Introduction

This article elaborates Turkey’s recent energy strategy with regard to market characteristics, geopolitical issues and foreign policy priorities. It points to Turkey’s growing energy demand as one of the most significant factors that affect the country’s policies. The increase in domestic energy demand raises energy security not only as an urgent matter that awaits affordable and sustainable solutions, but also as an important issue that is highly effective in building regional and global relations.

The link between: (1) the tangible characteristics of energy security (amount, price, timing, location and sustainability); and (2) foreign policy priorities that simultaneously embrace tangible (e.g. bilateral and multilateral relations and agreements concerning trade, military and cooperation) and intangible parameters (e.g. ideals, principles, identity politics and soft power instruments), emerges as an important problematic that deserves further elaboration.

To do this, the following sections analyze Turkey’s energy strategy and elaborate how it responds to current challenges by striking a compromise between market characteristics, and geopolitics and foreign policy. The main assumption of this article is that the tangible parameters of energy security are highly linked to the increase in domestic demand which in turn must be balanced with geopolitics and foreign policy issues; and channel cooperation with the concerned actors despite short-term or long-term political problems.

Turkey’s energy security is based on the availability of resources at affordable prices and sustainable processes

The first section, with conceptual and figurative highlights, gives a brief picture of the energy security challenges that Turkey faces. The second part focuses on Turkey’s official energy strategy (Turkey’s Energy Strategic Plan 2009-2014, as introduced by the Ministry of Energy and Natural Resources, MENR) to understand how, and to what extent, the policies respond to Turkey’s challenges and support the main hypothesis of this article.1 The conclusion discusses the findings and conceptual highlights of the article in order to provide an insight as to how energy security balances geopolitical motives and foreign policy goals on behalf of international cooperation.

The Calculus of Turkey’s Energy Security

Energy security is meant to guarantee a sufficient amount of resources at affordable prices whenever and however the demand arises. In this regard, Turkey’s energy security is based on the availability of resources at affordable prices and sustainable processes.2 Turkey’s geographical features encourage international oil and gas transport projects. However, it is not possible to identify Turkey’s energy strategy as if it merely stems from a geopolitical agenda. Instead, Turkey’s energy strategy arises from policy priorities as much as market characteristics. On the policy side, economic concerns and trade opportunities appear to be effective motivators behind Turkey’s strategy. On the market side, the growth of Turkey’s domestic energy demand leads to initiatives to diversify supplies and suppliers.3 As shown in Box 1, Turkey’s energy policies and investments are highly responsive to domestic demand as well as to international oil and gas pipeline projects.4

The increase in domestic demand puts pressure on Turkey’s need to guarantee supplies from an energy security perspective.5 Although state and governmental institutions remain important actors in the arena of domestic supply, it should be acknowledged that Turkey has entered an era of liberalization. The state, indeed, considered liberalization and privatization as an important means to accelerate infrastructure investments and support supply security.6

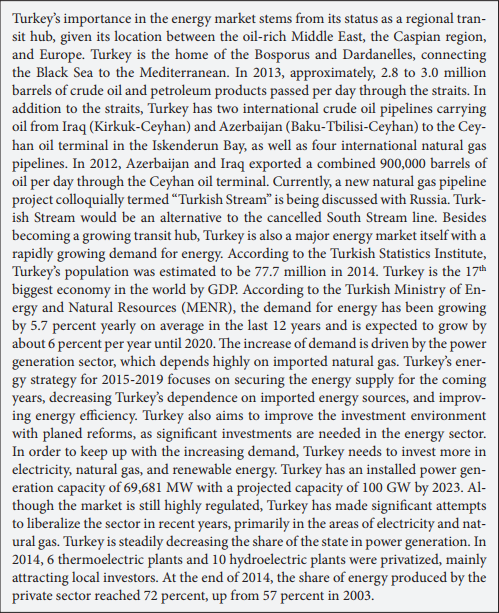

Box 1- Energy in Turkey: Fast Growing Market with Transit Infrastructures

Source: TCK Attorneys, 2015.

The 2001 Law No. 4628, and the secondary legal framework as designed by EMRA, resulted in the transformation of Turkey’s state-centric monopolistic structure into a competitive market, paving the way for further deregulation characterized by the engagement of the private sector in power generation. “The private sector contributed to more than three-fourth of the capacity additions made and played a key role in increasing the installed capacity from 31 846 MW in 2002 to 49 524 MW in 2010, and 53 211 MW at the end of 2011.”7 Electricity production (228.4 billion kWh in 2011) and consumption (229.3 billion kWh) seem to be balanced. This remains costly, since 74.8 percent (171 billion kWh) was generated by thermal plants mainly fueled by natural gas, hard coal and lignite including asphaltit, while allocating a limited share of 25.2 percent (58 billion kWh) to renewable sources such as hydro, geothermal and wind.8

Then Turkish Foreign Minister Ahmet Davutoğlu speaks next to Turkish Energy Minister Taner Yıldız and Transport Minister Lutfi Elvan during a press conference in Ankara, on June 13, 2014. | AFP PHOTO / ADEM ALTAN

Then Turkish Foreign Minister Ahmet Davutoğlu speaks next to Turkish Energy Minister Taner Yıldız and Transport Minister Lutfi Elvan during a press conference in Ankara, on June 13, 2014. | AFP PHOTO / ADEM ALTAN

Having acknowledged this awkward structure, Turkish energy strategy attributed a special significance to gas, nuclear and renewable energy to balance the economic and environmental risks that may arise from the excessive use of coal and oil in the next two decades. The environment, carbon emissions in particular, is an important factor affecting Turkey’s energy security priorities. To state this in terms of numbers, Turkey’s primary energy and electricity demand are expected to almost double and triple respectively by 2030. It is likely for fossil fuels, if the current trend remains, to account for more than 80 percent of the primary energy demand (exceeding 60 mtoe according to the business-as-usual scenario) and resulting in the doubling of carbon emissions from 300 million tons in 2010 to 600 million tons by 2030.9 As an Annex I party to the Framework Convention on Climate Change (UNFCCC) since 18 December 2003, upon approval of Law No. 4990, Turkey ratified Kyoto in 2009, yet declared no explicit target of reduction following the 2009 UN Climate Change Conference held in Copenhagen.10 Carbon emissions, however, appear as an important reference while making energy policies along with other energy supply security parameters.11 This approach lends a special significance to nuclear and renewable energy, which are likely to increase their share in Turkey’s energy mix throughout the next decade.

Oil and gas, in the meantime, not only support Turkey’s energy mix and contribute to direct investments, but also raise the spatial characteristics of pipeline transportation as an important means to foster regional and global cooperation.12 Oil and gas pipelines, along with contracts and agreements, enable Turkey to establish and maintain energy relations with suppliers, while developing new ties with demand-side countries mainly in Europe, as shown in Box 2.13

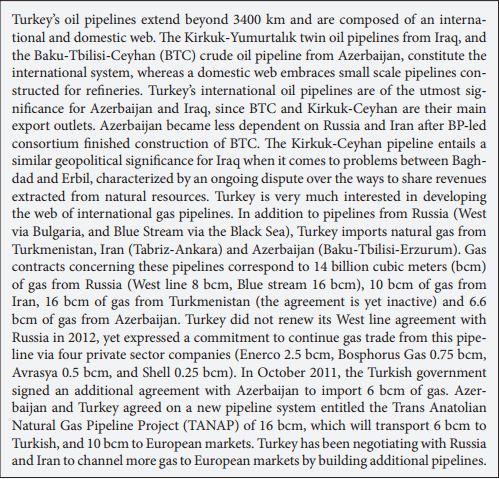

Box 2- Oil and Gas Pipelines

Source: BOTAŞ, 2013a, 2013b, 2013c.

State involvement in pipeline politics and massive investments such as the Akkuyu nuclear power plant is decisive in certain cases in which intergovernmental agreements played an important role in establishing long-term relations. The link between energy security and foreign affairs, however, cannot be fully conceived without factoring in the role of private sector engagement in other countries.14 For instance, Turkish private sector involvement in upstream and downstream business in Northern Iraq was an incentive to maintain good political relations between Turkey and the Kurdish Regional Government (KRG), whereas energy projects with Iraq along with the Kirkuk-Ceyhan pipeline provided strategic leverage for Baghdad to negotiate with Turkey and the KRG. Multinational companies, with investments in the KRG, have proposed a new oil pipeline project from the KRG to Turkey with a capacity of 1 million barrel per day.15 This pipeline is expected to support Turkey’s aim to increase the strategic significance of Ceyhan and turn it into an energy center similar to Rotterdam. In other words, Turkey’s diversification of supplies and suppliers in order to attain a desirable energy mix comes out as a function of volume, cost, time, affordability and sustainability. The international aspect of this approach results in strategic cooperation with many other countries, particularly with Russia (hydrocarbons, transportation and nuclear power), Azerbaijan (upstream, downstream, oil and gas transport), Turkmenistan (upstream, oil and gas), Iran (oil and gas), Iraq (upstream, downstream, oil and gas transport) and Japan (nuclear power).

The Policy Implications of Turkey’s Energy Strategy

Turkey’s energy strategy, as set by MENR, stems from domestic market characteristics. It also reflects global and regional dynamics in conformity with the picture proposed in the previous section. The official strategy proves to be energy security-oriented, with responsiveness to state and private company involvement. This characteristic extensively explains how Turkey synchronizes the tangible characteristics of energy security with geopolitical features and foreign policy priorities.

The Strategic Plan as set by MENR covered the period from 2009 to 2014 with well-defined targets and performance indicators. It furthermore put forward a vision for 2023, the 100th anniversary of the foundation of Turkish Republic. The plan is composed of five strategic pillars: (1) Energy supply security, (2) the regional and global effectiveness of Turkey in the field of energy, (3) the environment, (4) natural resources and (5) corporate structure.

These pillars make sense in terms of three aspects. Firstly, and with regard to the short term from 2009 to 2014, they give an idea about the target figures, which intersect with energy investment plans and consumption patterns in Turkey. Secondly, and with regard to the mid term, they give an idea about the strategic priorities to be addressed between 2014 and 2023. Thirdly, and with regard to spatial characteristics, the way these pillars have been supported by well-defined targets, strategies and policies gives an idea on geopolitical factors.

Private sector involvement is an important factor that interacts with the processes of policy making

Turkey’s growing energy demand is definitely the most urgent matter, followed by an explicit intention to channel more oil and gas from the neighborhood to international markets; boost electricity production from nuclear, coal and renewables; benefit more effectively from domestic resources; and sustain the shift from a hydrocarbon-based energy mix to a more diversified structure that includes oil, gas, coal, nuclear, renewables and other resources.

The aims set for energy security primarily envisage a diversification of supplies and suppliers, with more shares attributed to domestic resources. The first aim within the first pillar is “Providing Diversity in Resources by Giving Priority to Domestic Resources.” It describes short and long term steps to curb dependence on fossil fuels and hydraulic resources. It is designed to ignite a boost in the use of renewable and nuclear energy. Targets set in this regard are (1) domestic oil, natural gas and coal exploration (performance criterion is calculated in terms of coal, oil and gas exploration activities such as drilling wells), (2) increasing the total capacity of coal thermal plants from 200 MW in 2010 to 3500 MW, and (3) starting the construction of Turkey’s first nuclear power plant in 2014.

As to outcomes; Turkish Petroleum (TPAO) along with its partners and affiliates carried out a remarkable progress regarding the achievement of the first goal. Overall investments in exploration, drilling and extraction increased from $100 million in 2002 to $1.36 billion in 2011.16 The second aim delineates a long-term vision to increase the share of renewables in total installed capacity to 30 percent by 2023; and short-term targets for 2014 to complete the construction of another 5000 MW of hydroelectricity. Furthermore, the capacities of wind and geothermal would respectively increase from 802.8 MW (2009) to 10,000 MW in 2015, and from 77.2 (2009) to 300 MW in 2014. To talk numbers, the total installed capacities of 19,568 MW for thermal, 12,240 MW for hydro, and 36.4 MW for geothermal plus wind in 2002 increased to 34,223 MW for thermal, 17,699 for hydro, and 2,019 MW for geothermal plus wind in April 2012.17

The target set for coal-fueled thermal power plants is also quite ambitious, and confronts ecological concerns. As emphasized by the Turkish Government’s Council of Ministers in 2011, in conformity with the Ninth Development Plan (2007–2013), Turkey was very much interested in using more coal for electricity generation while taking full environmental responsibility to curb Carbon emissions.18 This goal may be supportive for decreasing import dependence and balancing overall costs for secondary energy. However, it suffers from outmoded technological applications not only in the mining industry but also in the use of coal-fueled thermal power plants itself. There is an explicit need for technological amendment, which could at least include fluidized bed combustion and carbon capture and storage applications, or the ecological liquefaction of coal and lignite as the Ministry aspires.19

The liberalization process faced market impediments and the state’s strategic priorities in certain cases

The government’s efforts to reach the nuclear targets set by MENR resulted in an intergovernmental nuclear energy agreement between Turkey and Russia which was signed and ratified by the Turkish Parliament in May and July 2010, respectively.20 Following the intergovernmental agreement, Russian Rosatom started activities to construct the first nuclear power facility in Akkuyu, Mersin after establishing the Akkuyu Project Company (APC) in December 2010. The construction of the port to serve the Akkuyu Power Plant was started in April 2015. In the meantime, companies including Japanese, Chinese and Canadian firms were announced to be among the short-listed bidders concerning the second nuclear power plant in Sinop. Turkey and Japan signed an agreement in October 2013 to build a 4800 MW plant in Sinop, the ownership of which would be split by Mitsubishi, Itochu (Japan), Areva, GDF Suez (France) and EUAS (Turkey). The agreement was ratified and approved respectively by the Turkish Parliament and President Tayyip Erdoğan in April 2015 with a schedule to start its construction in 2017.21 The government, in the mean time, declared a strong interest in building a third one, although it gave no clear hint as to its location other than speculations over the Black Sea town of İğneada by the Bulgarian border.22

The third aim comprised a long-term target decrease in energy intensity by 20 percent, which would be a remarkable improvement, from 2008 to 2023. Accordingly, primary energy intensity (kg equivalent oil/1000 dollars in GDP) was expected to decrease from 282 (2008) to 254 (2014). Another target set within this perspective supported maintenance, rehabilitation, modernization and the adoption of new technologies in the state power plants to achieve this goal. The fourth aim was to sustain liberalization of the energy markets and free market conditions to support private sector involvement, and reach a total investment of $126 billion from 2009 to 2020. Legal amendment in 2001 facilitated this process and the installed electricity capacity increased from 31750 MW in 2002 to 44600 MW in 2009, and 53942 in April 2012 with the help of investments from the private sector exceeding 7000 MW. The installed capacity is expected to go beyond 90000 MW in 2023 if private sector involvement continues its trend along with public investments.

Market liberalization has been a main concern of Turkey’s energy policy since the 1980s. International Arbitration Law was applied for the first time in January 2000 to settle disputes between the state and the private sector on public service contracts.23 A rapid and remarkable liberalization ensued. The Electricity Market Law and the Natural Gas Market Law, which were ratified by the Turkish Parliament in 2001, aimed at the full liberalization of the market to break the existing monopolistic structure and support market prices. Other efforts for liberalization are also discernible from the legal amendments. “The 2003 Petroleum Market Law liberalized oil market activities, lifted price ceilings and removed import quotas on petroleum products at the beginning of 2005.”24 The liberalization process took place with important legal amendments in premature sectors to be developed, such as renewable energy. Renewable energy Law No. 5436 of 2005 described the legal framework to promote the use of renewable resources in electricity generation, while an amendment entitled Law No. 6094 of 2010 clarified incentives to be paid to investors in wind, geothermal and sun based power plants.25 “Liberalization and deregulation in Turkey’s national energy policy are expected to be stronger trends due to the growing dynamism of the private sector, the adoption of international business norms, and Turkey’s increasing integration with international markets.”26

Private sector involvement is an important factor that interacts with the processes of policy making. This interaction has two folds. On the one hand, MENR along with other state and non-state regulative institutions such as the Energy Market Regulatory Authority (EMRA or EPDK), defines the legal framework, and then regulates it with direct involvement in the energy sector to avoid non-liberal (e.g. monopolistic) and illegal (e.g. smuggling) practices while maintaining high standards concerning safety, health and the environment (e.g. sample analysis of coal, oil, gas and LPG). On the other hand, liberalization and deregulation increase the role of private companies in regional and international relations.

The liberalization process faced market impediments and the state’s strategic priorities in certain cases. For instance, full implementation of the Natural Gas Market Law would eventually transform the state-based monopolistic structure of the gas supply and distribution sector into a competitive market of private companies. This shift could not be fully accomplished because of the long-term gas supply contracts owned by the state company, BOTAŞ. Illiberal pricing, in the mean time, appeared as one of the important consequences of Turkey’s high reliance on long-term contracts with Russia and Iran, the conditions of which set actual prices with no reference to Spot LNG prices and secures subsidies to keep retail prices affordable at the household level. Another barrier to liberalization was related to concerns over increasing dependence on Russia. Accordingly, and under current regulations, further liberalization in the gas business might have channeled integration between supply and distribution by causing a negative effect on Turkey’s external dependence on Russia. “The opening of the market has set the basis for Gazprom’s dominance, given that the Russian company shows a clear intention to increase its investments in Turkey: it has already signed a deal with Turkish Aksa Energy for the import and distribution of Russian gas, as well as for the construction of a terminal; it plans to increase its stakes in the gas distribution company Bosphorus Gas from 40 to 71 percent, and it is engaged in ongoing negotiations with BOTAŞ for the import of Russian gas.”27

The groundbreaking ceremony of Trans-Anatolian Gas Pipeline Project which will transport natural gas from Azerbaijan through Turkey to Europe. | AA PHOTO / AHMET OKATALI

The groundbreaking ceremony of Trans-Anatolian Gas Pipeline Project which will transport natural gas from Azerbaijan through Turkey to Europe. | AA PHOTO / AHMET OKATALI

The fifth aim emphasizes the risks arising from external dependence on a limited number of countries, particularly concerning oil and gas supplies. It then underlines the need to diversify resources from abroad, mainly by increasing the oil and gas production of Turkish companies in other countries and overseas, and decreasing extreme dependence on one country. Another target set in this aim was to double Turkey’s natural gas storage capacity from 2.1 bcm in 2009 to 4 bcm in 2014, and increase oil stock capacity. However there was not any clear-cut target set for this goal, and it is subject to the establishment of a national oil stock agency that remains delayed.

The sixth aim concerns the spatial characteristics of energy trade and therefore recalls the geopolitical aspect, although without mentioning it. The strategic pillar is entitled, “Regional and global effectiveness of Turkey in the field of energy.” It starts from the strategic significance of Turkey’s location neighboring 72 percent of the world’s proven oil and gas reserves. The sixth aim was to use this spatial advantage. It envisaged an increase in oil and gas transport from the Middle East and Eurasia to world markets via Turkey. The long-term goal was to make Turkey an energy hub by the help of additional infrastructure, grids, pipelines and other upstream and downstream facilities. Pipelines would play a prominent role in the achievement of this goal. The plan put emphasis on oil transport from Iraq (Kirkuk Yumurtalık Twin Pipelines) and from Azerbaijan (Baku-Tbilisi-Ceyhan), with a clear commitment to attain the full capacity of the BTC pipeline. It furthermore indicated alternative oil pipeline projects such as the Samsun-Ceyhan Pipeline project that was expected to promote Ceyhan’s international role by facilitating massive refinery investments in the region. Ceyhan, along with İzmir, takes a pivotal role within this process since MENR is intended to turn Ceyhan into an energy terminal supported by refineries, petrochemical facilities, LNG terminals, gas liquefaction units and LNG trains. The role of Ceyhan may even go further and start looking like that of Rotterdam’s if oil, gas, LNG and marine transportation systems can be supported by a regional oil price-setting mechanism for the Mediterranean. Regarding gas transport to Europe, Turkey’s unique location between supply and demand leads to important projects most of which are destined for European markets.28 The Turkey-Greece Gas Interconnector, the construction of which begun in 2002 and completed in 2008, technical preparations for building the Turkey-Greece-Italy Interconnector natural gas pipeline, and Babaeski-Filippi line, which was completed in June 2008, can be exemplified as positive outcomes of EU-Turkey Energy Security Cooperation. Turkey seeks to build upon this infrastructure by channeling additional gas pipelines, as in the case of TANAP and other related projects. It is therefore possible to point out Turkey’s growing role in energy transport in conformity with the targets set in this pillar.

What about the way these pillars affect foreign policy? In theory, the sixth aim, as set by MENA, intersects with the priorities set under the energy chapter of the Ministry of Foreign Affairs (MFA), unlike other energy security priorities. The MFA attributes a special significance to gas pipeline projects with the assumption that they contribute to Turkey’s foreign policy strategy.29 MFA’s 2014 report refers to natural gas pipelines and directly points to the Baku-Tbilisi-Erzurum (BTE) Natural Gas Pipeline, which has been operational since 3 July 2007. It then indicates why the Southern Gas Corridor will be very important with gas transport options from the Caspian region and the Middle East. The MFA document finally refers to TANAP, since the government and the ministries took leading roles in signing the Memorandum of Understanding with Azerbaijan on 24 December 2011, and the Intergovernmental Agreement and Host Government Agreement on 26 June 2012 in Istanbul.30“The construction of the Trans-Anatolian Pipeline, TANAP (including Azerbaijani gas and potentially Turkmen gas); the Samsun/ Ünye -Ceyhan pipeline (Kazakh oil) and the increase in the volume of Kazakh oil transported through the BTC oil pipeline could further increase the role of Turkey as a transit state.”31 Having acknowledged this possibility, the MFA document refers to existing and proposed oil and gas pipelines. It describes the Baku-Tbilisi-Ceyhan (BTC) pipeline as the main pillar of the East-West Energy Corridor, and mentions the significance of the Iraq-Turkey (Kirkuk-Yumurtalık) Crude Oil Pipeline System. According to the MFA, increasing vessel traffic through the Turkish straits should be avoided via the construction of aSamsun-Ceyhan by-pass oil pipeline, the protocol of which was signed in August 2009 during Russian Prime Minister Putin’s visit to Turkey. The MFA also acknowledges that these three pipelines would help transport 6 to 7 percent of the global oil supply to Ceyhan, which was expected to become a major energy hub once the three pipelines (two existing, one proposed) start functioning at full capacity.

Turkey’s energy agenda intersects with foreign policy priorities which characterize an interaction among a myriad of actors

Additionally, the MFA attributes a special importance to the need for opening the energy chapter with the EU, since it appears to be an important step not only for Turkey’s accession, but also for consolidating European energy security. Turkey, as a candidate country, has obtained an observer status in the Energy Community, and is on the way to becoming fully integrated with the European electricity transmission systems and natural gas transportation infrastructure. Turkey wants to become a part of the European grid, with more two-sided facilities for electricity imports and export, not only to make proposed massive investments feasible, but also to increase regional cooperation, and avoid the negative influence of seasonal variations related to cost and availability. The regulatory harmonization and physical connection of the national power system with the Union for the Coordination of Transmission of Electricity (UCTE) led to a number of projects which are expected to facilitate the completion of priority axes number four (Greece Balkan countries) and number nine (Mediterranean Electricity Ring) under the Ten-E umbrella.32

The seventh aim has been described under the third strategic pillar of energy, and it is about minimizing the negative environmental impacts of the activities related to energy and natural resources. Statements made under this aim mention how MENR will be committed to curbing carbon emission (especially CO2 emission released during electricity production) in conformity with Turkey’s plans, yet puts more emphasis on the need for environmentally friendly applications and the sustainable management of the energy sector, especially when it comes to mining operations which do not comply with ecological standards.

Mining and natural resource extraction are considered to be an important leitmotiv for the next strategic pillar entitled “Natural Resources.” The eighth aim is intended to increase the share of domestic resources within primary and secondary energy supply. Mining operations appear to be an important target since the plan aimed to double the revenues extracted through mining from $3.2 billion in 2008 to $6.4 billion in 2014, and did this in due course. The ninth aim was to increase the production of industrial raw material, metal and non-metal mineral reserves, and expand their domestic use with relevant research and development activities.

The final strategic pillar is about corporate capacity, and delineates two aims as means to improve the quality and efficiency of MENR and its affiliates. To this end, the tenth aim is about the managerial aspect of energy strategy; it expresses a clear commitment to improving the quality and efficiency of human resources, where as the eleventh, and the last, attributes a pioneering role to MENR concerning research, development and innovation.

Conclusion

The previous sections point to a link between energy strategy, geopolitics and foreign affairs driven by supply security issues on behalf of international cooperation between Turkey and its counterparts. If energy security is the most important factor that shapes Turkey’s actual energy strategy, then what is the most appropriate way of defining the role of Turkey’s energy strategy in easing, freezing or solving political and regional problems and promoting cooperation stemming from energy affairs? To ask theoretically, how do the factors of energy security intersect with foreign policy priorities stemming not only from tangible factors based on rational calculations, but also from intangible factors? To ask practically, how can we combine Turkey’s energy security, energy strategy and foreign relations from this perspective?

Theoretically speaking, Turkey’s energy agenda intersects with foreign policy priorities which characterize an interaction among a myriad of actors including, but not limited to, the Ministry of Energy and Natural Resources, the Ministry of Foreign Affairs, and non-state actors including private companies. Conceptual differences between these actors emerge in terms of the tangible characteristics of energy security facing the intangible features of foreign policy priorities. The first one, energy security, needs to be quantified as it is based on security parameters such as volume, price, availability and sustainability. Whereas the second one, foreign policy, is more than a sum of quantitative factors and includes a myriad of intangible considerations varying from identity politics and humanitarian action to long-term ideas and principles. There is indeed a sharp difference between the tangible characteristics of energy security and the multi-faceted pillars of foreign policy, which may prioritize cooperation or conflict on behalf of these intangible features to support soft power strategies, identity politics, ideological factors, long-term goals or geopolitical expectations.

Turkey has coped with this conceptual confrontation since energy security has played a pivotal role

Practically speaking, Turkey has thus far coped with this conceptual confrontation since energy security has played a pivotal role in building mutually beneficial strategic partnerships and enhancing foreign policy pillars. One can describe this compatibility, as this article did, with reference to synchronization between the Ministry of Foreign Affairs, the Ministry of Energy and Natural Resources, and the successful engagement of non-state actors in due course. Energy security priorities, indeed, maintained functional trade channels with diverse actors whose regional priorities did not fully converge with each other.

To conclude, this energy security perspective helps in understanding that “energy security priorities make Turkey conceive of every actor as an actual or potential partner with whom political problems may be solved, or be frozen, on behalf of mutual benefits.” In turn, Turkey’s energy strategy converges with foreign policy issues and geopolitical features by playing a sort of balancer’s role to foster regional and global cooperation.

Endnotes

- Ministry of Energy and Natural Resources (MENR), Turkey’s Energy Strategic Plan 2009-2014, (Ankara: MENR, 2010).

- M. S. Kiran, E. Özceylan, M. Gündüz and T. Paksoy, “A Novel Hybrid Approach Based on Particle Swarm Optimization and Ant Colony Algorithm to Forecast Energy Demand of Turkey,” Energy Conversion and Management, Vol. 53, No. 1, (2012), pp. 75-83.

- Mert Bilgin, “Geo-economics of European Gas Security: Trade, Geography and International Politics,” Insight Turkey, Vol. 12, No. 4, (2010), pp. 185-209.

- TCK Attorneys (Tiryakioğlu, Çakmakçı Keşmer), Turkish Energy Market 2015, (14 March, 2015), https://www.tckattorneys.com/en/turkish-energy-market-2015/, retrieved 6 April 2015.

- DEK-TMK, Enerji Raporu 2012, (Ankara: Poyraz, 2012).

- M. S. Sirin, “Energy Market Reforms in Turkey and Their Impact on Innovation and R&D Expenditures,” Renewable and Sustainable Energy Reviews, Vol. 15, No. 9, (2011), pp. 4579-4585.

- EPDK (EMRA), Turkish Energy Market: An Investor’s Guide 2012, (Ankara: EPDK, 2012), p. 15.

- Ibid, p. 16.

- S. Karbuz and B. Şanlı, “On Formulating a New Energy Strategy for Turkey,” Insight Turkey, Vol. 12, No. 3, (2010), p. 92.

- E. B. Peterson, J. Schleich and V. Duscha, “Environmental and Economic Effects of the Copenhagen Pledges and More Ambitious Emission Reduction Targets,” Energy Policy, Vol. 39, No. 6, (2011), pp. 3697-3708.

- Ibid, p. 3704.

- BOTAŞ (2013a), “Doğal Gaz Faaliyetleri,” http://www.botas.gov.tr/index.asp, retrieved 23 March 2014.

- BOTAŞ (2013b), “Gaz Alım Anlaşmaları,” http://www.botas.gov.tr/index.asp, retrieved 23 March 2014.

- Mert Bilgin, “Geo-economics of European Gas Security: Trade, Geography and International Politics,” Insight Turkey, Vol. 12, No. 4, (2010), pp. 185-209.

- BOTAŞ (2013c), “Ham Petrol Taşımacılık Faaliyetleri,” http://www.botas.gov.tr/index.asp, retrieved 23 March 2014.

- ETKB, Dünyada ve Türkiye’de Enerji Görünümü, (Ankara: ETKB, 2012).

- Ibid.

- K. Baris, “The Role of Coal in Energy Policy and Sustainable Development of Turkey: Is It Compatible to the EU Energy Policy?,” Energy Policy, Vol. 39, No. 3, (2011), pp. 1762-1763.

- Ibid.

- TAEK, “Turkish Atomic Energy Authority, Akuyu Nuclear Power Plant, 2013,” retrieved 15 February 2014, from http://www.taek.gov.tr/eng/services/206-akkuyu-nuclear-power-plant/789-akkuyu-nuclear

-power-plant.html. - WNS, “Erdoğan Approves Turkey Japan Nuclear Agreement,” World Nuclear News, 10 April 2015, retrieved 14 April 2015, from http://www.world-nuclear-news.org/NN-Erdogan-approves-Turkey-Japan

-nuclear-agreement-1041501.html. - JTW, “Turkey in 3rd Nuke Plant Bid,” Journal of Turkish Weekly, 22 October 2012, p. 17.

- IEA, International Energy Agency, Energy Policies of IEA Countries: 2003 Review, (Paris: OECD, 2013), p. 253.

- IEA, International Energy Agency, Energy Policies of IEA Countries: Turkey 2005 Review, (Paris: OECD, 2005).

- A. Baskan, “Liberalization of Turkey’s Hydroelectricity Sector,” in A. Kibaroğlu, W. Scheumann and A. Kramer (eds.), Turkey’s Water Policy, (New York: Springer, 2011).

- Ibid, p. 90.

- D. Triantaphyllou and E. Fotiou, “The EU and Turkey in Energy Diplomacy,” Insight Turkey, Vol. 12, No. 3, (2010), pp. 55-62.

- M. Bilgin, “Geopolitics of European Natural Gas Demand: Supplies from Russia, Caspian and the Middle East,” Energy Policy, Vol. 37, No. 11, (2009), pp. 4482-4491.

- MFA, TC Dışişleri Bakanlığı 2013 Faaliyet Raporu, (Ankara: Dışişleri Bakanlığı, 2014), pp. 139-141, retrieved 14 April 2015, from http://www.mfa.gov.tr/site_media/html/2014_mali_rapor.pdf.

- TANAP, “Trans-Anatolian Natural Gas Pipeline Project,” retrieved 23 March 2014, from http://www.tanap.com/en/.

- A. Balcer, “Between Energy and Soft Pan-Turkism, Turkey and the Turkic Republics,” Turkish Policy Quarterly, Vol. 11, No. 2, (2012), p. 159.

- L. Carafa, “Domestically Driven, Differentiated EU Role Adoption: The Case of Energy Sector Reform in Turkey,” in F. Morata and I. S. Sandoval (eds.), European Energy Policy: An Environmental Approach, (Cheltenham: Edward Elgar, 2012), p. 183.