand, is insufficient. The main underlying reasons for this low production level are the multilateral structure in the region and the consequent inability to form a cooperative environment. In this sense, the existence of many actors in the region deepens the ongoing competition in the Eastern Mediterranean.

The main motivation for investigating the energy facts in the Eastern Mediterranean is to analyze the general situation in the region in terms of hydrocarbon resources

On the other hand, this multilateral structure offers several opportunities for regional and global cooperation. However, due to the maximalist policies of some countries like Greece and GASC, it is difficult to design an environment conducive to cooperation throughout the Eastern Mediterranean. In this context, the most problematic area of the region in exploration, drilling, and production processes is considered to be the maritime zones of the island of Cyprus. One of the main problems here is the emergence of disputed maritime areas. Thus, the exploration and drilling activities in this field have lost continuity, and the problem of hierarchy of authority in Cyprus has become a focal point of the discussions. Therefore, unless the conflicts in this region are resolved, the issues of sharing the discovered resources will continue.

Another issue in the Eastern Mediterranean is about the transfer routes of the extracted resources to the foreign markets in the medium and long terms. In this sense, the EastMed project is the most prominent among the three possible scenarios. However, as an alternative to the EastMed Pipeline Project, the Turkey route can be considered more advantageous in terms of cost and safety. In addition to these, the last transfer option is transporting the resources as LNG. As well as the exploration and production operations, transferring processes of the resources from the region to foreign markets is extremely important. For this reason, there is serious competition in the region over the possible transfer routes.

In order to obtain a financial gain from the energy resources in the region, the political and economic conflicts should be minimized, and a joint cooperation platform must be established in the Eastern Mediterranean

The main motivation for investigating the energy facts in the Eastern Mediterranean is to analyze the general situation in the region in terms of hydrocarbon resources. In this sense, the discovered resources (to date) and the potential in the region have given enough impetus to transform the region into a competitive environment. This competition is not only on having the energy resources but also gaining political and strategic advantage in the region. Under these circumstances, the main objective in the Eastern Mediterranean is the utilization of the regional energy resources economically, geopolitically, and strategically.

To better understand the local and global competition for the region’s energy resources, the arguments of this study should be evaluated as a whole. There are at least three dimensions to the energy equation in the Eastern Mediterranean. These can be categorized as economic, political, and strategic advantages. In this sense, when the expected returns of having the energy resources in the region are considered, it can be understood that the environment of conflict or rivalry in the Eastern Mediterranean will deepen gradually. However, it should be noted that competition must give way to cooperation in order to gain economic benefit from the wealth of the region. Above all, designing a common platform with the participation of all parties in the region is crucial in terms of local and global energy markets.

As a result, it is clear that there is a multidimensional equation related to the energy resources in the Eastern Mediterranean. The countries in the region, global powers, and major energy companies must all be accepted as the parameters of this equation. This structure undoubtedly raises the question of how the resources in the region will be exploited. Moreover, this situation is causing the existing competitive environment in the region to deepen. On the other hand, the energy resources and economic value of these resources have the potential to create a catalytic effect in the stabilization of the Eastern Mediterranean. Therefore, in order to obtain a financial gain from the energy resources in the region, the political and economic conflicts should be minimized, and a joint cooperation platform must be established in the Eastern Mediterranean.

Endnotes

1. This information is obtained from the Israeli Ministry of Energy and the Egyptian Ministry of Petroleum and Mineral Resources, correspondingly. See, “Exploration History,” Israel Ministry of Energy, retrieved from https://www.energy-sea.gov.il/English-Site/Pages/Oil%20And%20Gas%20in%20Israel/History-of-Oil--Gas-Exploration-and-Production-in-Israel.aspx; “Petroleum History,” Egypt Ministry of Petroleum and Mineral Resources, retrieved from https://www.petroleum.gov.eg/en/about-ministry/petroleum-industry/Pages/petroleum-industry-development.aspx.

2. Umut Kedikli and Taşkın Deniz, “Enerji Kaynakları Mücadelesinde Doğu Akdeniz Havzası ve Deniz Yetki Alanları Uyuşmazlığı,” Alternatif Politika, 7, No. 3 (October 2015), pp. 399-424.

3. Tolga Demiryol, “Between Security and Prosperity: Turkey and the Prospect of Energy Cooperation in the Eastern Mediterranean,” Turkish Studies, Vol. 20, No. 3 (2019), pp. 442-464.

4. “Assessment of Undiscovered Oil and Gas Resources of the Levant Basin Province, Eastern Mediterranean,” S. Geological Survey, (May 2010), retrieved from https://pubs.usgs.gov/fs/2010/3027/pdf/FS10-3027.pdf, pp. 1-4.

5. The expression of Cyprus covers all the parties (TRNC and GASC) of the island.

6. Oleg Vukmanovic and Stephen Jewkes, “Greece Looks Out to Sea for Gas Wealth Salvation,” Reuters, (October 3, 2012).

7. Şükrü Merey and Sotirios Nik. Longinos, “Doğu Akdeniz’in Gaz Hidrat Potansiyeli,” Maden Tetkik ve Arama Dergisi, 160, (2019), pp. 117-134.

8. “Türkiye’nin Gaz Hidrat Yol Önerisi,” Dünya Enerji Konseyi Türk Milli Komitesi, (January 18, 2018), retrieved from https://www.dunyaenerji.org.tr/turkiyenin-gaz-hidrat-yol-haritasi-onerisi/.

9. Şükrü Merey and Sotirios Nik. Longinos, “Does the Mediterranean Sea Have Potential for Producing Gas Hydrates?” Journal of Natural Gas Science and Engineering, 55, (July 2018), pp. 113-134.

10. “Statistical Review of World Energy 2020,” British Petroleum (BP), (June 2020), retrieved from https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html, p. 32.

11. Gongcheng Zhang et al., “Giant Discoveries of Oil and Gas Fields in Global Deepwaters in the Past 40 Years and the Prospect of Exploration,” Journal of Natural Gas Geoscience, Vol. 4, No. 1 (February 2019), pp. 1-28.

12. Ana Stanič and Sohbet Karbuz, “The Challenges Facing Eastern Mediterranean Gas and How International Law can Help Overcome Them,” Journal of Energy and Natural Resources Law, (October 2020), pp. 1-35.

13. This graph is formed based on the data available at Rystad Energy’s website. See UCube Database, retrieved from https://www.rystadenergy.com/energy-themes/oil--gas/upstream/u-cube/.

14. This calculation is based on Germany’s natural gas import price in 2019. The data were obtained from the “Statistical Review of World Energy 2020,” retrieved from https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html, p. 39.

15. “Statistical Review of World Energy 2020,” p. 32.

16. The data are obtained from several sources as follows: The data of the Tamar, Leviathan, and Aphrodite fields were obtained from the website of Delek Drilling company (https://www.delekdrilling.com/). The data of the Tanin and Karish fields were obtained from the website of Energean company (https://www.energean.com/). The data of the Royee field was obtained from the website of Israel Opportunity – Energy Resources company (https://www.oilandgas.co.il/en/home/). The data of the Calypso and Gaza fields were obtained from the website of Reuters News Agency (https://www.reuters.com/). The data of the Glaucus field was retrieved from the website of ExxonMobil company (https://corporate.exxonmobil.com/). The data of the Zohr, Great Nooros, and West Nile Delta fields were retrieved from the website of ENI company (https://www.eni.com/en-IT/home.html). The data of the Atoll field was retrieved from the website of the British Petroleum (BP) company (https://www.bp.com/).

17. “Statistical Review of World Energy 2020.”

18. “Statistical Review of World Energy 2020.”

19. This table is formed based on the data available at the BP Statistical Review of World Energy 2020 report. See the total proved oil and natural gas reserves of the world on pages 14 and 32, respectively. The report is retrieved from https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html.

20. Sohbet Karbuz, “Doğu Akdeniz’de Ne Kadar Doğal Gaz Var?” Bilkent Üniversitesi Enerji Politikaları Araştırma Merkezi - Bilkent Enerji Notları, No. 12 (July 2019), p. 6.

21. “Tamar Gas Field,” Delek Drilling Company, retrieved October 30, 2020, from https://www.delekdrilling.com/natural-gas/gas-fields/tamar.

22. Isabella Ruble, “European Union Energy Supply Security: The Benefits of Natural Gas Imports from the Eastern Mediterranean,” Energy Policy, Vol. 105, (June 2017), pp. 341-353.

23. “Tamar Gas Field,” Delek Drilling Company.

24. Brenda Shaffer, “Israel-New Natural Gas Producer in the Mediterranean,” Energy Policy, Vol. 39, No. 9 (September 2011), pp. 5379-5387.

25. Dov Lieber, “Israeli-U.S. Consortium Begins Pumping Natural Gas to Egypt,” The Wall Street Journal, (January 15, 2020), retrieved from https://www.wsj.com/articles/israeli-u-s-consortium-begins-pumping-natural-gas-to-egypt-11579097813.

26. “Leviathan Gas Field,” Delek Drilling Company, retrieved October 30, 2020, from https://www.delekdrilling.com/natural-gas/gas-fields/leviathan.

27. Theodoros Tsakiris, “The Importance of East Mediterranean Gas for EU Energy Security,” The Cyprus Review, Vol. 30, No. 1 (Spring 2018), pp. 25-50.

28. Suleiman A. Bengharsa, “The Egyptian Natural Gas Remedy,” The Journal of Energy and Development, Vol. 17, No. 2 (Spring 1992), pp. 291-301.

29. “Zohr,” ENI Company, retrieved October 30, 2020, from https://www.eni.com/en-IT/operations/egypt-zohr.html.

30. “Nooros,” ENI Company, retrieved October 30, 2020, from https://www.eni.com/en-IT/operations/egypt-nooros.html.

31. “BP Sanctions ‘Fast-Track’ Development of Atoll Discovery in Egypt,” British Petroleum (BP), (June 20, 2016), retrieved from https://www.bp.com/en/global/corporate/news-and-insights/press-releases/bp-sanctions-fast-track-development-of-atoll-discovery-in-egypt.html.

32. Hayriye Kahveci Özgür, “Eastern Mediterranean Hydrocarbons: Regional Potential, Challenges Ahead, and the ‘Hydrocarbonization’ of the Cyprus Problem,” Perceptions: Journal of International Affairs, Vol. 22, No. 2 (Summer-Autumn 2017), pp. 31-56.

33. “Aphrodite Gas Field,” Delek Drilling Company, retrieved October 31, 2020, from https://www.delekdrilling.com/project/aphrodite-gas-field.

34. “Deposit of a Chart and Lists of Geographical Coordinates of Points Defining the Western, Northern and Southern Limits of Lebanon’s Exclusive Economic Zone,” United Nations, retrieved from https://www.un.org/Depts/los/LEGISLATIONANDTREATIES/STATEFILES/LBN.htm.

35. “TPAO Faaliyet Alanları-Deniz,” Türkiye Petrolleri Anonim Ortaklığı (TPAO), retrieved November 2, 2020, from https://www.tpao.gov.tr/deniz.

36. “Petrol Piyasası 2019 Sektör Raporu,” Enerji Piyasası Düzenleme Kurumu (EPDK), retrieved November 2, 2020, from https://www.epdk.gov.tr/Detay/Icerik/3-0-107/yillik-sektor-raporu.

37. “Doğal Gaz Piyasası 2019 Sektör Raporu,” Enerji Piyasası Düzenleme Kurumu (EPDK), retrieved November 2, 2020, from https://www.epdk.gov.tr/Detay/Icerik/3-0-94/dogal-gazyillik-sektor-raporu.

38. “Sakarya Sahasının Tuna-1 Bölgesindeki Toplam Doğal Gaz Rezervi Miktarı 405 Milyar Metreküpü Buldu,” Presidency of the Republic of Turkey, retrieved October 21, 2020, from https://www.tccb.gov.tr/haberler/410/122393/-sakarya-sahasinin-tuna-1-bolgesindeki-toplam-dogal-gaz-rezervi-miktari-405-milyar-metrekupu-buldu-.

39. Murat Temizer, “Türkiye’nin Denizlerdeki Enerji Filosu,” Anadolu Agency, (August 22, 2020), retrieved from https://www.aa.com.tr/tr/ekonomi/turkiyenin-denizlerdeki-enerji-filosu/1949802.

40. “ENI First Quarter 2020 Results,” ENI Company, retrieved October 21, 2020, from https://www.eni.com/en-IT/media/press-release/2020/04/eni-first-quarter-2020-results.html.

41. Sibel Morrow, “Total’s Net Profit Decreases 35% in Q1 Amid Oil Crisis,” Anadolu Agency, (May 5, 2020), retrieved from https://www.aa.com.tr/en/energy/oil/total-s-net-profit-decreases-35-in-q1-amid-oil-crisis/29177.

42. Tomi Kilgore, “Exxon Mobil Swings to a Loss and Revenue Falls 12%, as COVID-19 Weighs on Oil Demand,” Market Watch, (May 1, 2020), retrieved from https://www.marketwatch.com/story/exxon-mobil-swings-to-a-loss-and-revenue-falls-12-as-covid-19-weighs-on-oil-demand-2020-05-01.

43. Katherine Dunn, “ExxonMobil’s CEO Is Banking on a Return to Normal—but Most Others in the Energy Business Aren’t so Sure,” Fortune, (May 1, 2020), retrieved from https://fortune.com/2020/05/01/exxonmobil-earnings-q1-exxon-ceo-energy-industry/.

44. “Doğu Akdeniz’deki Denkleme Petrol Ayarı,” TRT Haber, (April 15, 2020), retrieved from https://www.trthaber.com/haber/gundem/dogu-akdenizdeki-denkleme-petrol-ayari-476265.html.

45. Mehmet İkbal Aslan, “ENI ve Total Şirketleri, Rumların Sözde Münhasır Ekonomik Bölgesindeki Sondaj Çalışmalarını Erteledi,” Anadolu Agency, (May 5, 2020), retrieved from https://www.aa.com.tr/tr/dunya/eni-ve-total-sirketleri-rumlarin-sozde-munhasir-ekonomik-bolgesindeki-sondaj-calismalarini-erteledi/1829255.

46. Liquefied Natural Gas (LNG) is the liquid phase of natural gas by being cooled to -162 degrees at atmospheric pressure. In this way, the volume of the liquified gas shrinks approximately 600 times. Therefore, the transportation and storage processes are easier and safer. See, Michelle Michot Foss, “Introduction to LNG,” Center for Energy Economics, Bureau of Economic Geology, Jackson School of Geosciences, University of Texas, (June 2012), retrieved from https://www.beg.utexas.edu/files/energyecon/global-gas-and-lng/INTRODUCTION%20TO%20LNG%20Update%202012.pdf, p. 6-7.

47. “EastMed Project,” IGI Poseidon, retrieved on November 20, 2020, from http://www.igi-poseidon.com/en/eastmed.

48. Vedat Yorucu and Özay Mehmet, Europe’s Energy Security and the Southern Energy Corridor, (Cham: Springer, 2018), p. 18.

49. “Gökhan Güler, “Yunanistan’ın Eastmed Blöfü ve Türk Akımı,” Türkiye Uluslararası İlişkiler ve Stratejik Analizler Merkezi (TÜRKSAM), (December 10, 2018), retrieved from http://turksam.org/yunanistanin-eastmed-blofu-ve-turk-akimi.

50. Emre Erşen and Mitat Çelikpala, “Turkey and the Changing Energy Geopolitics of Eurasia,” Energy Policy, Vol. 128, (May 2019), pp. 584-592.

51. Andrea Prontera and Mariusz Ruszel, “Energy Security in the Eastern Mediterranean,” Middle East Policy, Vol. 24, No. 3 (Fall 2017), pp. 145-162.

52. “Statistical Review of World Energy 2020,” p. 40.

53. “LNG Outlook 2020,” Shell, (February 2020), retrieved from https://www.shell.com/promos/overview-shell-lng-2020/_jcr_content.stream/1584588383363/7dbc91b9f9734be8019c850f005542e00cf8ae1e/shell-lng-outlook-2020-march.pdf.

54. Matthew J. Bryza, “Eastern Mediterranean Natural Gas: Potential for Historic Breakthroughs among Israel, Turkey and Cyprus,” Turkish Policy Quarterly, Vol. 12, No. 3 (Fall 2013), pp. 35-44.

55. “World LNG Report 2020,” International Gas Union (IGU), (April 27, 2020), retrieved from https://igu.org/app/uploads-wp/2020/04/2020-World-LNG-Report.pdf, p. 18.

56. Sohbet Karbuz, “Energy Economy, Finance and Geostrategy,” in Andre B. Dorsman, Volkan Ş. Ediger, and Mehmet B. Karan (eds.), Geostrategic Importance of East Mediterranean Gas Resources, (Cham: Springer, 2018), pp. 237-255.

57. İsmail Kavaz, “Doğu Akdeniz’deki Enerji Kaynaklarının Olası Transfer Güzergahları,” in Kemal İnat, Muhittin Ataman, and Burhanettin Duran (eds.), Doğu Akdeniz ve Türkiye’nin Hakları, (İstanbul: SETA Yayınları, 2020), pp. 275-294.

58. “Gas Markets in the Mediterranean,” Association of Mediterranean Energy Regulators (MEDREG), (September 2018), retrieved from http://www.medreg-regulators.org/Portals/_default/Skede/Allegati/Skeda4506-292-2018.9.28/14-Leaflet_GAS_09-2018.pdf?IDUNI=tbgp5qhjmpp53hgjmxzppjp48795, p. 6.

59. Tova Cohen, “Leviathan Partners Considering LNG Facility Offshore Israel,” Reuters, (July 30, 2019), retrieved from https://www.reuters.com/article/us-israel-natgas-leviathan/leviathan-partners-considering-lng-facility-offshore-israel-idUSKCN1UP0SM.

60. “Mediterranean Energy Perspectives 2018-Exclusive Summary,” Observatoire Méditerranéen de l’Energie (OME), (2018), retrieved from https://www.ome.org/wp-content/uploads/2020/05/EXECUTIVE-SUMMARY-MEP-2018.pdf, p. 2.

61. “Statistical Review of World Energy 2020,” p. 36. Since the annual gas consumption amounts of countries such as Cyprus, Jordan, Lebanon, and Libya are very low, they are not included in the table.