The aim of this paper is to analyse Turkey’s energy security perceptions and its placement in the new energy geopolitics. Like most countries that rely heavily upon imported energy sources, Turkey’s energy policy is shaped by the broad definition of energy security. However, energy security is a term that means different things to different people. In northern Europe, energy security means reducing carbon emissions; in Eastern Europe, it means diversifying to counter an over reliance on Russian gas imports. For the Turkish government, it means avoiding a reliance on imported energy sources and supplying energy at a reasonable cost to the Turkish population.

This article will examine the latest developments in Turkey’s energy policy and look at how the government is planning to meet the present challenges. It will show how the current policies are unlikely to meet growing demand without an expensive reliance on imported natural gas. This study also aims at discussing Turkey’s energy policies within the context of the new energy geopolitics. Hence the article seeks answers to the following questions: How is energy security perceived in Turkey, and hence how are its energy-related policies formulated? What is Turkey’s position within global energy security dynamics and why does Turkey matter for the new energy geopolitics?

Energy today has become one of the important generators of spatial geopolitics by emphasizing the ownership of hydrocarbon resources and control over pipelines routes

The New Energy Geopolitics

Geopolitics is a generic term that covers “conceptual and terminological tradition in the study of the political and strategic relevance of geography.”1 The term covers the relationship between the conduct of foreign policy, political power and the physical environment. Historically, energy commodities have constituted geopolitical instruments. Under the global market economy, suppliers compete in the market and energy-producing countries can use energy as a regulative instrument. Hence, the issue of control of and access to energy resources appears as an indispensable part of any states’ geopolitical considerations. The 18th century British and 19th century German power politics based on the control of energy resources illustrate the close link between geopolitics and energy.2 Similarly, the United States’ quest for accessing oil resources overseas has dominated 20th century geopolitics. In the early 1980s the term ‘resource war’ became popular in the United States because of the perceived Soviet threat to American access to Middle Eastern oil and gas.3

To draw attention to the close link between geopolitics and energy, with his renowned “Heartland theory,” Halford Mackinder argued that the one who controls or influences the export routes and the oil and gas resources of the Heartland, the geographical area that covers Eastern Europe including Russia and most of the Black Sea, dominates the world.4 After the end of the Cold War, the geopolitical significance of the greater Middle East has continued unabated, and the United States has extended its control over this energy-rich region to ensure that no single power should control its ‘geopolitical space.’5 In the post-Cold War era, a new geopolitics based on resource flows has prevailed over the old Cold War geopolitics drawn by ideological divides.

As global energy consumption continues to rise, there is more competition than ever over access to resources, and more attention is being given to protecting energy supply routes. Against this background, energy today has — more than ever — become one of the important generators of spatial geopolitics by emphasizing the ownership of hydrocarbon resources and control over pipelines routes.

The post-Cold War shift in international security from a security concept based on ideological differences to one that revolves around securing access to and control over energy resources has required further understanding and conceptualization of the link between energy and geopolitics. Within this context, Ülke Arıboğan discusses the concept of energeopolitics,6 and Mert Bilgin discusses new energy order politics, or neopolitics, within which the will and capabilities of big and rising powers consolidate their authorities.7

The threat of declining oil production, the rise of natural gas, and new forms and uses of energy and energy security have become important issues for the energy sector today. As Arıboğan and Bilgin argue, the main problem is the fact that upcoming age of energy is influenced by multiple actors rather than one hegemon or two superpowers.8 The current global energy dynamics are dominated by five major actors, each with different agendas and interests: The United States, the EU, the developing world including China and India, energy producers, and anti-status quo and regulative non-state actors like international and national oil corporations.9 In short, the post Cold War political and economic power shift eastward, the strong demand stemming from growth in China and India, the rise of resource nationalism, and the interference of national and international oil corporations appear as the main factors that have shaped the new and complex field of energy geopolitics.

As noted by Michael Klare, the new energy geopolitics is subject to the influence of two troubling trends. The first is an unprecedented increase in future energy demand thanks to newly industrialized capitalist states like China and India which are expected to account for nearly half of the global increase.10 Indeed, the rise of new regional and global powers, the gap between global-level energy supply and demand, the concentration of non-renewable stocks of oil and gas in the Greater Middle East, and the spread of industrial capitalism into China and India could trigger a new “Great Game” as global powers compete for access to and control over energy resources.

In the new energy geopolitics or new energy order, India and China have grown into two of the biggest consumers of Eurasian energy resources, thus becoming major competitors to the United States and the EU. The growth witnessed in China and India has added considerable pressure to the global demand for more energy sources. Currently India imports 70% of its oil and gas. Consequently, India has extensively searched for long-term agreements with supplier states. Similarly, China has just signed a US$ 100 billion contract to purchase crude oil and natural gas from Iran for a period of 25 years.11 Conversely, facing the geopolitical effects of its growing dependence on external energy suppliers, especially for the highly preferred natural gas, the EU is trying to vary both its supplies and suppliers. The uncertainty of gas imports from Russia and the deficit between energy consumption and production in Europe has led the European states to pursue other supply options besides Russia. However, other countries like India, Pakistan, and China are also potential long-term customers for the EU’s alternative suppliers. Intense competition for energy supplies between Asia and Europe and the long-term deals between Asian powers and energy suppliers could cause a considerable decrease in share of the Union in the regional supplies.

Energy has become the key strategic asset in securing Russia’s economic security, along with its global status as a superpower. In order to localize power in the hands of the government, Vladimir Putin successfully renationalized control of energy resources, taking a controlling share of Gazprom, the largest Russian extractor of national gas. Both Russia and Iran’s rise as energy superpowers and their power play with Europe and the United States have caused serious concerns about the future of the global balance of power. Given the current debate on sanctions against Iran, and the Russian government’s efforts to dominate the global energy market, the possibility of a coordinated energy strategy between Iran and Russia could have severe implications for the new energy geopolitics. By lying at the heart of the energy geopolitics in Eurasia, such an alliance between the two energy superpowers of the region could affect the Eurasian space all the way to China and India in the east and to Europe in the west.12

Last but not least, pipeline politics plays a significant role in the current state of affairs in energeopolitics. Transporting energy may be an issue of supply and demand, but essentially it is determined by geopolitical concerns. Within the context of new energy geopolitics, the routes of pipelines have become the subject of geopolitical competition – for power, influence, and for economic advantage.13 Besides being choke points for busy tanker lanes, including Hormuz, the Turkish straits, and the Suez and Panama canals, hydrocarbon transmission through transnational pipelines has become a coveted target for energeopolitical competition. Control over the pipelines and resources has made Russia an energy superpower. By reducing the gas flows and investing in pipeline infrastructure in the former Soviet republics, Russia has been able to exert power on its near abroad. In a similar way, the power play between Iran and the United States in the Middle East also focuses on pipeline politics. The United States’ insistence on excluding Iran from every possible pipeline project including Nabucco, which is projected to carry Central Asian gas to Europe, and its objections to the Iran-Pakistan-India route, reflect America’s strategy to isolate Iran in the region.

In the context of the move towards a multi-centered energeopolitical order where Russia and China rival the United States and the EU, some actors like Turkey have found themselves at the center of attention as energy hubs

In the context of the move towards a multi-centered energeopolitical order where Russia and China, as energy superpowers, rival the United States and the EU, some actors like Turkey have found themselves at the center of attention as energy hubs. As underlined by Arıboğan and Bilgin, both the United States and the EU will need the cooperation of Turkey to include at least two of the energy rich countriesin the region, Azerbaijan, Turkmenistan – and possibly Iran – in the region within the European energy system.14 Given its geographical and strategic position, Turkey has emerged as a key actor in the new energy geopolitics. The Russian and Chinese challenge to the United States and Europe, accompanied by the rise of Iran as a regional power, have helped Turkey to gain strategic leverage. In the following sections, Turkey’s energy security perceptions and placement within the global energy dynamics, as well its energy-oriented foreign policy making will be analysed. Turkey’s role as an energy hub vis-a-vis the leading actors of the energy market such as the United States, the EU, China, Russia and Iran will also be discussed.

Turkey’s Energy Security Perceptions

In the Ministry of Energy’s Strategic Plan for 2010-2014, released in April 2010, Turkish energy minister Taner Yıldız wrote that the “main target is to provide energy resources to all consumers adequately, with high quality, at low costs, securely and in consideration of the sensitivities about environmental matters” plus “reducing the import dependence of our country in energy supply.”15 Mission statements in strategic plans, such as this one, are typically vague and far-reaching. However, it is noteworthy that there are two somewhat unrelated aims in the strategy: first, to reduce Turkey’s dependence on energy imports, and second, to increase the amount of energy products that are transported through Turkey.

To meet the first goal of reducing domestic reliance on imported energy sources, there is a “headline goal” of exploiting all domestic energy sources, including coal and renewables, and building nuclear power plants by 2023, the 100thanniversary of the foundation of the Turkish Republic. Part of this goal is aimed at reducing dependency on any single energy supplier. The second goal is to turn the country into an “energy hub,” primarily through the construction of pipelines linking hydrocarbon reserves in countries bordering Turkey with the demand, which in this case is Europe. This latter goal is somewhat unusual in an energy strategy, as it is more a matter of foreign policy than domestic energy policy. However, it shows how the government is trying to use energy for political purposes.

To understand the energy strategy that Turkey needs to implement it is first necessary to look at the current energy situation in Turkey. Firstly, energy demand is on the rise in Turkey. Although in fits and starts due to numerous economic crises, either domestic crises as in 2001 or international ones as in 2008-2009, Turkey’s GDP has consistently risen, going from 8,000 euros per capita in 2000 to 11,400 in 2008. There was negative GDP growth in 2008, but growth is expected to return in 2010, at 2.8%, and to increase to 3.6% in 2011. As would be expected, energy consumption has increased during the same period. From 1996 to 2007, Turkey’s primary energy consumption grew by almost 50%, from 67.6 million tonnes of oil equivalent (Mtoe) to 101.5 Mtoe, an average annual growth rate of 4%. Per capita consumption of energy in Turkey is still around a third compared to EU countries and so growth is to be expected to continue.16 In 2009 the government projected that primary energy consumption will increase to 222 Mtoe by 2020, an annual growth rate of 6%.17

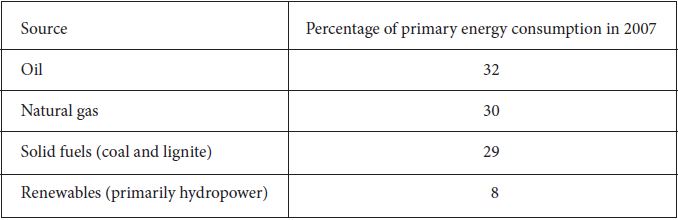

Table 1 shows the breakdown in primary energy consumption in Turkey. Turkey has relatively small domestic reserves of fossil fuels, apart from lignite (low quality brown coal). Therefore, as demand has increased so has the share of imported energy sources in total energy consumption, from 60.1% in 1997 to 73% in 2007. In 2008, 97% of natural gas, and similar percentages of oil and hard coal were imported.18 The primary reason for the large increase in dependency on imported energy sources in the last decade was an almost four-fold increase in natural gas imports, from 8.3 Mtoe in 1997 to 30.4 Mtoe in 2007, an average annual increase of 13.8%. Hydropower is the only large domestic energy source. Oil, which is primarily used for transportation, had a much slower annual increase, at 1.6% between 1997 and 2007.19 As Turkey also starts to align its domestic policies with EU norms, there will be a need to shift to gas for environmental reasons as natural gas produces only half as much carbon emissions per unit of output compared to coal.20 Gas consumption is projected to increase by an average of 5% per year between 2009 and 2020.21

Table 1. Breakdown of sources of primary energy consumption in Turkey in 200722

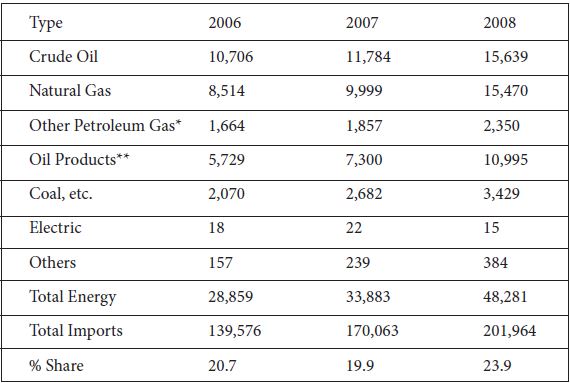

The reliance on imported energy sources affects Turkey’s economy in several important ways. In 2006 and 2007, the share of energy in total imports was around 20%, accounting for US$29 billion in 2006 and US$34 billion in 2007. The share of energy increased to 23.9% and US$48 billion in 2008, probably due to the large increase in oil prices in 2008. Table 2 provides a breakdown by energy source.23

Table 2. Energy imports (in million of USD)

* LPG, Butane,Propane

** Gasoline, Fuel oil, Diesel oil

During the same period, electricity demand also increased. Between 1996 and 2008, installed generating capacity, the total amount of power plants, doubled from 21 GW to 42 GW. In 2008, natural gas-fired plants had the largest installed capacity with 15.1 GW, followed by hydropower with 13.8 GW, lignite with 8.2 GW, hard coal (mostly imported) with 2.0 GW, other fossil fuels at 2.3 GW, and wind and geothermal with 0.4 GW. The increase in generating capacity from 1996 to 2008 was primarily due to the construction of 12 GW of natural gas-fired plants and 4 GW of new hydropower plants.24

In terms of energy policy, the question of natural gas supply will become the most important one

In 2008, the peak load in the electricity system, the highest total power demand at any one time, was 31 GW.25 Typically, there should be around 20-25% more generating capacity than peak demand to ensure there is a reserve of power plants in case of accident or breakdown. According to TEIAS (Türkiye Elektrik İletim A.Ş., the Turkish electricity grid operator), peak demand is projected to increase to between 52 and 55 GW by 2018. Assuming a similar reserve of around 25%, there will need to be between 65 and 69 GW of power plants in Turkey by 2018, an almost 50% increase from 2008. In TEIAS’s low-growth projections, planned power plants and those under construction (again mostly natural gas and hydropower plants) should just about cover demand by 2018; however, in the high-demand scenario there will not be sufficient power plants to meet demand by 2018 and there will be blackouts without additional construction.

It is clear that large investments in the energy sector will be required. Starting in 2001, the energy market has been slowly liberalized and private companies have been investing and building new power plants and other forms of infrastructure. Since 2003, just over half of all new power plants built are privately owned and private companies are expected to build 11 GW of new power plants by 2018, compared to around 5 GW by the state-owned power generator EÜAŞ (Elektrik Üretim A.Ş.). Around a third of the new privately built plants will be hydropower, while most of the remaining will be gas-fired.26 There is a trend in countries that have liberalized their energy sector for investment to focus on gas-fired plants, known as the “dash for gas,” due to their lower investment costs and flexible operating conditions meaning they can quickly respond to changes in demand and market prices.

In addition, most of Turkey’s domestic coal reserves are lignite, which is low quality and more polluting than gas. In terms of nuclear power, an agreement with South Korea’s Kepco to build a 5.6 GW nuclear plant near Sinop was signed in March 2010. This agreement followed the failure of another nuclear power project near Mersin where the only bidder, Russia’s Atomstroyexport, offered a price that was unacceptable to the government, although it appears that a new bid will be successful.27 However, it would be unlikely for any new plant, even the Kepco plant which is a proven design, to be operational by 2020. The recent European experience of nuclear power construction has been one of long delays and cost overruns.

Given the liberalization of the market, increasing energy demand, and a need to limit carbon emissions, natural gas will continue to play a large role in Turkey’s energy mix, especially as the natural gas network expands to more communities and replaces lignite and coal for domestic heating. In terms of energy policy, the question of natural gas supply will become the most important one. Oil is mostly traded on the open spot market and can easily be transported. Therefore, peak oil concerns aside, supply of oil is generally not a problem as long as the customer is willing to pay the market price. Also, as mentioned above, as oil is generally used only for transportation, the rate of increase is much slower than for gas.

Turkey has long-term gas supply contracts with five countries. Natural gas is more of an infrastructure issue than oil as it is much harder to transport. Given the costs of developing infrastructure, the norm in the European gas market has been long-term oil-indexed gas supply contracts, with delivery either through pipelines or in the form of liquefied natural gas (LNG) transported in ships from countries such as Algeria, Qatar, and Nigeria, that do not have direct pipeline routes to export markets. There is a spot market for gas as well that is used to balance supplies, but the spot market is not used as widely for gas as it is for oil.

Typically, between 60-65% of natural gas consumed in Turkey comes from two pipelines with Russia. This share was reduced in 2009 due to decreased demand, but imports from Russia are expected to return to normal levels in 2010 and 2011. Both Iran and Azerbaijan, through the Baku-Tbilisi-Erzurum pipeline (BTE, also known as the South Caspian pipeline), export gas to Turkey through pipelines. Turkey also receives LNG from Algeria and Nigeria. These supplies are delivered through long-term contracts, generally for between 15 and 25 years.28 Less than 1% of gas consumption is purchased on the spot market.29

The government’s energy strategy intends that no one country will supply more than 50% of Turkey’s gas consumption. Given the large share of Russian gas in imports, already more than 50%, this target is aimed directly at Russia. Although there is the potential for large oil and gas reserves to be found under the Black Sea, it is not yet apparent how large they are and if they are economically recoverable.30 Either way, even if development is feasible, it would be unlikely for any offshore development to start producing gas before 2020.

Therefore, with energy demand increasing, and with Turkey locked into long-term supply contracts, the only way the government’s target can be achieved is to find new gas suppliers.

Politics will dictate the development of the gas corridors, in particular the relationship with Russia, and the problems in securing gas supplies

The need for new suppliers, and the plan to increase nuclear power production to reduce domestic demand for gas, brings us to the second part of the government’s energy strategy: to turn Turkey into a transit hub for suppliers in the Middle East and Central Asia to Europe. This is not so much an energy issue as it is a geopolitical issue and needs to be discussed as such.

New Energy Geopolitics: Turkey as Energy Hub

For the Turkish government, there are two primary reasons to make the country an energy hub, a transit route for the so-called “fourth corridor” of gas suppliers in the Middle East and the Caspian basin (Norway, Algeria and Russia being the other three corridors). The first is to guarantee the security of supply, particularly for gas. The Turkish government has always insisted on the right to take some of the gas in transit pipelines for their own consumption, known as offtake rights. The second reason is to gain political influence in Europe and in the region due to the ownership of a key infrastructure route.

Politics will dictate the development of the gas corridors, in particular the relationship with Russia, and the problems in securing gas supplies. For Russia, energy policy and foreign policy are interrelated.31 The same is true for Turkey. By becoming the center of the transit routes for hydrocarbons between the Caspian, the Middle East and Europe, Turkey will be able to increase its influence in the region. This would allow Turkey to leverage the government’s policy, formulated by foreign minister Ahmet Davutoğlu, of “zero problems with neighbors,” in many cases the neighbors that will be supplying the hydrocarbons.

After the 2008 Russian-Georgian war and the 2009 dispute between Russia and Ukraine, which led to the shutting off of a major part of European gas imports, the EU realized it needed to diversify its supplies of natural gas, a goal that will become more critical as the demand for gas is growing in Europe just as domestic supplies are depleted.32 Turkey could present itself as the solution to Europe’s energy problems.

There are a number of pipeline projects being considered that are designed to turn Turkey into an energy hub. The first is the Interconnector-Turkey-Greece-Italy (ITGI) gas pipeline. This project is an extension of the Turkey-Greece gas pipeline, which brings gas from Azerbaijan to Greece, to southern Italy and then to the European network. The project, led by the Italian utility Edison, DEPA (the Greek public pipeline corporation) and BOTAŞ (Boru Hatları ile Petrol Taşıma Anonim Şirketi, the state-owned Turkish pipeline company) envisages 8 billion cubic meters a year of gas moving from Azerbaijan to Italy through Turkey and Greece starting in 2015, increasing to 15 billion cubic meters a year.33

A much more ambitious proposal is the Nabucco gas pipeline, a 7.9 billion euro project to build a 30 billion cubic meter a year pipeline from Turkey up through the Balkans to Austria. The project is supported by BOTAŞ, Bulgarian Energy Holding (BEH), the Austrian OMV, the Hungarian MOL, the Romanian Transgaz, and the German utility RWE. The European Commission supports the project. Azerbaijan would supply the gas in the initial stages, and then possibly Turkmenistan, and potentially later Iran, Iraq and Egypt. Construction is due to start in 2011, with gas flowing as of 2014.34

Despite the potential of these projects, Russia has historically held the monopoly on imports of Eurasian natural gas to Europe through its Soviet-era pipeline network, now owned by Gazprom, and this has given the country a strong geopolitical influence. It is an influence that Russia wants to retain. And after the 2008 Russian-Georgian war, the message was clear: Russia has the military power and will to dictate terms in its near abroad when it feels its position is weakening. The Turkish government is clearly aware of this message.

Russia’s attempt to maintain its monopoly on the supply and transportation of Eurasian gas can be seen in the Russian-proposed South Stream gas pipeline, a pipeline that could potentially compete with Nabucco. The South Stream project is a proposed 60 billion cubic meters a year natural gas pipeline running under the Black Sea, thereby bypassing Ukraine, and exporting Russian and Central Asian gas. The project is led by Gazprom and Eni, an Italian energy company, and is expected to cost 20 billion euros. The Austrian company OMV, also a partner on the Nabucco pipeline, recently joined the consortium, as well as Slovenia, Croatia and EdF from France. Construction is due to start in 2011, with the initial stages completed by 2015.35

Russia works to entice suppliers into using its pipelines using both threats and promises. The 2008 Georgian war was the threat, when it became clear that pipelines in the region were potentially vulnerable. The promise was commercially attractive terms. In other words, Russia wanted to give the message that it was willing to use force to keep its influence, but cooperative countries would benefit. In 2009, Russia told the Azerbaijani government that it would be willing to purchase all its gas production at European “net back” prices, the sales price in Europe, minus transportation charges, which was much higher than what Turkey was paying for gas at the time. In 2009, the Azerbaijani government agreed to export a small quantity of gas, 0.5 billion cubic meters a year, through Gazprom’s networks.36

The Azeri decision to export small quantities through Russia can also be seen as a way for the Azerbaijan government to force Turkey to accept a new pricing deal. Under the original contract for the BTE pipeline, Turkey was paying US$100 to US$120 per thousand cubic meters, much lower than contracted prices in Europe. In May 2010, it was reported that Turkey agreed to pay US$220 per thousand cubic meters.37 This price is very similar to US$230 per thousand cubic meters agreed between Russia and Ukraine in April 2010, a price that was considered roughly equal to the price charged in Europe, minus the extra transportation charges.38 Therefore, by agreeing to export gas to Russia, Azerbaijan was able to both mollify the Russians and force Turkey to agree to pay European contract prices for its gas.

The Azeri situation must be taken into consideration by the Turkish government as a challenge to its energy security goals. And suppliers apart from Azerbaijan will be required for Turkey to become an energy hub. There are realistically two countries: Iran and Turkmenistan. At present, Turkmenistan, which has perhaps the fifth largest gas reserves in the world is diversifying from its traditional export route through Russia by building pipelines to China and Iran, as well as agreeing to look into building a pipeline across the Caspian to supply the Nabucco pipeline and continuing to export through Russia. By diversifying the countries it supplies, Turkmenistan would be able to balance Russian influence with Chinese, while keeping on good terms with the West.

Iran has the third largest gas reserves in the world, according to BP, which, due to US sanctions, have not been largely exploited. Also, since 2001 Iran has been exporting gas to Turkey. The Iranian government has offered TPAO (Türkiye Petrolleri Anonim Ortaklığı, the Turkish state-owned oil and gas company) development concession on its South Pars gas field, one of the largest in the world, to gain support from Turkey to oppose the US sanctions.39 Iraq could be another supplier, and oil is intermittently shipped via pipeline through Turkey to the port of Ceyhan. However, the pipelines in Iraq are subject to numerous attacks, and until the situation in that country is resolved, the required investment in pipeline construction and developing the resource base is unlikely to be forthcoming.

The development of Turkey into an energy hub would reinforce two major policy objectives of the government: ensuring the security of supply and increasing connections with its neighbors and the EU

To sum up the challenges Turkey faces in becoming an energy hub, the primary goal of all these exporting and importing countries is to avoid reliance on Russia and to pursue their own particular political goals. Azerbaijan agrees both to send gas to Russia and to Turkey, which avoids conflict and gives it a good bargaining position for prices; Turkmenistan wants to have all the big regional powers reliant on its gas; Austria agrees to participate in both the South Stream and the Nabucco projects. Even Turkey, while primarily supporting the Nabucco project, has agreed to let South Stream be developed in its territorial waters.40 The Turkish government is also continuing to negotiate a contract for Russia to develop a nuclear power plant in Mersin, further drawing in Russian involvement in the energy sector.41 Only Iran seems to have a single objective: Undercut US sanctions and develop its own gas fields to increase revenue. All of these arrangements are also affected by the current low price in natural gas, due to reduced demand because of the recession and an increase in US unconventional shale gas production.42 As a result it is unclear if there will be sufficient demand, never mind supply, to develop all the proposed projects.

At the moment there are competing projects – South Stream and Nabucco primarily – and the Turkish government appears to be supporting both. Azerbaijan and some EU member states and companies are also following this strategy. There is a lack of coherent strategy on the part of Turkey as the government is looking at short-term objectives such as trying to increase the speed of EU accession negotiations, negotiate a low price for Azerbaijani gas, and to keep on good relations with Russia. The same considerations can be seen in terms of nuclear power: the Turkish government is having Russia develop one plant, and South Korea another. This lack of a coherent long-term strategy means that the Turkish government is primarily responding to events instead of influencing them. The development of Turkey into an energy hub would reinforce two major policy objectives of the government: ensuring the security of supply and increasing connections with its neighbors and the EU. Without a coherent strategy these goals will be difficult to attain.

Conclusions

The threat of declining energy production combined with increasing competition over energy resources has made energy one of the basic issues in international actors’ geopolitical considerations. In the post-Cold War era, with the rise of newly industrialized capitalist states like China and India, a multi-polar and energy-oriented geopolitics has emerged. Within the new energy geopolitics, China and India have grown into one of the biggest consumers of Eurasian energy resources. Hence, the intense competition in the global energy market has caused a decrease in the share of the US and the EU. Furthermore, this intense competition has given energy-rich states strategic and geopolitical leverage to become the superpowers of the new world order. The rise of Russia and Iran is a good illustration of this shift toward new, energy-oriented geopolitics. Besides the energy-rich regional powers who seek strategic leverage over global superpowers, the new energy geopolitics has created wider room to maneuver for the states that lie at the center of the supply and demand routes for oil and gas. Within this context, Turkey has been trying to exploit its new position as an energy hub in the new energy geopolitics to guarantee the security of supply, particularly for gas, by enjoying the offtake rights of transit states. Aside from these resource-led reasons, being an energy hub could provide Turkey with strategic advantage to gain political influence in Europe and in the region. The question is, what will Turkey do next with this great potential?

Endnotes

- Oyvind Osterud, “The Uses and Abuses of Geopolitics,” Journal of Peace Research, Vol.25, No.2, (1988), p.191.

- Paul Kenedy, The Rise and Fall of the Great Powers: Economic Change and Military Conflict from 1500 to 2000 (New York: Vintage Books, 1987), p.151-215.

- Philippe Le Billon, “The Geopolitical Economy of ‘Resource Wars’,” Geopolitics, Vol.9, No.1, (2004), p. 1.

- Halford J. Mackinder, Democratic Ideals and Reality (New York: W.W. Norton, 1962 [1919]), p. 150.

- Zbigniew Brzezinski, The Grand Chessboard: American Primacy and Its Geostrategic Imperatives (New York: Basic Books, 1997), p. 124,148.

- Deniz Ülke Arıboğan, Geleceğin Haritası (Istanbul: Profil Yayıncılık, 2008), pp. 151-153.

- Mert Bilgin “Energy Supply Security Problems and Alternative Solutions”, Working Paper, Turkey’s Strategic Vision in 2023 Project (Istanbul: TASAM, 2008).

- D. Ülke Arıboğan and Mert Bilgin “New Energy Order Politics Neopolitics: From Geopolitics to Energeopolitics,” Uluslararası İlişkiler, Vol. 5, No. 20, p. 119.

- Paul Roberts, The End of Oil (New York: Mariner Book, 2005), p. 285.

- Michael T. Klare, Rising Powers, Shrinking Planet: The New Geopolitics of Energy (New York: Metropolitan Books, 2008).

- Abbas Maleki “Energy Supply and Demand in Eurasia: Cooperation between EU and Iran,” The China and Eurasia Forum Quarterly, Vol. 5, No. 4, (2007), p. 106.

- Bezen Balamir Coşkun, “Global Energy Geopolitics and Iran,” Uluslararası İlişkiler, Vol. 5, No. 20, (2009), p. 186.

- Rafael Kandiyoti, Pipelines: Flowing Oil and Crude Politics (London: IB Tauris, 2008), p. xiii.

- D. Ülke Arıboğan and Mert Bilgin “New Energy Order Politics Neopolitics: From Geopolitics to Energeopolitics,” Uluslararası İlişkiler, Vol. 5, No. 20, p. 127.

- Ministry of Energy and Natural Resources, the Republic of Turkey, “Presentation by the Minister,” Strategic Plan: 2010-2014, April 15, 2010. Available at www.enerji.gov.tr.

- Eurostat.

- Ministry of Foreign Affairs, Turkey’s Energy Strategy, January 2009. Available at www.mfa.gov.tr. For an evaluation, see: Saban Kardas, “Turkey Unleashes New Energy Strategy Plan,” Eurasia Daily Monitor, Vol. 7, No.83, April 29, 2010.

- Eurostat and Ministry of Energy and Natural Resources, Strategic Plan: 2010-2014.

- Eurostat.

- DTM, Foreign Trade Outlook 2008. Available at www.dtm.gov.tr.

- Gareth Winrow, Problems and Prospects for the “Fourth Corridor”, June 2009. Oxford Institute for Energy Studies, NG30.

- Eurostat.

- DTM, Foreign Trade Outlook 2008.

- TEIAS, Istatiskleri 2008. Available at <www.teias.gov.tr/istatistik2008/index.htm>.

- Ibid.

- TEIAS, Turkish Electrical Energy 10-Year Generation Capacity Forecast, June 2009. Available at www.teias.gov.tr.

- “Turkish-Russian Ties Evolve into Strategic Partnership,” Today’s Zaman, May 13, 2010.

- BOTAS.

- Ministry of Energy and Natural Resources, Strategic Plan: 2010-2014.

- “Turkish Energy Minister Enthusiastic About Black Sea Exploration,” Turkish Daily News, January 3, 2010.

- Dieter Helm, “EU Energy and Environmental Policy: Options for the Future,” in L. Tsoukalis, ed., The EU in a World of Transition. (Policy Network: 2009).

- Winrow, Problems and Prospects for the “Fourth Corridor”.

- See the website of IGI Poseidon, the joint company developing the pipeline. Available at www.igi-poseidon.com.

- See the Nabucco website at www.nabucco-pipeline.com.

- See website at south-stream.info.

- “Azerbaijan Backs Gas Exports via Three Main Routes,” News.AZ, April 15, 2010.

- “Turkish PM Expected in Baku,” News.AZ, May 4, 2010.

- Edward Chow, “Bad Deal All Around,” Kyiv Post, April 22, 2010.

- “Iran Offers Turkey Natural Gas Concessions,” UPI, April 27, 2010.

- Lyubov Pronina and Ali Berat Meric, “Turkey Offers Route for Gazprom’s South Stream Gas Pipeline,” Bloomberg, August 6, 2009.

- “Turkish-Russian Ties Evolve into Strategic Partnership,” Today’s Zaman, May 13, 2010.

- Guy Dinmore and Heba Saleh, “Gas Plans Clouded by Demand Doubts,” Financial Times, April 28, 2010; Christian Lowe and Thomas Pfeiffer, “World’s Biggest Gas Exporters Meet to Cut Glut,” Reuters, April 19, 2010.