The traditional advice given to the prince in the Ottoman Empire (late fifteenth century) was:

ŌĆ£Look with favor on the merchants in the land; always care for them; let no one harass them; let no one order them about; for through their trading, the land becomes prosperous and by their wares, cheapness (or inexpensiveness) abounds in the world.ŌĆØ1

Turkish economy has been subject to a variety of analyses, based on different perspectives. Depending on the analytical tools employed, however, the scope of and the inferences from the analyses change dramatically. Based on an assessment of TurkeyŌĆÖs new foreign policy orientation through its foreign trade performance, this paper is focused on the specific arguments around trade policies and takes on a political economy perspective. The period of 2002-2008 under the AK PartyŌĆÖs administration is regarded as a significant landmark in terms of TurkeyŌĆÖs foreign policy as well as its trade orientation. A new multi-dimensional approach grounded in a theoretical background re-defining the countryŌĆÖs position as a central power -rather than peripheral- power thrust Turkey into a new era. The country has engaged in new bilateral relationships, strongly motivated by economic and commercial demands in the last decade, particularly during the AK PartyŌĆÖs term.

TurkeyŌĆÖs changing foreign trade structure also fits the new global economic trends that began in the 1990s

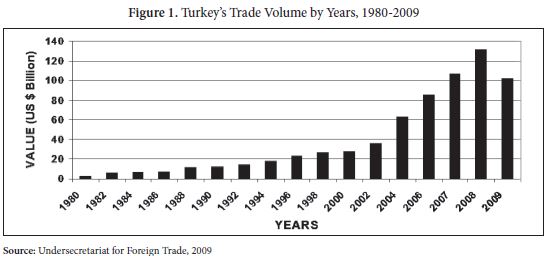

Along with many other aspects, TurkeyŌĆÖs increasing economic performance manifested itself in the continuous surge in the volume of its export which reached 36 billion US Dollars in 2002, 47.3 billion US Dollars in 2003, 63.2 billion US Dollars in 2004, 73.5 billion US Dollars, and 85.5 billion US Dollars by 2006. During the period of 2004-2006, the AK Party government undertook the Exports Strategic Plan, which was a roadmap for TurkeyŌĆÖs new export orientation as well as rising targets. The Plan targeted a total export volume of 75 billion US Dollars by the end of 2006, which it exceeded by more than 10 billion. Turkey ranked 22nd┬Āin terms of exports during the period of 2004-2006, compared to its previous position of 25th┬Āin 2002, according to the World Trade Organization statistics.2

Exports witnessed robust growth rates, with 25.3 percent in 2007 and 23.1 percent in 2008. Therefore, the total volume of TurkeyŌĆÖs exports reached 107.2 billion US Dollars and 132 billion US Dollars in 2007 and 2008, consecutively. The share of industrial sector exports was 115.2 billion US Dollars as of 2008. The main export destination for Turkey in 2008 remained by far the EU-27, as the exports to the EU members reached 63.4 billion US Dollars, with an increase of 4.9 percent and a share of 48 percent out of the total. Due to the global financial crisis that erupted in 2008, however, TurkeyŌĆÖs main export markets as well as the world economy as a whole were negatively affected, so the total export volume decreased by a significant 22.6 percent. The total export volume dropped down to 102.1 billion US Dollars in 2009, as shown in Figure 1 below. Nevertheless, it was still above the previously targeted 98.5 billion, envisioned by the Mid-term Economic Program (2010-2012). Exports to the EU-27 countries faced a sharp decline of 25.8 percent in 2009, dropping to 47 billion US Dollars. However, two significant developments emerged within the second half of the decade. TurkeyŌĆÖs exports to the Middle East ŌĆōespecially to the Gulf Cooperation Council (GCC) - and African countries witnessed dramatic increases. The share of African economies as a destination for TurkeyŌĆÖs exports, for instance, witnessed a strong increase of 12.3 percent, reaching 10.2 billion US Dollars in 2009, where trade volume in almost all main export destinations fell drastically.3

This analysis argues that the basic motivation behind TurkeyŌĆÖs emergence as a ŌĆśrising starŌĆÖ is foremost its economic, rather than political, cultural or religious orientation. ŌĆ£A major shift in the Turkish economy occurred in the 1980s with the adoption of neo-liberal economic policies. Despite several crises, the Turkish economy has developed to a considerable degree, making it the 16th largest in the world (in terms of total GDP by 2010). TurkeyŌĆÖs vibrant economy and the raising democratic standards (i.e. recent constitutional amendments) in the EU negotiation process have increased its soft power in the region and made it particularly attractive for reformers.ŌĆØ4┬Ā

The argument of TurkeyŌĆÖs so-called ŌĆ£axis shiftŌĆØ appears to fit TurkeyŌĆÖs changing foreign trade scheme because the number of new export destinations and the significant rise in TurkeyŌĆÖs bilateral trade volume with Latin American, African and Mid-eastern countries as well as China illustrate this new orientation. However, TurkeyŌĆÖs changing foreign trade structure also fits the new global economic trends that began in the 1990s. A simple while careful analysis of the world merchandise trade and TurkeyŌĆÖs export-import dynamics in the last decade show a considerable overlap. This is particularly true when it comes to the emergence of the East in the early 21st┬Ācentury as a new economic player and trade partner on the world scene. The exponential growth in TurkeyŌĆÖs economic figures needs to be placed in this context and qualified. The globally favorable investments, capital flows, and trade climate for emerging economies alongside TurkeyŌĆÖs politically stable domestic environment are arguably major contributing factors to TurkeyŌĆÖs robust economic performance. The increasing structural efficiencies and the low-cost margins coupled with product and market differentiation strategies are also some of the components behind the rapid expansion witnessed through bilateral and multilateral trade. Record-high amounts of foreign direct investment (FDIs) are considered as other sources of economic growth, which attained 84 billion US Dollars during the period of 2002-2009, including mergers & acquisitions as well as privatization revenues.5

With its strong economic development over the decade, Turkey has become the focus of global interests, including major events such as the IMF-World Bank Annual Meetings in October 2009, globally important energy projects like the Nabucco gas pipeline, and strategically significant issues such as the Iranian nuclear standoff. In addition, TurkeyŌĆÖs regional significance is also on the rise as it is heavily involved in mediating Mideast peace efforts, resolving Balkan disputes, and attenuating rivalries in the Caucasus region. Trade, or in more general terms, business has been one of the driving forces of increased Turkish attractiveness in its region, particularly the Middle East. TurkeyŌĆÖs prolonged desire for becoming a full EU member and its harmonization efforts with the EU┬Āacquis┬Āled to extensive political, judicial, and economic reforms in the last decade.

From the far east to the west, the baiting ŌĆśaxis shiftŌĆÖ debate hovers around TurkeyŌĆÖs political re-orientation as ŌĆ£the questions being asked are whether Ankara is turning its back on the West and drawing closer to the East. This is described as a ŌĆ£shift of axisŌĆØ and there is even talk of Turkey joining a Eurasian Union along with Russia, China and other regional countries, or finding its moorings as leader of an Islamic bloc in the Middle East and Central Asia.ŌĆØ6┬ĀThe ŌĆśaxis shiftŌĆÖ argument taken up by the traditional eliteŌĆÖs new rhetoric claims that the AK Party government has moved the country away from its prolonged axis ŌĆōwhich is by definition ŌĆśthe West.ŌĆÖ A very recent snapshot on the discussions around TurkeyŌĆÖs new orientation or axis, however, rightly describes the ŌĆśaxis shiftŌĆÖ arguments as a simple form of political blackmail that is aimed at putting down TurkeyŌĆÖs new foreign policy makers.7┬ĀThis study also shares the view that this axis shift debate is highly manipulative, as it lacks i) a proper definition of the ŌĆśaxis shiftŌĆÖ; ii) the necessary conditions for the fulfillment of a real axis shift; and iii) a definition of TurkeyŌĆÖs present axis and the counter axes along with the necessities of sustaining an axis.8┬ĀBased on these three basic deficiencies of the ongoing debate around TurkeyŌĆÖs shifting axis, the paper attempts to find evidence either ŌĆ£ForŌĆØ or ŌĆ£AgainstŌĆØ the axis shift argument on the grounds of TurkeyŌĆÖs evolving nature of foreign trade.┬Ā

┬Ā

┬Ā

ŌĆśAxis ShiftŌĆÖ Debate and the Unbearable Lightness of its Reasoning

This study asserts that the ongoing ŌĆśaxis shiftŌĆÖ debate is at the very least groundless, provided TurkeyŌĆÖs multi-dimensional and multi-layer foreign policy setup, implemented effectively during the AK PartyŌĆÖs ruling term. The axis shift debate is not neutral and possesses a hidden negative connotation, as it carries with it an accusation that Turkey intends an expansion into new regions, as ŌĆ£those who accuse Turkey of changing axis confuse the transformation of global politics with that of values and (ideological) trends. And this is where the question of axis shift is perceived as a threat and there is a ringing of alarm bells. But Turkey is simply continuing the broad trends and values begun in 1839 during the period of the Tanzimat (Reorganization) reforms,ŌĆØ9┬Āaccording to moderate observers. Whether TurkeyŌĆÖs current policies are a continuation of the Tanzimat reforms or not, TurkeyŌĆÖs new orientation both at home and overseas deserves a more profound analysis. The frontiers of limitations of an axis shift, however, are not well defined and the arguments around it are based on perceptions rather than realities. Therefore, a robust definition for the term should be introduced for each epistemological and actual domain that would legitimize the ongoing debate. Since our analysis takes TurkeyŌĆÖs foreign trade as the central perspective, however, the subsequent arguments regarding the debate will be put forward accordingly. It is certain that the ŌĆśaxis shiftŌĆÖ debate is multi-dimensional, as it has political, historical, military and security, strategic, economic, and cultural aspects. The paperŌĆÖs reading of the debate is, however, built upon the question of whether there is an axis shift on economic and specifically foreign trade grounds. Therefore, the descriptive economic data provided throughout the paper in the subsequent sections aims at providing an insight to the changing nature of the global economy as well as TurkeyŌĆÖs foreign trade orientation and (in the last section) its lack of proper strategies in the long-term. Other aspects of the debate will intentionally be left to the experts. This section will take a quick look at the rise of the Eastern economies at the dawn of the 21st┬Ācentury while analyzing TurkeyŌĆÖs position with reference to its trade relations in the last decade.

┬Ā

A Global Axis Shift: The Rise of the East

ŌĆśThe rise of the EastŌĆÖ is gradually becoming a factual rather than a perceptional phenomenon where Turkey is re-positioning itself accordingly

Global economic relations have considerably changed in favor of the Eastern countries or in more general terms the emerging market economies over the last couple decades (i.e. the 90s and 2000s). The share of developing countries ŌĆōor emerging market economies- has consistently increased both in terms of financial-capital inflows as well as trade-commodity flows. A quick look provides the necessary insight on the issue as observed in the course of world merchandise trade, based on the World Trade Organization (WTO) statistics. As Russia and China, two giants of the world commodity trade, have intensively engaged in the WTO meetings in the last decade with the latter already being a member since 2001, they still constitute a major part in worldŌĆÖs trade as well as investments. The so-called BRIC (Brazil-Russia-India and China) countries, the ASEAN+3 countries (Indonesia, Malaysia, Philippines, Thailand, Singapore, Brunei, Vietnam, Laos, Myanmar, Cambodia plus China, Japan, and South Korea), and the developing economies within the G-20 group are the rising stars of the global economy in the post-2008 financial crisis period and of the new global economic system. Despite the comparatively low levels of capital and FDI stocks or world trade shares, compared to the EU-27 and North American Free Trade Agreement (NAFTA) economies, the Eastern powers emerged as the representatives of a multi-polar global economy.10┬ĀTo provide an understanding of the great potential born by the recent giants of the world economy, ChinaŌĆÖs non-financial FDI outflows ŌĆōnot inflows- reached 48 billion US Dollars in 2009 alone, according to the UNŌĆÖs 2010 World Investment Report. ChinaŌĆÖs total outbound FDI stock is expected to hit some 500 billion US Dollars as of 2013, according to Chinese authorities.11

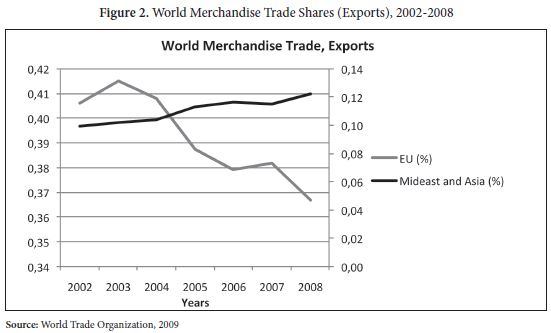

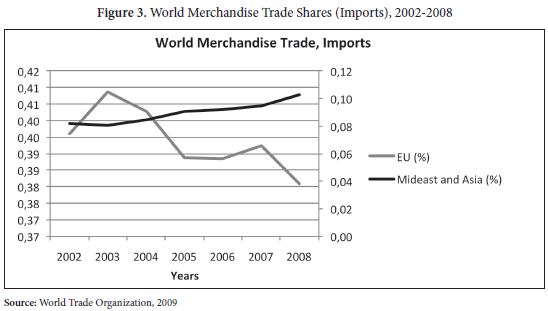

For a meaningful comparison in the case of Turkey (i.e. the axis shift debate), the above and below figures (Figure 2 and Figure 3) provide a depiction of the evolving shares of the EU-27 countries (including intra-EU trade) and the Asian economies, including Middle Eastern countries. Accordingly, the total share of the EU-27 block in world merchandise trade is steadily declining over the period of 2002-2008, from 41 percent down to 37 percent in exports and from 40 percent down to 38 percent in imports. Meanwhile, the share of Asian exports witnessed an increase from 10 percent up to 12 percent while imports were up from 8 percent to 10 percent.12┬ĀTherefore, if the term is applicable, it is quite evident that a slow but gradual ŌĆśaxis shiftŌĆÖ towards the East is in place on a global scale.

It should be no surprise to see the declining trend continue in the total trade share of the EU countries coupled with the rising share of Asian economies as of today, particularly given the financial crisis of 2008. Capital flows to the US and the EU markets have significantly slowed down while the inter-trade volume among the developed nations (i.e. the G-7 members) was hit considerably over the last couple years. In addition, global FDI figures imply that the developed economies, such as the US and the UK, were severely affected by the crisis as total FDIs declined by 68 percent and 85 percent, respectively in 2009. Overall drop in the FDI flows to the 20 developed nations reached 54 percent while the 34 emerging market economies suffered from a 40 percent decline in the FDI flows in 2009, due to the crisis. The aforementioned 54 countries account for more than 90 percent of the worldŌĆÖs total FDI flows ŌĆōwhich witnessed some 49 percent decrease in 2009.13┬ĀRecent data that provides a projection for the mid-term also suggests that China is expected to surpass all G-7 members, except the US as of 2015, in terms of its economic size.14┬ĀThe IMFŌĆÖs World Economic Outlook (WEO) 2010 report also suggests that the Emerging and Developing EconomiesŌĆÖ stake in world trade has increased from a total volume of 3.2 trillion US Dollars (approx.) up to around 11.8 trillion US Dollars in 2010. During the same period, however, IMF data suggests that the total trade volume of advanced economies witnessed an increase from 9.5 trillion US Dollars in 2002 up to 18.2 trillion US Dollars in 2010.15

All in all, ŌĆśthe rise of the EastŌĆÖ is gradually becoming a factual rather than a perceptional phenomenon where Turkey is re-positioning itself accordingly. The emerging and developing economies mostly located in the East are also increasingly the financers of world economic growth. The IMF data projects the total debt stock in the US to attain 110.7 percent of the total GDP while it is expected to be 89.3 percent for the Euro zone in 2015. The same data indicates expected current account deficits of advanced economies to reach around 274.4 billion US Dollars in 2015 while emerging and developing economies are expected to run a surplus of 763.8 billion US Dollars in 2015.16

Other indicators such as savings and investment numbers are also providing a strong indication of emerging economiesŌĆÖ increasing role in the global economy. Net FDI and portfolio investment flows are also suggestive of the developing economiesŌĆÖ robust performance regarding their attractiveness for global capital movements. According to the most recent estimates, savings rate (as portion of the total GDP) for the emerging economies will be reach 33.8 percent, during the period of 2012-2015, while the investment ratio will hit 32 percent in the same period. Meantime the savings and investment ratios will stand at 19.7 percent and 20.1 percent, respectively.17

┬Ā

┬ĀTurkeyŌĆÖs Eastward Shifting Axis: Integration or Penetration?

For more than half a century, TurkeyŌĆÖs traditional trading markets include the EU, Russia, the US, and parts of the Middle East. The EU has the highest share due to its market size in terms of geography, population (i.e. demand) as well as its GDP. Increased involvement in bilateral trade with the European Union (EU) economies implies that TurkeyŌĆÖs export sector needs to maintain its competitiveness while being regionally oriented westward. Trade between Europe and Turkey has blossomed, especially after TurkeyŌĆÖs accession to the EU Customs Union at the end of 1995. Total trade volume hit 81 billion Euros (104 billion US Dollars) in 2009. However, the Customs Union agreement was signed without concluding a free trade agreement. Therefore, Turkey still suffers certain losses due to the lack of a Free Trade Agreement (FTA) or because it is not a full member of the EU.

This has led Turks to increasingly question the current status of EU-Turkey trade, despite the free trade of certain goods and preferential access to the EU markets, since ŌĆ£this relationship remains overly complex and discriminatory toward Turkey in two respects. First, as a precondition of joining the customs union (CU), Turkey was required to adopt the EUŌĆÖs existing FTAs with partner countries, including the European Free Trade Area. However, arrangements between the EU and third countries since 1995 automatically extend to Turkey, even though Ankara is excluded from the decision-making process. Second, Turkish markets are automatically opened to these third countries under the customs union agreement, but Turkey is not automatically granted reciprocity by the third country. Reciprocity depends on BrusselsŌĆÖ goodwill and willingness to include a ŌĆśTurkish clauseŌĆÖ in their final agreement. This arrangement is unsatisfactory. Turkish commercial policy has essentially been seconded to Brussels without any gain in voting rights. Trading away its sovereignty might be a price worth paying if EU membership was assured, but membership is not assured. Therefore, the EU should adopt a full and comprehensive FTA with Turkey to replace the customs union agreement.ŌĆØ┬Ā18

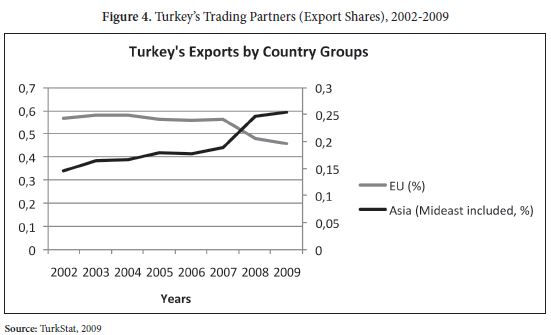

The share of EU markets in terms of Turkish exports declined significantly from┬Ā56 percent in 2002, down to 46 percent in 2009 while AsiaŌĆÖs share increased from 14 percent up to 25 percent during that period

A new wave of free trade agreements with neighboring countries is expected to take place, as stated in the EUŌĆÖs 2007 Market Access Strategy. Under such terms, Turkey expects to be included in an expanded FTA scheme, such as the Euro-Mediterranean Free Trade Area (EMFTA), as a current member of the Union for the Mediterranean. Sectors previously excluded from the EUŌĆōTurkish Customs Union, including agriculture should therefore be included under such an FTA. Although the US is relatively a staunch supporter of TurkeyŌĆÖs EU bid to become a full member, the US still gains from TurkeyŌĆÖs advanced ties with the EU as a recent analysis puts it: ŌĆ£A bold and comprehensive FTA with Turkey could set a precedent for achieving greater volumes of trade than the EU Customs Union and would create an enduring basis for EUŌĆōTurkish integration separate from the highly politicized question of EU membership. Establishing an FTA with Turkey in place of the customs union should not remove the prospect of EU membership for Turkey. Nor should the EU withdraw its financial aid to Turkey as designated under the Instrument for Pre-Accession Assistance. However, if Turkey is ultimately denied EU membership, Ankara will still be in a position to benefit from an enduring trading relationship with the EU and its Mediterranean partners. If TurkeyŌĆÖs accession to the EU remains as unlikely as it appears today, Europe needs a fallback position to ensure that Turkey still has a reason to maintain good relations.ŌĆØ19

TurkeyŌĆÖs trade with the EU-27 block has been consistently subject to limited declines over the period of 2002-2009 in terms of its share in total, as observed in the figures above and below. This phenomenon is partly due to the above-mentioned problems over the customs union agreement and TurkeyŌĆÖs prolonged quest for joining the ŌĆśclubŌĆÖ as a full-member while the EUŌĆÖs most weighty members, like Germany and France, are still resistant to TurkeyŌĆÖs inclusion. It is crystal clear that the customs union in practice for instance has not yielded a long-run ŌĆśtrade creationŌĆÖ in terms of percentage change but rather a ŌĆśtrade diversionŌĆÖ on behalf of Turkey.20┬ĀThe recent comparative shift in TurkeyŌĆÖs trade with its neighboring countries and ŌĆśclubsŌĆÖ has also to do with the globally rising performance of the East, as stated in the previous sub-section. In addition, ŌĆ£the share of the EU-27 group in the Turkish exports declined from 48 percent down to 46 percent between 2008 and 2009, which is considered as a setback in TurkeyŌĆÖs traditional trade markets and an indicator of both a shift of axis in the EU markets and Turkish exports, by some circles. Accordingly, a recent global shift away from the EU-27 block to the rest of the world is taking place in terms of multi-national firm operations, investments and capital and commodity flows during the crisis period of 2008-2009.ŌĆØ21┬ĀTurkey however missed the opportunity of both increasing its exports to the EU members in a period of declining intra-EU trade figures while taking advantage of outbound capital and commodity flows as it attracted significant amounts of FDIs and boosted its trade volume over the last decade.

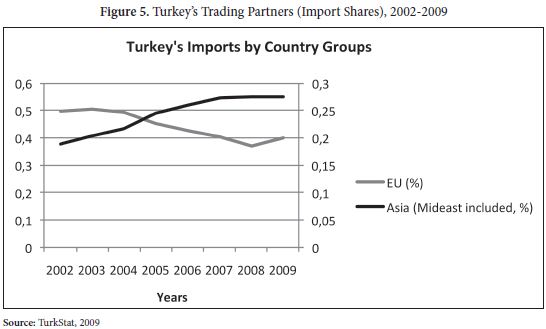

According to the relevant figures above and below (Figure 4 and Figure 5), TurkeyŌĆÖs trade with the Asian economies, including the Mideast countries, is constantly rising while there is a gradual decline observed in the trade with EU-27 during the period of 2002-2009, despite the slight correction for the imports from the EU in 2009. The share of EU markets in terms of Turkish exports declined significantly from 56 percent in 2002, down to 46 percent in 2009 while AsiaŌĆÖs share increased from 14 percent up to 25 percent during that period. For the imports, EUŌĆÖs share declined from roughly 50 percent down to 40 percent over the period of 2002-2009 while the share of Asian countries surged from around 19 percent in 2002 up to 27 percent in 2009.

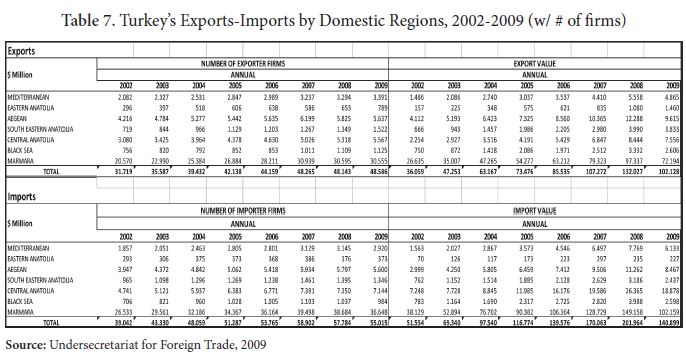

Another significant development in Turkish trade is observed in the relative changes in the shares of TurkeyŌĆÖs domestic regions in the context of its total trade volume. TurkeyŌĆÖs South-Eastern Anatolian and Mediterranean regions as well as the Eastern Anatolian region gained comparative advantages in the period of 2002-2009 where a significant overall increase was witnessed (see Table 7). Cross-border trade also made a substantial contribution to the recent increase in trade activities in the Southeastern provinces, thanks to the visa-free travel regimes and reduced bureaucracy since 2002. TurkeyŌĆÖs recently improving ties with Middle Eastern and North African countries as well as Russia and other Eastern economies are in part due to the overall development in the Turkish trade sectorŌĆÖs performance and also in part due to the EU-Turkey political issues (including the visa disputes). Therefore, it is still too early to speak about an axis shift, as the EU-27 block will remain the main trading partner for Turkey for the foreseeable future, even if its full-membership bid fails to produce the successful outcome Turkey has been working towards achieving in the next decade.

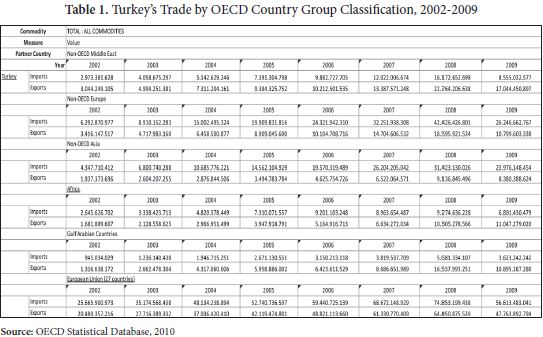

Turkey has successfully managed to increase its total trade volume as well as the diversity of its destinations in the period of 2002-2009 while the main axis of its foreign trade partners remained unchanged. The figures from OECD ŌĆōprovided in the Table 1 below- imply that Turkish trade has witnessed a significant decline almost in all fronts, except the group of African countries, during the recent global financial downturn. However, during the whole period of 2002-2009, the weight of the EU-27 countries has seen a relative decline while the rest of the world accounts for an increasing share of TurkeyŌĆÖs total trade in terms of percentages. That alone does not indicate a shift of axis but rather the effective utilization of potential markets, i.e. in Africa.

The above table provides insight on TurkeyŌĆÖs commodity trade, which clearly indicates a decline both in Middle Eastern and European trade volumes during the recent crisis period (2008-2009) while during times of the world trade booms (2002-2007) there was an increase. Significant determinants of an ŌĆśaxis shiftŌĆÖ should have also revealed themselves in terms of services and labor flows. Although the latter is still far from being accomplished in todayŌĆÖs world, the first is increasingly developing, particularly with the EU. As underlined in the previous sections, TurkeyŌĆÖs service industry has strong ties with its European counterparts, in telecommunications, tourism, and finance. Therefore, bilateral trade in services which reached 46.5 billion US Dollars in 2008, mostly with the EU members is yet another indicator of a broadening axis, rather than an ŌĆśaxis shift.ŌĆÖ22

┬Ā

┬Ā

Trade Booms and Busts: Signs of an ŌĆśAxis ShiftŌĆÖ?

Turkey has witnessed periods of trade booms and busts for decades. However, all are associated with periods of political stability or instability which had their corollary economic repercussions. In this section, the theoretical foundation of TurkeyŌĆÖs so-called axis shift from a trade perspective is questioned. Empirical evidence and recent data are employed in the analysis when necessary. Relevant links between the recent political orientation and its economic consequences will also be reflected under the following sub-sections. The increasing influence of TurkeyŌĆÖs new diplomatic assertion in its region is argued to be coupled with deepening economic ties manifesting itself in the number of free trade agreements, visa-free travel agreements, and even in new flight routes between Turkey and its partners. TurkeyŌĆÖs increasing relations with its neighbors will be analyzed first through the ŌĆśgravity equationŌĆÖ tool in the new trade theory which focuses on the geographic as well as cultural proximity of countries engaging in bilateral trade. The second sub-section will underline the important transition of the political and diplomatic dimensions into the economic dimension. Finally, last sub-section will discuss the lack of a long-term economic strategy to maximize TurkeyŌĆÖs foreign trade potential with its neighbors as well as its other trading partners.

┬Ā

TurkeyŌĆÖs FTAs and the New Gravity Equation

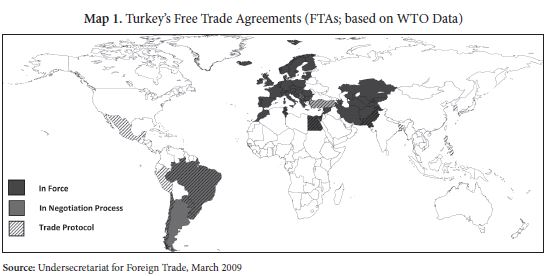

Gravity (equation) models are considerably new to the theory of international trade though they have been in use for more than a decade now. In general, new trade theory takes economic size, geography or rather proximity, culture, common language or borders and other such issues into account in order to estimate the role of trade in cross-country growth forecasts. In the case of Turkey, the FTAs created more than the customs union with the EU, as they are increasingly effective in diversifying and magnifying Turkish exports. The table below and the map provide an insight into TurkeyŌĆÖs new trade dimensions, taking the common elements in bilateral relations into account.

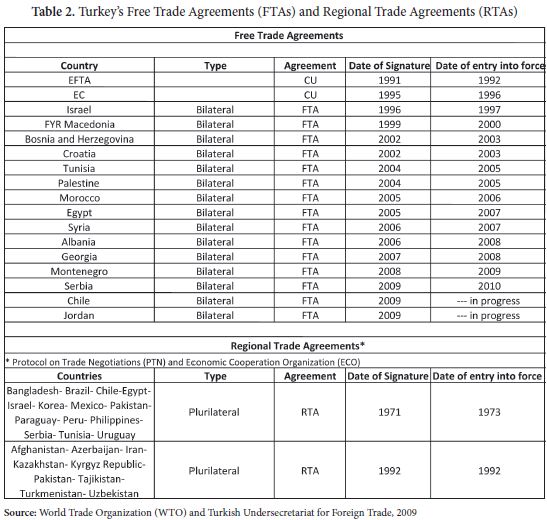

TurkeyŌĆÖs new trading partners are not only in the Greater Middle East but also in Latin America, Asia and North America as well as Africa as shown in the above Map 1. It depicts the countries that Turkey has engaged with in terms of FTAs. Although common language (as seen in bilateral relations with Central Asian and Caucasian countries), cultural heritage and ties (observed in Middle Eastern, Caucasian, and Balkan regions), and shared borders (in all cases) are important elements of the rapprochement to the aforementioned regions, Turkey has managed to establish a widespread network of bilateral trade relations even with very distant (both geographically and culturally) countries via governmental and private initiatives since 2002. The history of the preferential trade agreements signed by Turkey, however, dates back to before the first FTA was established with the European Free Trade Association (EFTA) ŌĆōrepresented by Austria, Finland, Switzerland, Iceland, Liechtenstein, Norway, and Sweden in 1992. Since then, Turkey has realized more than a dozen of FTAs (excluding the customs union agreements) with varying countries as indicated in Table 2 below.

While establishing FTAs and RTAs throughout different regions in the world, Turkey has managed to establish visa-free travel regimes at all levels with more than a dozen countries within the last decade. Countries that Turkey signed mutual visa-free travel agreements on different levels or visa holder-status include: Tajikistan (2003 and 2009); Uzbekistan (2003); Romania (2004); Guatemala (2004); Venezuela (2005); Paraguay (2006); Colombia (2006); Latvia (2006); Vietnam (2007); Kuwait (2007); Afghanistan (2007); Montenegro (2008); India (2008); UAE (2008); Kosovo (2009); Djibouti (2009); Syria (2009); Pakistan (2009); Albania (2009); Kenya (2009); Qatar (2009); Libya (2009); Jordan (2009); Azerbaijan (2009); Lebanon (2010); Tanzania (2010); Cameroon (2010); Russia (2010); Serbia (2010); Portugal (2010); and Greece (2010).23┬ĀOne could assess the reach and diversity of TurkeyŌĆÖs new foreign policy and thus trade relations via established free trade agreements, new flight routes, and visa agreements which indicate a multi-polar geographic orientation rather than a clear-cut axis shift. In addition, the Turkish Undersecretariat for Foreign Trade documents reveal that the government is in negotiations to finalize the establishment of FTAs with Lebanon, the GCC countries, Ukraine, MERCOSUR countries, Libya, Mauritius, Seychelles, and Faroe Islands while initiating talks with Mexico, Algeria, South African Customs Union, ASEAN, South Africa, ANDEAN, India and 36 countries under Africa Caribbean Pacific Group of States (ACP).24┬ĀTherefore, the relatively unexploited nature of TurkeyŌĆÖs bilateral trade with the aforementioned countries or groups offers a unique opportunity to rapidly develop further economic and commercial ties. This list of countries, on its own, is irrefutable evidence that the argument for an axis shift is weak and it has much more to do with providing some insight into TurkeyŌĆÖs future vision of diversifying its trade destinations.┬Ā

The role of ŌĆśgravity equationŌĆÖ becomes crucial when the location, size, and diversity of the newly established FTAs or other forms of bilateral trade relations are taken into account. Recent studies on the impact of trade on cross-country income growth rates have been investigating alternative instruments for trade. For instance, a pioneering work in the trade-growth literature provides geographical instruments for countriesŌĆÖ overall trade based on the standard gravity equation.25┬ĀThe distance between countries that have bilateral trade and the country sizes are used as instruments which are seemingly unrelated to any other factor affecting their income levels, respectively. While using one of the instruments, however, one should control the other since they are negatively correlated. Constructing an instrumental variable for trade and estimating the effects on income suggest that the trade share may not have a positive significant effect on income growth while in some cases trade variables have insignificant positive or again insignificant negative coefficients. In general, however, using geographical variables as instruments for both bilateral and international trade alone could be said to eliminate statistically relevant problems issues but it does not always provide satisfactory results in explaining the effects of trade on income.

┬Ā

┬ĀThe Role of Politics on TurkeyŌĆÖs Trade Policy

At the dawn of 21st┬Ācentury, Turkey has become increasingly a global actor while still revealing that its capacities are mostly regional and it possesses internal weaknesses. Nevertheless, many argue, more powerful than a decade ago, Turkey has emerged as a key member in international organizations, including the United Nations Security Council, Organization of the Islamic Conference (OIC), the OECD, even in the International Monetary Fund (IMF), and the World Bank. The latter two, however, should be read under the context of the increasing influence of emerging market economies altogether. Along with the increasing weight in the IMF and the World Bank Group, TurkeyŌĆÖs G-20 membership (1999) also becomes more critical and operational nowadays, thanks to the gradually evolving nature of the global economy and governance since 2008.26

Regarding TurkeyŌĆÖs relations with and its position in the Middle East particularly, Foreign Minister Ahmet Davutoglu underlined the importance of paying attention to the region at least in terms of its potential strategic assets while showing efforts to put the pieces together in the ŌĆśgeo-economically torn apartŌĆÖ Mid-eastern countries.27┬ĀOn economic ties with the European Union (EU), TurkeyŌĆÖs foreign policy chief stresses that due to the uncertainties regarding the future track of TurkeyŌĆÖs EU membership processes, the country should formulate a new development strategy based not only on its domestic potential but also to support the potential opportunities originating from its geographic location.28┬ĀIn an assessment of the foreign policy developments of 2007, Davutoglu asserted that TurkeyŌĆÖs diverse regional composition or unique central position gives her a capacity to maneuver in several regions simultaneously, which in turn creates an area of influence in its immediate environs.29┬ĀThe five pillars of TurkeyŌĆÖs new foreign policy vision have been delineated as follows: i) balance between security and democracy; ii) ŌĆśzero problem policy toward TurkeyŌĆÖs neighborsŌĆÖ; iii) development of relations with neighboring and distant regions; iv) adherence to a multi-dimensional foreign policy; and v) rhythmic diplomacy. Within the framework of these five pillars, Davutoglu refers to the role of individuals, corporations, and civil organizations as complementary in the pursuit of TurkeyŌĆÖs foreign policy.30┬ĀDiplomatic efforts for increasing regional political and economic stability included mediation in the indirect peace talks between Israel and Syria, diplomatic engagement in Iraqi politics, and the mediation of nuclear talks between Iran and the P5+1 countries (five permanent members of the UN Security Council, EU and Germany) together with Brazil. TurkeyŌĆÖs pursuit for stability on the domestic, regional, and global fronts is accompanied by its increasing economic presence in its own region and the world.

Turkey is asserting its new geo-strategic position through a series of policies and instruments within the theoretical cadre of strategic engagement accompanied by practical and often tactical moves to enhance regional and bilateral diplomatic and economic relations. An emerging business group, TUSKON, which is largely comprised of exporters, has been actively engaged in African and East Asian markets while another business group, the Independent Industrialists and BusinessmenŌĆÖs Association (MUSIAD) is in search for increased cooperation with the Gulf countries. In the meantime, TurkeyŌĆÖs oldest business group, the Turkish Industrialists and BusinessmenŌĆÖs Association (TUSIAD), continues to actively lobby for the eventual EU membership of the country. Given such a diversified composition of efforts to promote TurkeyŌĆÖs global position, one should also note the dramatic rise in the number of direct or indirect flight routes of the national flagship carrier, Turkish Airlines (THY), since 2002. Between 2002 and 2010, the distribution of the newly opened routes is also informative, as 14 out of the total 58 new routes are to European cities, while 18 routes are to Asia. THY meantime has opened 14 flight routes to the Middle Eastern and North African cities, along with eight new routes in Africa.31┬ĀBusinessmen are now easily traveling and conducting business with their counterparts via direct flights to the capitals of Africa, Asia, and Europe.┬Ā

TurkeyŌĆÖs increased economic influence in its region manifested itself in the volume of trade with neighboring countries, as observed in Turkish-Iranian bilateral trade figures (up from 1.2 billion US Dollars in 2002 to around 5.4 billion US Dollars in 2009); Turkish-Russian bilateral trade figures (up from 5.1 billion US Dollars in 2002 to 22.7 billion US Dollars in 2009) and Turkish-Syrian bilateral trade figures (up from 773 million US Dollars in 2002 to 1.8 billion US Dollars in 2009), despite the negative effects of the recent global financial crisis.32┬ĀSimilarly, the total trade volume with the Latin American and Caribbean countries rose from 735 million US Dollars in 2002 to more than 4 billion US Dollars as of 2008. As the study aimed to demonstrate, all of the figures illustrated are practical indicators reflecting TurkeyŌĆÖs changing foreign policy structure from an international trade perspective.

Economists often argue that political outcomes or the type of the state can effectively create an ŌĆśefficientŌĆÖ trade policy scheme. The interplay of economic/commercial actors in a country or at the global level has a significant result on potential trade games and even trade wars.33┬ĀThe relationship between trade and growth and their impact on income distribution within and across countries has been intensively discussed in a vast body of literature. The relative changes in the income levels among different business groups or industrial segments in Turkey also result from the interplay between politics and trade policies.

In shaping a countryŌĆÖs trade policy, the size of its domestic market, the variety of its products (i.e. amount of capital or intermediate goods), and geographic proximity are among several important elements. Trade laws and the efficiency in doing business are other components to impede or speed up the countryŌĆÖs trade performance. As politics are important in shaping trade policies, the latter is also effective on income creation and redistribution mechanisms.34┬ĀTrade policies are usually correlated with other factors related to income (growth), for instance, the adoption of free market trade policies as is the case with Turkey in the 1980s, as in other developing countries, brought about subsequent policy measures such as financial liberalization. The aim of this paper is, however, to isolate the rest of the factors other than trade that would explain TurkeyŌĆÖs current economic policies. Therefore, the recent developments on the political scene and its reflections on trade policy will be at the focus of this analysis. Since the early ŌĆÖ90s, the emerging business groups can be described as the economic face of TurkeyŌĆÖs changing political environment. Despite the continuing role of TUSIAD in the political sphere, MUSIAD and export unions such as the Turkish ExportersŌĆÖ Assembly (TIM) or formations like TUSKON in recent years are increasingly effective in shaping the countryŌĆÖs trade policies. Traditional conglomerates mostly represented under TUSIAD are mostly clustered in automotive, chemicals and metals, construction and energy, finance and pharmaceutical industries while relatively smaller size firms ŌĆōmostly represented in MUSIAD- operate in textiles, retail, consumer electronics and food sectors.┬Ā

TurkeyŌĆÖs emerging trade destinations provide a relative advantage for the smaller size entrepreneurs due to their firm size while yielding significant amounts of positive externalities for the conglomerates in their increased bilateral economic ties as well. TurkeyŌĆÖs new trade orientation or re-balancing act has been, therefore, beneficial to all parties at the domestic level while providing cyclical results ŌĆōbeside Africa- at the international level. The latter argument is evident in TurkeyŌĆÖs significant losses in European, North American, Asian and Middle Eastern ŌĆōincluding Gulf countries- bilateral trade volumes (see Table 5 and Table 6).

Despite the increasing trade volume with its neighbors in recent years, Turkey has not adopted a well-structured long-term export strategy though its new pro-active foreign policy aims at creating regional economic zones. An ad hoc rather than a systematic approach is embraced in trade policy while the role of aforementioned business groups earns increasing weight. The inter-governmental relations pave the way for exporter to reach new markets while a comprehensive trade strategy is still far from being implemented. Turkish exporters are still highly dependent on state policies and the possible agency problems might hinder further economic development as bureaucratic and administrative quality are key to success in such a framework. Despite the recent rise in TurkeyŌĆÖs trade performance, we may conclude, it is too early to suggest an ŌĆśaxis shiftŌĆÖ in the modes of production and the relative roles of small and middle sized entrepreneurships (SMEs) versus conglomerates. TUSIAD in that sense continues to be the leading club both in terms of its total trade volume and the value-added.

┬Ā

Prospects for Turkish Trade in a Changing Global Economy

Due to the structural comparative advantage and the countryŌĆÖs increasing competitiveness, Turkey is expected to remain as one of the foremost trading partners for the EU countries. It is quite natural for a pivotal state like Turkey to develop new ties with the global economiesŌĆÖ rising stars and its neighboring countries due to several reasons: increasing economic power (GDPs etc.),┬Ā

dynamic population (driving the demand), and common ties (i.e. geography, history, religion and culture). Therefore, an axis shift debate becomes obsolete when studying the facts and once the negative and skeptical perceptions over TurkeyŌĆÖs new foreign (trade) policy are removed. Such a debate reveals the remnants of the old compartmentalizing mentality of the Cold War in the minds of TurkeyŌĆÖs Western allies.

TurkeyŌĆÖs recent rise, based on its rapid economic growth, is reinforced by its strong ties to the EU, as it obligates Turkish exporters to function with a high level of standards

The traditional Western perception of the ŌĆśEastŌĆÖ once again seems to have emerged in the recent ŌĆśaxis shiftŌĆÖ debates without any solid basis. In the wake of changing global economic setup with the rise of G-20 specifically, it would be quite normal to see Turkey becoming a regional player as well as an actor in the newly shaping global economic structure. Based on the trend over the last decade, we could argue that Turkey continues to promote new development in terms of its foreign trade. This trend could continue for the foreseeable future given the political stability within the country combined with favorable global economic conditions, particularly for the developing economies. The significant dependence over the import of intermediate goods and the lack of a proper R&D strategy, however, are among the factors which hinder a more rapid economic growth in the country. In the meantime, Turkey needs to develop a long-term trade policy strategy plan to address the current weaknesses in its production, marketing, and other segments of its trade structure.

The differences in the rate of economic growth are often observed to depend on the relative sizes of the countries under the endogenous growth models ŌĆōwhich imply that positive gains or increasing returns of scale are possible provided that endogenous factors are driving the rate of growth among countries. Therefore, increasing the size of a country leads to expanding the variety in intermediate goods and results in efficiency gains in production of the final goods. This increased diversity in exported goods is found to have a positive effect on trade volumes and thus growth rates, as shown in numerous empirical works. Another implication is the decreasing fixed costs of innovative new intermediate inputs. This is the cause of a permanent increase in the output due to a larger country size. Therefore, we may conclude that TurkeyŌĆÖs trade with its neighbors and other short-distance partners will yield relatively bigger gains for itself. However, it is all directly linked to a comprehensive industrial and commercial policy design, which will provide substantial productivity increases in the long-run. The size or scale effect and productivity increase would not have the same impact in cases where policies do not matter. It is, however, crucial for Turkey to maintain a robust and continuous productivity increase that would guarantee competitiveness.

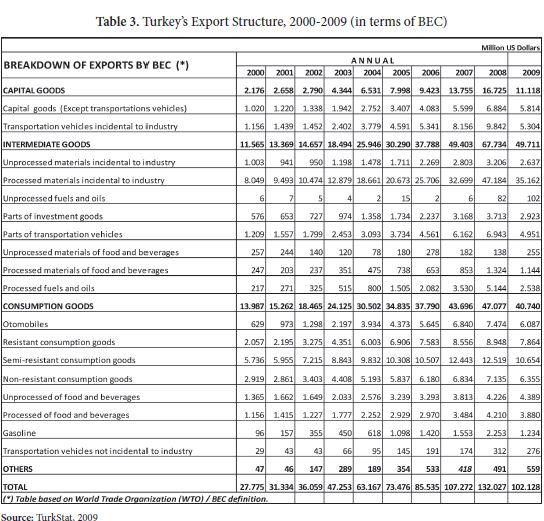

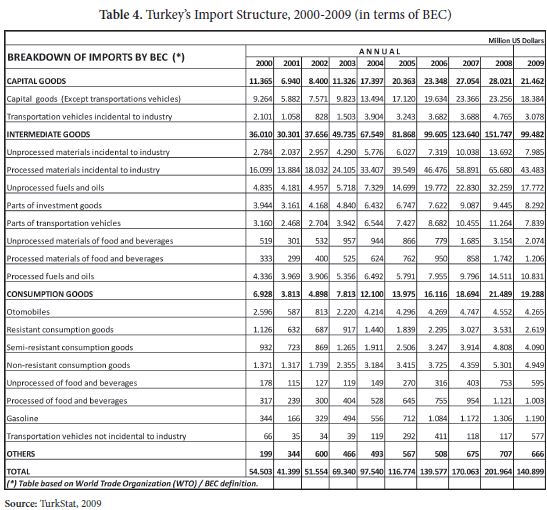

The endogenous growth models referred above also imply that with knowledge spillovers, trade increases the growth rates. In that sense, TurkeyŌĆÖs trade with a wider set of countries will benefit all parties in many aspects. Table 3 and Table 4 provide a clear understanding of the lack of a sustainable export-oriented growth strategy as the export and import shares of intermediate goods ŌĆōwhich are crucial for final production-, are hardly correlated. In 2009 only, the amount of intermediate goods imported (99.5 billion US Dollars) is almost as much as TurkeyŌĆÖs total exports (102.1 billion US Dollars). Another way to look at TurkeyŌĆÖs performance in terms of a structural breakthrough is to assess the technology component or share in export goods. In both terms, Turkey is far from producing value-added items that would increase efficiency as well as overall economic infrastructure.

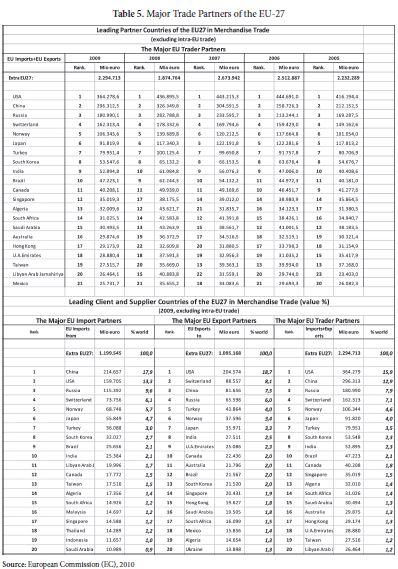

TurkeyŌĆÖs recent rise, based on its rapid economic growth, is reinforced by its strong ties to the EU, as it obligates Turkish exporters to function with a high level of standards. Positioned at the top of the quality ladder, the EU markets drive the export sector to become more competitive by increasing the quality of commodities and services while maintaining competitive price levels. With its unique geographic advantage, supported by a dynamic population and a significantly large market size as well as improving human and physical capital stock, Turkey is also becoming an indispensable partner of European trade. As depicted in Table 5, TurkeyŌĆÖs position among EU-27ŌĆÖs trade partners is almost unchanged over the period of 2005-2009, as it ranks 7th┬Āin the whole five-year period, which could be read as another rejection of the axis shift arguments.

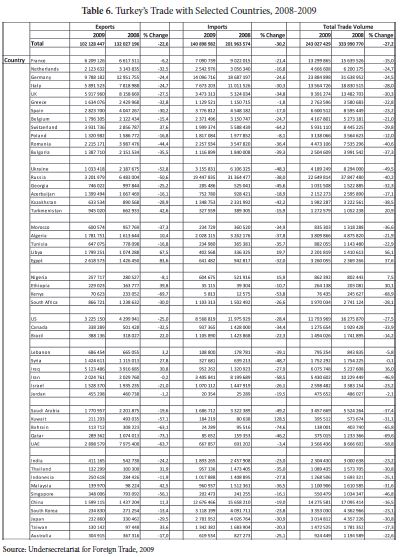

TurkeyŌĆÖs trade is dominated by the traditionally advantageous export industries, such as textiles, machinery, chemicals, plastics, metals and automotive subsidiaries. This is true not only for trade with the EU-member countries but also the newly engaged markets. However, for Turkey to ensure a sustainable future for its exports - it is crucial that it make a significant shift towards high-technology intensive products. As observed in Table 3, 4 and 5, the structural breakthrough for the export sector is vital for a sustainable path to maintain long-run growth. The export sector should strive to reach a significant level of quality and creativity in terms of marketing power as well as productive and innovative capabilities in order to meet its full potential. The recent global financial turmoil can be used as an experimental case for our study since it revealed the structural weaknesses of TurkeyŌĆÖs export sector and its high level of dependency to imported goods. During the period of 2008-2009, TurkeyŌĆÖs trade with its traditional partners such as EU-27, North America, Russia, China, and the Middle East as well as many other markets shrank dramatically, as observed in Table 6. The only exception to this general rule came from certain North African and Central Asian markets.

TurkeyŌĆÖs recent initiatives and relative orientation towards the East does not only stem from its own policy choices but also reflects an indispensible necessity due to the evolving nature of the world political and economic makeup

TurkeyŌĆÖs export sector should, therefore, learn how to advance in terms of technological capacities as well as marketing power. Turkey is not the dominant power or the leader as an exporter in the new markets it has extended its arms across the globe. Therefore, Turkey needs a comprehensive strategy that takes geographical, cultural and social as well as technological and economic (i.e. efficiency) aspects into account, which will pave the way to succeed in the long-term. TurkeyŌĆÖs recent foreign policy orientation towards its region and the world could facilitate the creation of positive externalities. However, TurkeyŌĆÖs failure to design a profound economic strategy might lead to an alignment of interests of the policy-makers and the business circles in the short-run. The rent-seeking business groups that aim to maximize profits and the current export-oriented regime fostered by the government will run counter to the need for generating the necessary technological and innovative infrastructure the Turkish economy requires to position itself on the world trade stage as a permanent and powerful actor. Unfortunately, this has already manifested itself by TurkeyŌĆÖs low level of investment in technology and registered patents. The lack of value-added in most of the sectors also leads to a higher current account deficit, which is an additional constraint to TurkeyŌĆÖs path towards long-term sustainable growth.

TurkeyŌĆÖs new trade destinations and relations have helped to alleviate the negative impact of the global financial crisis┬Āof 2008

┬Ā

┬Ā

Conclusion

Turkey is emerging as a pivotal state with its vibrant economy and increasingly stable domestic political scene in the first decade of the 21st┬Ācentury. The present paper provides an insightful while critical understanding of the evolving nature of the debates hovering over TurkeyŌĆÖs new foreign policy structure through TurkeyŌĆÖs perspective of foreign trade from 2002 to 2010. A detailed and careful analysis reveals that the so-called ŌĆśaxis shiftŌĆÖ debate becomes obsolete once factual economic indicators are demonstrated and analyzed. From the number of flights overseas to the mutual visa-exemption agreements, and the establishment of cross-border commercial ties; all are indicators of TurkeyŌĆÖs changing trade environment.┬Ā

TurkeyŌĆÖs recent initiatives and relative orientation towards the East does not only stem from its own policy choices but also reflects an indispensible necessity due to the evolving nature of the world political and economic makeup. Therefore, this analysis puts forward the argument that Turkey does not fit into an ŌĆśaxis shiftŌĆÖ debate. The term that would best coin the recent developments might be an ŌĆśexpansionary axisŌĆÖ or a new ŌĆścreative axisŌĆÖ. The ongoing trend in TurkeyŌĆÖs recent foreign policy and, therefore, foreign trade rapprochement with the East in broad terms, seems to have entered into a new phase that could be irreversible. However, the current global trends would need to prevail in the medium and long-term.

Nonetheless, TurkeyŌĆÖs new trade destinations and relations have helped to alleviate the negative impact of the global financial crisis of 2008. Although TurkeyŌĆÖs GDP shrank by 4.7 percent and its total trade volume significantly dropped by around 27 percent on annual basis,35┬ĀTurkey has managed to avoid a long-term recession as its economy is expected to grow at a rate of above 7 percent in 201036┬Āand the total trade volume is estimated to dramatically recover. However, the negative counterpart is TurkeyŌĆÖs widening current account deficit, of which its trade deficit is a major factor. As TurkeyŌĆÖs trade volume increases, so does its deficit, due to structural issues as stated in the previous sections. Therefore, a sustainable trade scheme should incorporate a solution to remedy the structural deficit problem, which stems from the mode of production and low levels of technology, thus Turkey produces products with a weak value-added.

Since the current trade deficit is unsustainable in the long-run, TurkeyŌĆÖs recently discovered trade relations, which usually yield trade surpluses are of crucial importance to achieve a balanced path to foreign trade. Such a structural break would only have long-term positive contribution to the aggregate economy. As long as TurkeyŌĆÖs engagement with the European markets on economic grounds and the EU on the political continues, the current level of bilateral trade with the EU-27 club will get closer to reaching its full potential, as it contributes greatly to TurkeyŌĆÖs economic growth. The relatively less-utilized markets, however, provide a broad set of opportunities in terms of its ŌĆśvalue-addedŌĆÖ in foreign trade. Given the lack of a proper structure for its trade with the EU and the current imbalances in bilateral trade with countries such as China, TurkeyŌĆÖs elusive quest for new trade partners and regions is indispensable.

┬Ā

┬Ā

Appendix

┬Ā

┬Ā

Endnotes

- Halil Inalcik, ŌĆ£Capital Formation in the Ottoman Empire,ŌĆØ┬ĀThe Journal of Economic History, Vol. 29, No. 1 (1969), p. 102, cited in Fernand Braudel,┬ĀCivilization and Capitalism 15th-18th┬ĀCentury, Vol.2 The Wheels of Commerce┬Ā(London: Phoenix Press, 2002), p. 558.

- Cited in ŌĆ£TurkeyŌĆÖs Export Development,ŌĆØ Undersecretariat for Foreign Trade Report, 2009.

- Undersecretariat for Foreign Trade, 2009 Annual Foreign Trade Report.

- Meliha Benli Altun─▒┼¤─▒k, ŌĆ£Turkey: Arab Perspectives,ŌĆØ TESEV Foreign Policy Analysis Series 11 (May, 2010), p. 9, retrieved from http://www.tesev.org.tr/UD_OBJS/PDF/DPT/OD/YYN/ArabPerspectivesRapWeb.pdf.

- UNCTAD and Central Bank of the Republic of Turkey, 2010.

- Rahimullah Yusufzai, ŌĆ£A ŌĆśshift of axisŌĆÖ by Turkey?ŌĆØ┬ĀThe News International, Peshawar, June 22, 2010, retrieved from http://www.pkcolumns.com/2010/06/22/a-shift-of-axis-by-turkey-by-rahimullah-yusufzai/.

- Nuh Y─▒lmaz, ŌĆ£Mahalle Bask─▒s─▒ Olarak Eksen Kaymas─▒,ŌĆØ┬ĀUSA Sabah Daily, SETA Commentary, September 22, 2010, retrieved from http://www.setav.org/public/HaberDetay.aspx?Dil=tr&hid=48440.

- See Nuh Y─▒lmaz, ŌĆ£De─¤er Eksenli Realist D─▒┼¤ Politika ve Eksen Kaymas─▒,ŌĆØ┬ĀAnlay─▒┼¤, SETA Commentary, November 2009, retrieved from http://www.setav.org/public/HaberDetay.aspx?Dil=tr&hid=5486.

- Mensur Akg├╝n, ŌĆ£Turkey: what axis shift?ŌĆØ┬ĀLe Monde diplomatique English edition Blog Posts, July 9, 2010, retrieved from http://mondediplo.com/blogs/turkey-what-axis-shift.

- Mehmet Babacan, ŌĆ£Whither Axis Shift: A Perspective from TurkeyŌĆÖs Foreign Trade,ŌĆØ SETA Policy Report, No. 4, November 2010, pp. 1-36, retrieved from http://www.setav.org/Ups/dosya/53018.pdf.

- UNCTAD World Investment Report, 2010 and China Investment Promotion Agency of Ministry of Commerce (CIPA).

- World Trade Organization (WTO), 2009, www.wto.org.

- UNCTAD World Investment Report, 2010 and Bloomberg.

- IMF World Economic Outlook (WEO), October 2010, http://www.imf.org/external/pubs/ft/weo/2010/02/index.htm.

- IMF World Economic Outlook (WEO) 2010, Statistical Appendix, Table B16, p. 21.

- IMF World Economic Outlook (WEO) 2010, Statistical Appendix, Table A8, p. 191.

- IMF World Economic Outlook (WEO) 2010, Statistical Appendix, Table A16, p. 204.

- Sally McNamara, Ariel Cohen and James Phillips, ŌĆ£Countering TurkeyŌĆÖs Strategic Drift,ŌĆØ The Heritage Foundation Backgrounder No. 2442, July 26, 2010, p. 14, retrieved from http://thf_media.s3.amazonaws.com/2010/pdf/bg2442.pdf.

- McNamara et al, ŌĆ£Countering TurkeyŌĆÖs Strategic Drift,ŌĆØ p. 14.

- For arguments of the defense of the customs union between the EU and Turkey, See Sinan ├£lgen and Yiannis Zahariadis, ŌĆ£The Future of Turkish-EU Trade Relations: Deepening vs. Widening,ŌĆØ Centre for European Policy Studies and the Economics and Foreign Policy Forum, EU-Turkey Working Papers No. 5, August 2004, p. 30.

- Ay┼¤eg├╝l Din├¦├¦a─¤-├£mit ├¢zlale, ŌĆ£Export Losses in EU markets,ŌĆØ TEPAV Policy Note, July 2010, p. 3, http://www.tepav.org.tr/upload/files/1284637561-9.Export_Losses_in_the_EU_Market.pdf.

- Data from the Undersecretariat for Foreign Trade, 2009.

- Turkish Ministry of Foreign Affairs, www.mfa.gov.tr.

- ŌĆ£A Note on TurkeyŌĆÖs Free Trade Agreements,ŌĆØ Undersecretariat for Foreign Trade, 2009.

- See Jeffrey A. Frankel and David Romer, ŌĆ£Does Trade Cause Growth?ŌĆØ┬ĀThe American Economic Review, Vol. 89, No. 3 (1999), pp. 379-399.

- Babacan, ŌĆ£Whither Axis Shift: A Perspective from TurkeyŌĆÖs Foreign TradeŌĆØ.

- Ahmet Davutoglu,┬ĀStratejik Derinlik┬Ā(─░stanbul: K├╝re Publications, 2001), p. 336.

- Ibid, p. 513.

- Ahmet Davutoglu, ŌĆ£TurkeyŌĆÖs Foreign Policy Vision: An Assessment of 2007,ŌĆØ┬ĀInsight Turkey, Vol. 10, No. 1 (2008), p. 78.

- Ibid, pp. 83.

- Turkish Airlines, www.turkishairlines.com.

- Undersecretariat for Foreign Trade, 2009 Annual Foreign Trade Report and Turkish Statistical Institute (TurkStat).

- Gene M. Grossman and Elhanan Helpman,┬ĀInterest Groups and Trade Policy┬Ā(Princeton, NJ: Princeton University Press, 2002), pp. 173-198.

- See Robert C. Feenstra,┬ĀAdvanced International Trade: Theory and Evidence┬Ā(Princeton, NJ: Princeton University Press, 2004) for a comprehensive understanding on the role of trade in defining economic change.

- TurkStat, 2010.

- IMF forecast for TurkeyŌĆÖs GDP growth in 2010 is 7.8 percent (WEO 2010) while the governmentŌĆÖs projection is revised from 3.5 percent up to 6.8 percent according to the recently announced Mid-Term Economic Program.