Introduction

After the recent discoveries of natural gas resources in the Eastern Mediterranean (Levant) basin, geopolitics and natural gas related commercialization efforts have become top agenda items. However, technical, economic and political facts illustrate that without regional stability, cooperation, and the contributions of global and regional actors, the exploitation of the isolated, small-scale reservoirs of EastMed does not seem viable. Therefore, one can see a number of regional cooperation efforts cropping up between Israel, Cyprus, Egypt and Greece which could help to realize the first phase of exportation of EastMed gas into world markets. Ankara, too, aims to become a robust gas transit center and key gas trade hub. However, Turkey has political conflicts with Greece, Israel and the Greek Cyprus Administration (GCA) that hinder its ability to be the most feasible route for exportation via pipelines. Nevertheless, the gigantic reserves of EastMed would require a pipeline system to commercialize and export the gas, and pipeline options without Turkey are considered politically possible but economically unfeasible. Once the political issues are resolved, Turkey shall be the main market for the new EastMed Gas Corridor for integrated gas resources. The EastMed Turkey European Gas Project thus may represent the sole win-win for regional resources and an instrument of solution for the EastMed’s regional conflicts.

The emergence of the EastMed as a new upstream player in the world market

Turkey has the largest natural gas market in the EastMed vicinity, and is located in the middle of natural gas-rich regions (47.8 billion cubic meters (BCM) natural gas consumption with 5.7 percent annual increment in 2014).1 However, Turkey has a robust growing economy that depends almost entirely on energy imports (97.15 percent of the gas demand was imported in 2013).2 In order to meet the demands of Turkish industry, gas is the top “to do list” item for the Turkish government. Accessing, Acquisition and Affordability are the “triple A” for sustaining a feasible natural gas supply in response to roaring domestic demand.3 Ankara’s primary concern is to satisfy Turkey’s own energy needs in the most cost-effective way; its ambitions to become an energy corridor and hub are secondary.4 Regardless of which issue takes precedence, however, Turkey’s need to clear up long-standing conflicts with the other players in the EastMed region has become immanent.

The Cyprus issue has been the most problematic issue of Turkey’s foreign affairs since the country’s establishment in 1923. Turkey’s increasing problems with its EastMed neighbors over the last five years have limited Turkey’s geopolitical capacity to connect EastMed resources to the Turkish market. Despite the political obstacles, however, the exportation of EastMed gas via Turkey is commercially appealing and is still being discussed among gas business circles.

The geopolitical importance of the EastMed basin has increased in recent years due to the large gas findings in the region. This has resulted in the emergence of the EastMed as a new upstream player in the world market, and with that shift has come both a revival of old conflict zones, and the potential for new and unusual alliances. A rising demand for democracy, civilian uprisings for freedom and the soft-power efforts of global actors indicate that tension will not be an option for the region in the near term. This paper will focus on the natural gas export options of the EastMed and will examine some options for the exportation of the EastMed resources. This paper also proposes an optimum “integrated model” for a Turkish solution, a model supported by a brief overview of the relevant technical, commercial and geopolitical facts and figures.

EastMed Gas Resources and Upstream History

The U.S. Geological Survey (USGS) estimated that there are 1.7 billion barrels of recoverable oil and 3.4 trillion cubic meters (TCM) of recoverable gas in the Levant basin as of 2010.5 USGS also illustrated the prospects of 1.8 billion barrels of oil, 6.2 TCM of gas, and six billion barrels of condensate in the Nile Delta Province.6 Furthermore, numerous reports indicate the world-class undiscovered gas potential of the southern Cretan basin, the deep Herodotus basin and the Ridge prospects.7These landmark announcements for the Levant basins were solid signals for the pioneer companies of the “Caspian-class or even larger” business development rush and the competition with Northern Iraq and Sub-Saharan offshore resources. EastMed gas could be supplied to meet the rising Middle East gas demand, the exploding Egyptian consumption, the fast-growing Turkish economy, the European Union (EU), and even the broader global demand in the form of Liquefied Natural Gas (LNG).

The history of the exploration efforts of EastMed is older than the USGS estimate. The newer, core developments which have attracted global interest are primarily due to Israeli efforts. Initial small gas discoveries were made in the Noah offshore field by the Tethys Sea Partnership in June 1999 and the Mari-B field with 45 BCM reserves in February 2000. The field supplied gas to the Israel Electricity Company starting in 2004.8

Meanwhile, on the Palestinian side, the BG Group estimated that Gaza Marine-one and -two wells contained 28 BCM of natural gas at 36 km offshore Gaza in 2000.9 However, BG withdrew from the negotiations in 2007. It is not clear when the Palestinian gas could be exploited, but the finding was as important, as it was yet another proof of the potential for a working petroleum system in the basin.

However, the first game-changing offshore find was the 283 BCM of gas discovered at the Tamar site in January 2009 by the consortium of Noble Energy of the U.S., and Avner, Delek Drilling, and Isramco Negev of Israel. In March 2009, the Tamar partners also discovered another small gas reservoir at the Dalit site with seven to eight BCM of gas. Delek has estimated that Tamar and Dalit contain a quantity sufficient to meet Israel’s natural gas needs for over 20 years.10 Tamar was commissioned and started to supply gas to Israel in March 2013.

The next major discovery in the region (as well as the largest to date) was in October 2010: A giant field in the Leviathan blocks which was comprised of 491 BCM of gas reserves11 (updated to 623 BCM gas and 39.4 million barrels of condensate after further analysis in July 2014).12 The shareholders of the consortium are Noble, Delek, Avner and Ratio Oil. A 25 percent farm-in option of Australian LNG-player Woodside Petroleum at a cost of 2.7 billion U.S.$ (bnU.S.$) failed in May 2014. Another recent discovery is the Karish prospect of the Delek and Avner partnership on 22 May 2013. The field is located in the Alon-C license near to the conflict zone with Lebanon. The reserve has approximately 50 BCM.13 The field also contains 13 million barrel of condensate.

On 4 December 2013, Noble announced another discovery of a small reserve containing 20 BCM gas 13 km southwest of the Tamar field. Finally, the latest announcement (December 2014) highlighted the third biggest field, containing 89 BCM of gas, the Royee field 150 km off Israel’s coast.14 The license is owned by a consortium led by Ratio. Smaller discoveries include the Dolphin, Yam Tetis, Shimshon and Tanin (34 BCM) fields; the Pelagic field is estimated to hold 190 BCM but needs further confirmation through appraisal drillings.15 The EastMed Levant basin reached around 1.2 TCM recoverable gas reserves with these latest discoveries. According to Israeli sources, the fields are mainly gas-prone, and oil potential in the system is low.16 The same sources also stated that there are strong indicators of deeper gas reservoirs and deep oil.

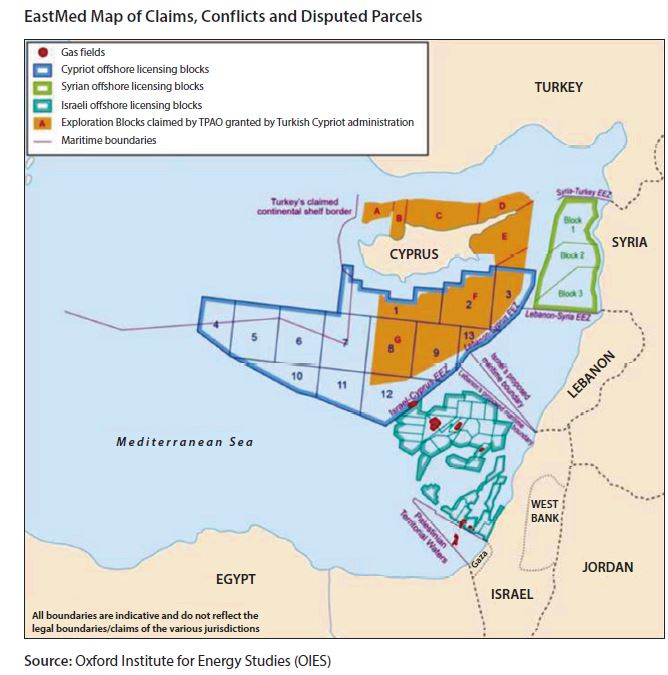

In parallel with the Israeli developments, at the north of the basin, the GCA-initiated exploration efforts in 13 parceled blocks of the so-called Cyprus Exclusive Economic Zone (“EEZ”) was based on delineation agreements reached between 2003 and 2007 with Egypt and Lebanon, which have not yet been ratified, In February 2007, Noble was awarded a license in Block 12. With the EEZ agreement signed with Israel in December 2010, the first drilling in the block began on 20 September 2011. In December 2011, Noble announced 198 BCM of gas discoveries in Aphrodite field.17 Noble’s partner, Delek, further estimated the reserves as being approximately 147 BCM.18 The discovery in Block 12, together with the large finds in the neighboring Israeli Leviathan block, significantly raised interest for the second Southern Cyprus offshore licensing round, launched on 11 February 2012. Despite protestations from Turkey, the round attracted 15 strong bidders such as Total, ENI, Gazprombank, Petronas and Kogas.19 ENI and Kogas were invited to contract for Blocks 2, 3 and 9 and Total by itself for Blocks 10 and 11.

There is strong concern in Arab countries about Israeli policies aimed at penetrating the Arab energy sector

In the northeast, Lebanon’s government announced that there are up to 2.69 TCM of natural gas and 750 million barrel of oil resources in its EEZ. Preliminary seismic data estimates the amount of recoverable gas to be 708 BCM.20 The government announced that the deadline to submit bids for the first licensing round had been re-extended from 14 August 2014 to early 2015.

Deep exploration plans on older strata of the Levant basin, the deep Nile campaign, the Lebanon tender progress, offshore Antalya developments and prospects on the adjacent Herodotus, Cretan and M. Ridge basins offer improvements for the commercialization of the EastMed basin. The expensive Floating Production and Storage Offloading Platform (FPSO) and/or Floating LNG (FLNG) terminals will likely represent the introduction of new, cutting-edge upstream technology in EastMed. Noble is the pioneering oil company and front-runner in the EastMed.

TPAO started to explore EastMed basins off of Turkey. Initially there was an exploration and development agreement with Shell signed in 23 November 2011.21 The consortium will explore the offshore Antalya bay in three licenses. Shell is responsible for all of the costs for this campaign. However, there have been no further announcements of activities as of early 2015.

As a summary, the EastMed basin covers a considerable amount of discovered, recoverable gas resources in the Israeli and Gaza EEZs (nearly 1.2 TCM), discovered marginal gas volume (150 or 200 BCM) around Cyprus, and more prospects, as well as possible discoveries in Lebanese territorial waters. The basin is thus comparable with the Caspian Sea. Despite this massive potential, however, the region’s many small, isolated and discrete fields have resulted in big technical and economic challenges for commercialization, alongside the region’s critical and historical conflicts.

Ongoing EastMed Geopolitics and Gas Commercialization Efforts

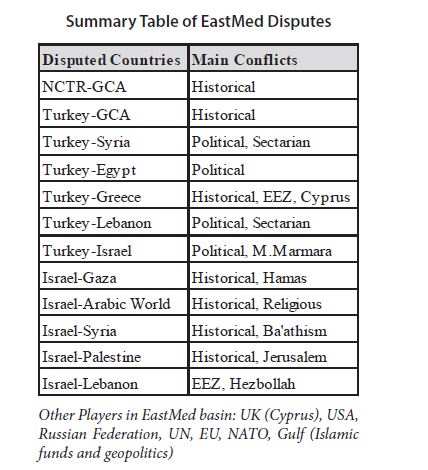

The EastMed basin has been defined as a new gas frontier. The discoveries are potentially so important that the economic map and geopolitical pacts of the region are already being redrawn.22 However, many chronic setbacks remain– mainly the delamination of EEZ’s and sovereignty disputes– among the regional countries. Complex conflicts and geopolitical tensions have to be resolved or mitigated before implementation of any EastMed gas scenario.23 The Turkish side is located at the center of the disputes and the geopolitical scheme to harvest the region’s natural gas thus fits into a wider collaboration effort involving the defense sector. For instance, Israel, Greece (plus GCA) and the U.S. currently conduct annual or seasonal military exercises to simulate the defense of seaborne gas drilling installations in EastMed, such as Operation Noble Dina, which was first inaugurated in 2011.24 The positions of the regional actors, investors, powers, buyers and organizations should all be aligned in the interest of commercial benefit in order for further proceedings to occur.

Summary Table of EastMed Disputes

Compiled by the authors on collected data from open media sources listed in the paper

Israel is the front-runner of the EastMed gas operations. The Israeli government decided on 13 June 2013 that only 40 percent of the reserves, or over 450 BCM, could be allocated for exportation.25 The Leviathan project is designated primarily for export, however, because the Tamar reservoir is estimated to be enough to supply all of Israel’s domestic gas needs in the coming years. Israeli sources predict that the required investment by Israel into the gas sector by 2020 will be almost 40 bn USD.26 Noble also stated that each year that Leviathan is not developed costs nearly three bn USD.27

Integrated pipelines via conventional FPSO or FLNG are the two main candidates for the production model of the Leviathan field. The first stage of Leviathan would cost six to eight bn USD for a FPSO facility with a capacity of 16 BCM per annum (“BCM/y”). On the other hand, Israeli authorities pointed out that “to establish an onshore LNG liquefaction plant there needs to be a minimum 280-300 BCM of recoverable gas reserves.”28 Moreover, neither the EastMed shores of Israel nor the coast of the Red Sea are suitable for an onshore LNG terminal from environmental and technical perspectives. Therefore, the “FPSO plus new onshore LNG liquefaction facility” option does not seem viable.

Indeed, Leviathan partners recently delivered their initial development plan to the Israeli authorities.29 Partners would sanction the project in Q1-2015 and it would be in operation by the early 2020s with a gas production rate of 16 BCM/y by FPSO. If Noble decides to invest in FPSO for the Aphrodite and Leviathan fields, Noble will get the first production in 2021 at the earliest.30 This effort is also part of the challenges faced due to the limit on Israeli gas exports.

The later development stage is expected to include the expensive but flexible FLNG option with a five BCM/y capacity. The first giant FLNG plant, the 600K-ton Prelude, will be commissioned in Australia in late 2017. The capital and operational expenditures of the FLNG plant are extremely high (10.8 to 12.6 bn USD, or around two bn USD/ton).31 Hence, FLNG investment on small and isolated EastMed reservoirs by pioneer companies is not affordable, especially in a plunged oil price environment. Finally, after the failed Woodside investment, the FLNG option has been relegated to the lowest option status. Another option for the later stage would be the construction of a pipeline to Cyprus, where the government plans to build an onshore LNG export facility for supplying larger volumes to secure investments. However, this project risks not being supported by lenders, who forecast a new LNG-glut era and plunging prices next term.

Cost-efficient options are thus the main target for the realization of the initial stage of EastMed gas exportation. The strongest option is the transmission of gas from Israel to the existing but unutilized LNG terminals in Egypt via offshore pipelines. The Leviathan field is located at the midpoint between Egypt and Turkey (500 km from each). However, as the pipeline to be built to Turkey needs deeper crossings, its cost would skyrocket to four bn USD32. Conversely, a pipeline to Egypt would pass through a shallower area and its cost would be around two bn USD.

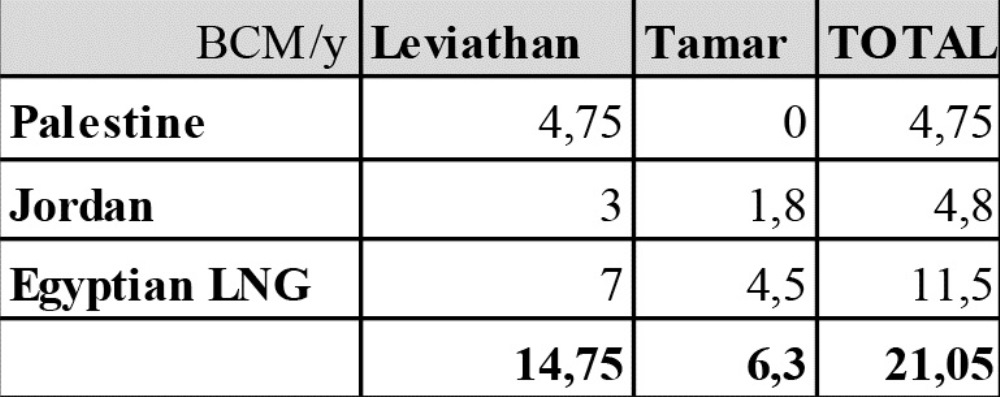

Several non-binding Letters of Intent (LoIs)/Memorandum of Understandings (MoUs) have been signed for initial export markets. The first effort toward the commercialization of the EastMed gas was a LoI signed in October 2013 to sell five BCM of Tamar gas to Egypt’s Dolphinus Holding over a three-year period through the existing offshore Eastern Mediterranean Gas Pipeline which once transported Egyptian gas to Israel.33 In January 2014, the Leviathan partners signed another LoI to sell 4.75 BCM/y of gas to the Palestine Power Generation Co over a 20-year period, for a cost of 1.2 bn USD for the gasification of a plant to be built in the West Bank town of Jenin.34 In February 2014, the Tamar partners signed a 500 million USD deal to provide 1.8 BCM/y of gas to the Jordanian firms Arab Potash and Jordan Bromine over 15 years, beginning in 2016, which would power their Dead Sea facilities.35 In May 2014, Tamar partners signed a new LoI to supply 4.5 BCM/y of natural gas for 15 years to the Spanish Union Fenosa Gas for its LNG liquefaction facility at Damietta.

In June 2014, the Leviathan partners signed a 30 bn USD deal in a LoI with BG to supply seven BCM/y of natural gas over 15 years to BG’s LNG liquefaction facility at Idku with a 7.2 million ton per annum (MTPA) liquefaction capacity with similar contingencies.36 BG will decide very soon on either the approval of this purchase of Leviathan gas or instead securing BP’s recent Nile basin Salamat gas discovery.37 The combined capacity of the two semi-idle LNG liquefaction plants (Damietta and Idku) is 12.2 MTPA. Recently, Noble also announced another LoI to supply gas from the Leviathan field to Jordan’s NEPCO on September 3, 2014.38 Based on the terms of the 15 bn USD value of the LoI, Leviathan partners will supply nearly 45 BCM of natural gas from the field over a 15-year period.

However, there is strong concern in Arab countries about Israeli policies aimed at penetrating the Arab energy sector.39 It is noteworthy that the Jordanian parliament has recently discussed and advised that the importation of gas from Israel should not be approved.40 In parallel, Egypt is negotiating a possible gas import deal with GCA through a pipeline or the importation of LNG from Algeria combined with increased domestic output.41

Long-term Non-binding LoI Agreements on Israeli Gas

Compiled by the authors on collected data from open media sources listed in the paper

The total volume of long-term gas deals on the Israeli sector based on LoIs is 21.05 BCM/y if all deals are exercised. There is room for an additional 10 BCM/y capacity which shall be mainly exercised by Leviathan incremental volumes.

It is crystal clear that the island of Cyprus is the geopolitical hotspot of the EastMed

The recent decision by Israel’s anti-trust authority is highly critical in that it may withdraw an arrangement permitting Noble and Delek to develop the Leviathan field by branding them as a cartel.42 That decision forces those two companies to unbundle their activities,43 and could result in a transition from Israel to Cyprus as the new center of gravity in the EastMed energy game.44 The anti-trust authority’s decision also poses a threat for the Noble-Delek-owned Aphrodite development plan.45 Noble, which had previously lost in farm-out rounds against Russian and Australian firms, has entered advanced negotiations with an Italian firm (Edison) to buy the Karish field, which is close to Lebanese waters, in addition to the adjacent Tanin field and part of the nearby Leviathan field.46 If a final agreement is reached, Noble will secure the necessary liquidity to start development of Leviathan, and to meet the demand of the Israeli authority.

On the other hand, the main issue will be how to mitigate the broken Turkish-Israeli relationship, which has deteriorated dramatically in the last few years. During the commercial negotiation rounds in late 2012 to early 2013, selected private Turkish companies and Leviathan’s partners discussed the terms and conditions of the business.47 Any pipeline from Israel to Turkey would run through Cyprus or Cyprus’s so-called EEZ. Although most of the commercial terms of reference were agreed upon, the negotiations were not concluded due to rising political tensions.

It is crystal clear that the island of Cyprus is the geopolitical hotspot of the EastMed. The sole exploration efforts of GCA and the discovery in the Aphrodite structure of Block 12 resulted in strong objections from Turkey and the Turkish Republic of Northern Cyprus (TRNC). Turkey stated that the partitioning of GCA’s EEZ is unacceptable and overlaps with Turkey’s EEZ, and that the findings in the EEZ of the island of Cyprus should be shared by all nations in Cyprus. The Turkish Prime Minister recently emphasized in Athens on 6 December 2014 that any delimitation of the Mediterranean between Egypt and Greece would also be not acceptable.48 Dramatically, the new Greek government in turn also criticized and warned Turkey over its efforts in the Mediterranean.49

Two points are critical in GCA geopolitics: “First, absent from the list of successful bidders during tender were the five blocks which Turkey claims partly fall within its continental shelf, although bids were reportedly also received for some of these blocks.50 Second, all the companies chosen were very large oil and gas companies from countries with significant military strength.”51 The GCA’s bolstering of its ties with Israel in the past three years can also be interpreted in this light. Furthermore, the GCA has signed MoUs with ENI, Total, and Noble for onshore LNG export terminals and FLNG feasibilities, and is involved in ongoing discussion regarding a 25 percent shareholder option for the Chinese CNOOC to invest in the Aphrodite parcel.

Both pipelines and conversion to LNG have been considered as options for GCA resources. However, block 9 may be dry after the failed Onasagoras prospect and Block 12 may not hold additional reserves other than the Aphrodite structure.52 The gas of Aphrodite, however, is enough to materialize a pipeline.

Based on the same source, “anywhere from 55-83 BCM is sufficient to monetize a find using compressed natural gas (CNG) solutions and FLNG, requires between 83-111 BCM”. But most of the individual reservoirs in the EastMed basin do not contain enough gas to fulfill these options on their own, and need to tie in to a gas gathering center for build-up. This is why Noble officials were looking at pipelines as their top option, and FLNG and CNG as secondary alternatives. Indeed, a comprehensive analysis53 illustrates that a pipeline to Turkey is the best option as by far it offers the lowest cost and the highest revenue.

Egypt and the GCA have sped up negotiations to implement the pipeline transport of gas to Egypt for LNG exportation and domestic demand.54 Moreover, the Egyptian government recently declared that Egypt is ready to book all output of the Aphrodite field.55 Egypt, Greece and the GCA governments also announced the “Cairo Declaration” from the highest level on 8 November.56 The GCA offered three models: selling gas directly to the Egyptian government for their domestic market, selling gas to owners of terminals, or utilizing LNG facilities and marketing gas by Aphrodite partners.57 However, the latest dry well of ENI-Kogas on the Onasagoras structure of Block Nine after an expenditure of nearly 100 million USD58 is a real disappointment for the gas export plans of the GCA.59 Nonetheless, the biggest prospect (Amathus) is located at the north of the Onasagoras and it may be as large as Leviathan at nearly 538.1 BCM reserve potential.60 Indeed, Noble, the operator in Block 12, is anticipated to drill another exploration well in 2015; ENI launched a four-well drilling program at Block 9, and Total (if it does not cancel all exploration efforts,61 will start drilling in Blocks 10 and 11 in 2015.

On the onshore side, the GCA’s ambitious pipeline proposal, the “EastMed Pipeline,” lacks financial and technical viability. The cost of the pipeline running from Cyprus to Italy via Crete with a capacity of 28 BCM/y would be around 20 bn USD due to long, unstable and deep tectonic passages.62 However, the EU has agreed to grant three to four million EUR of support to the project for comprehensive feasibility studies.63 The EU further declared that the North-South interconnectors of the ambitious “Vertical Corridor” and EastMed Pipeline may have been integrated.64 Simultaneously, Israel also called on the EU to support an EastMed Pipeline project that would connect the natural gas fields in Israel and Cyprus to the EU via Greece. The Israeli government stressed the importance of the project in mid-November 2014.65

An innovative proposal from the SeaNG Alliance is based on an integrated and flexible CNG option for EastMed gas.66 The corporation pointed out that the players of EastMed have prevented huge pipeline and LNG investments due to several technical, economical and geopolitical facts. SeaNG Alliance offers clear netback for the CNG value chain from offshore Cyprus to Greece, in contrast to other options.

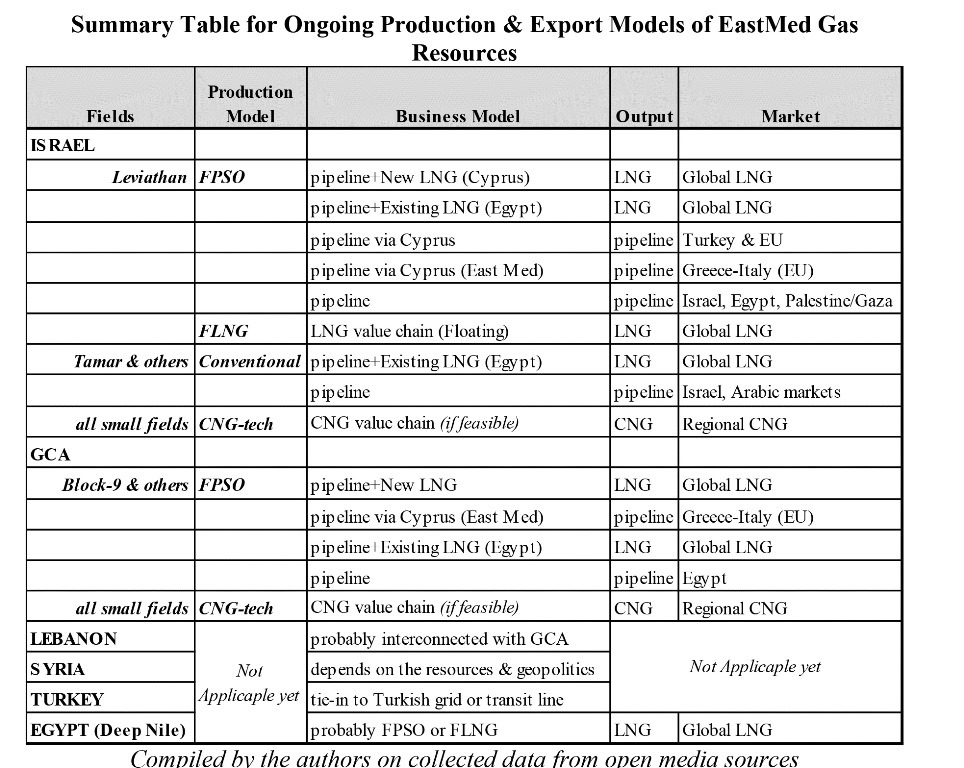

Global oil and gas markets have been deeply impacted by slumped oil price levels. Oil prices were recorded around 50 USD/barrel, and European and Asian spot LNG gas prices were around seven USD/MMBtu at the end of February 2015. These low prices have resulted in an “unaffordable” investment climate for geopolitically troubled waters such as those of the EastMed. As a consequence, various competitive upstream options have emerged to tap the EastMed resources for different markets:

Summary Table for Ongoing Production & Export Models of EastMed Gas Resources

The Optimum Solution for EastMed Gas: The Exportation Model through the Turkish Gas Market

The Turkish gas market represents one of the most liquid, mature, diversified and well-regulated markets of Europe. It is located between giant gas sources and the European market.67 The gas value chain is mainly dominated by BOTAŞ. Turkish gas consumption was recorded at 48.7 BCM/y in 2014, and is forecasted to be more than 60 BCM in 2020. Annual contract quantities of the binding agreements of Turkish companies are nearly 73 BCM/y of which 19.75 BCM/y volumes will be commissioned after 2016.68

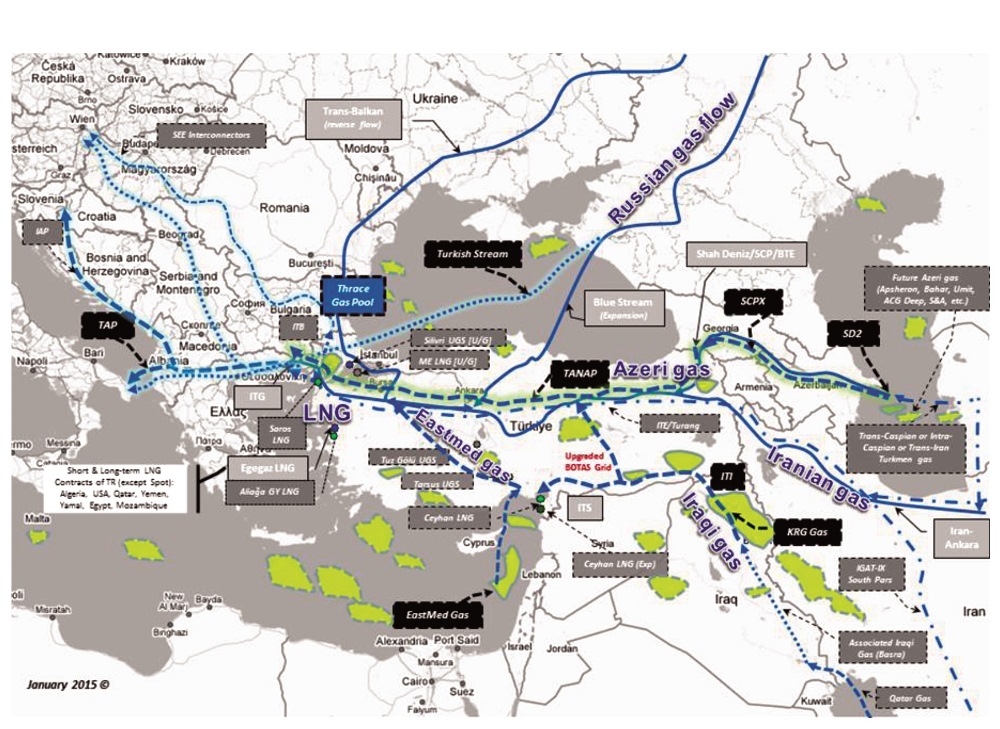

Turkey is the key market in the region, one of the main investors and a strong transit player for Caspian (Southern Gas Corridor), Russian (Blue and Turkish Streams) and future Iraqi gas sources. Strong growth potential, liberal market regulations, Turkey’s location as a transit corridor have resulted in a gas center and trading hub transformation.

Turkish Gas Master Plan and Anatolian Gas Center Projection to 2023

Compiled and modified by the authors

The Anatolian Gas Center69 represents an integrated Turkish gas market structure where cross-border gas pipelines, interconnected pipelines, national gas networks, LNG facilities, storages, and Turkey’s unconventional and offshore gas potentials are to be fully integrated. It is envisaged that more than 150 BCM/y volume gas could potentially be supplied, traded, transited, and stored along Anatolia by 2023.

It is widely accepted that the final shape of the “EastMed Gas Corridor” fully depends on geopolitics

The Thrace Gas Pool represents a gas trading hub sourced from the Gas Center and integrated with EU hubs. The Gas-Pool will be a benchmark, a spot balancing point and a gas store for hourly, daily and future/forward trading activities for the Southeastern Europe, Turkey and Middle East markets.

The Gas-Center and The Gas-Pool shall be optimized by ENTSO-G and ACER nomenclatures of the EU. However, it is widely accepted that the final shape of the “EastMed Gas Corridor” fully depends on geopolitics.70 The flexibility provided by LNG could also help EastMed actors overcome the uncertain outlook of the EU natural gas demand, thereby facilitating the necessary ongoing investments for the implementation of what could be defined as the “initial stage of the Corridor.”71 Most notably, a second stage, the construction of an EastMed main gas export pipeline, shall be constructed will be described and modeled below.

Given the knowledge contained in the above-mentioned sections and the defined facts: i) Without the contribution of Turkey, huge amounts of gas could not be exported easily; ii) Turkey seems the best and closest market for EastMed gas; iii) The so-called EastMed Pipeline to Greece and Italy is unaffordable; iv) Avoiding the cost-burden of FLNG and onshore LNG liquefaction investments is a must for a commercial model.

Therefore, several build-up stages shall be implemented respectively: 1) the gasification of the regional markets; 2) the integrated upstream development of the basin; 3) the exportation to/through Turkey (EastMed-Turkey-Europe Gas Project) and 4) the addition of neighbor basins and the production of deep layers of the EastMed basin.

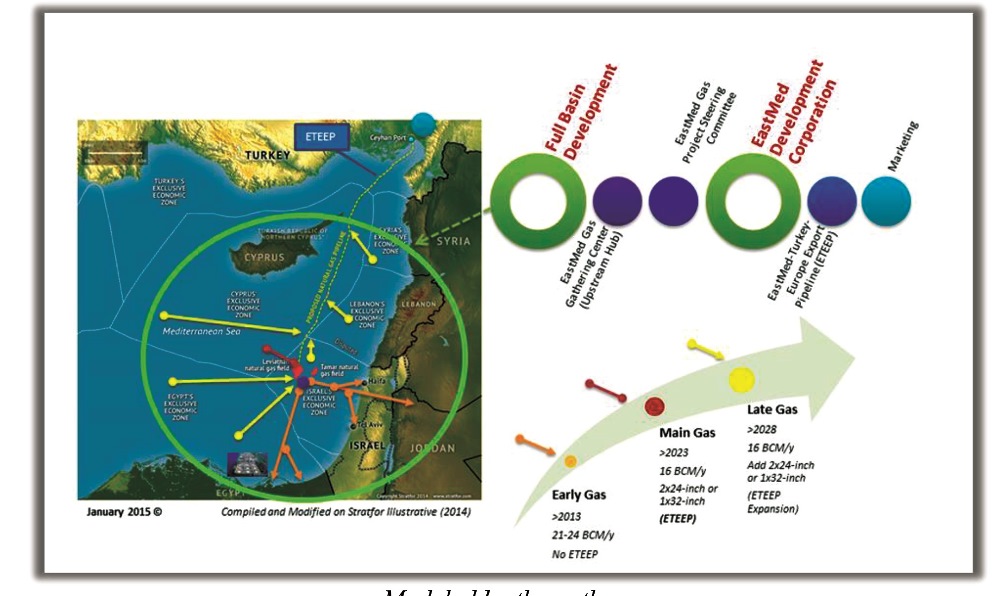

Hence, EastMed gas shall be developed for gasification of the region initially (i.e. Israel, Egypt, Jordan, Palestine, Gaza, Lebanon, and Cyprus Island) [Early Gas]. Exportation of the initial Leviathan gas and some Tamar gas via existing Egyptian LNG facilities is also applicable in Early Gas phase. EastMed Gas shall be subjected to the Full Basin Development of the Levant basin rather than through field-by-field or countrywide/EEZ-based solutions. The farm-in or merge and acquisition efforts of global investors (like ExxonMobil, Shell, etc.) and regional players (TPAO, BOTAŞ, DEPA, etc.) into fields of mid-level pioneers (Petronas, Kogas, Noble, even Total, ENI etc.) and national players (like Delek) are crucial for commercial and political stability. An EastMed Gas Gathering Center (“Upstream Hub”) shall be created after consolidation through integrated pipelines, as will a “seller and buyers’ club” bringing together the individual fields to create a gas pool and evacuation conduit of Main Gas.

An Upstream Hub shall be further integrated into The Gas-Center and then The Gas-Pool via cost-efficient, feasible and affordable ways [Main Gas]. The Main Gas phase shall be an extremely win-win model for the EastMed players. The gas of the EastMed basin (led by Leviathan) shall be gathered, collected and commercially developed in Full-Basin Development and Upstream Hub models. Corresponding countries and global investors shall be agreed upon to stabilize a political framework (via inter-governmental and post-governmental agreements) to implement a joint business plan for gasification of the region. A supreme governmental steering committee shall be established for securing regional stability and resolving (or freezing) the main disputes. This governmental umbrella for commercial initiation (The EastMed Gas Project Steering Committee) covers all players’ rights and positions. There shall be also an international lender model of the rejuvenated Caspian Development Corporation concept: The EastMed Development Corporation. The Corporation would be responsible for funding all Full-Basin Development, Upstream Hub and Transportation of the EastMed gas to the Mersin or Ceyhan landfalls via the Cyprus EEZ: EastMed-Turkey-Europe Export Pipeline.

The EastMed gas would be marketed to shippers of EU consumers via The Gas-Pool with high netback returns

Based on various media sources, the Israeli authorities have declared that Turkey is both the most commercial and the least political option.72 However, the partners of the Leviathan field invited selected Turkish companies (Turcas Petrol, Zorlu Group, Çalık Holding and Genel Energy) in early January 2014 to bid for seven to ten BCM/y gas through a pipeline.73 Former U.S. ambassador and board member of Turcas, Matthew Bryza announced on September 2013 that the company offered to finance the construction of a 410-km and 24-inch dual offshore pipeline (similar to Blue Stream) that would connect the Leviathan field to Ceyhan in Turkey via Cyprus or the EEZ of Cyprus.74 The pipeline would have a capacity of 16 BCM/y and a cost of 2.5 bn USD. Turcas reconfigured the project later and proposed a 24-inch dual pipeline with a 2.25 bn USD cost, 470-km in length to Mersin.75 Finally, Turcas cooperated with EnerjiSa and restated in mid-May 2014 that the pipeline may cost about two bn USD and could supply seven to ten BCM/y gas to Turkey via a nearly 500km undersea route.76

Zorlu, another Turkish conglomerate, is also focused on Leviathan. Zorlu Energy stated that an offshore pipeline between the Leviathan field to Ceyhan via the Cyprus EEZ would be 2.5 to three bn USD and has a capacity of ten BCM/y.77 The importer shall be ready to invest in the midstream part of the project, but upstream investment of Leviathan, around six bn USD, is due by Leviathan partners.

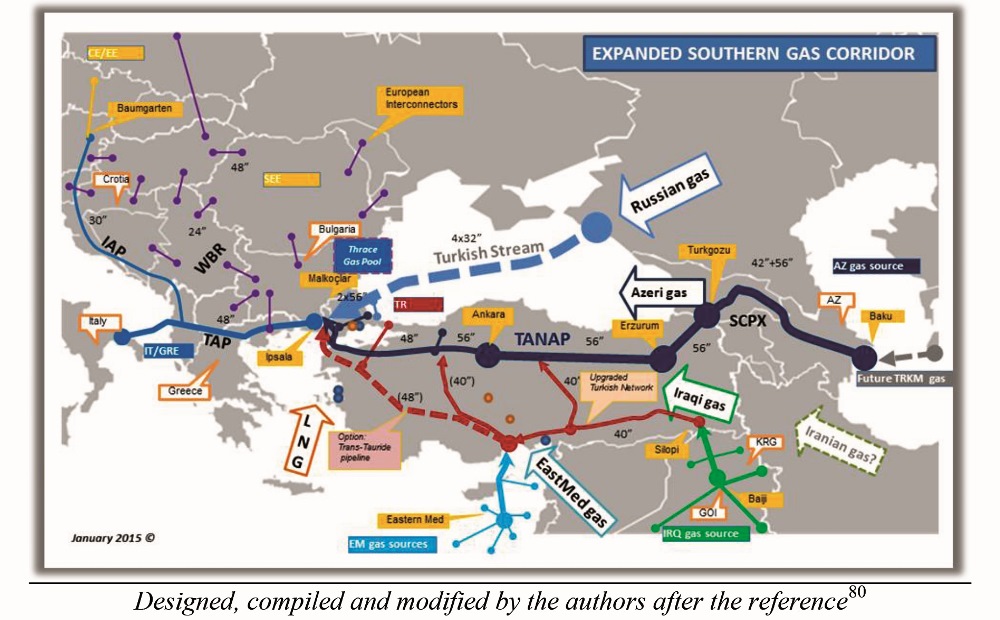

Integration of the gas to The Gas-Center and The Gas-Pool after landfall shall use either i) a BOTAŞ national gas network; ii) a physical swap, a BOTAŞ network or TANAP after Eskisehir as Expanded Southern Gas Corridor element; or iii) a new standalone transit pipeline (an onshore section of the Pipeline which may be implemented as Trans-Tauride concept together with Northern Iraqi gas).78 The “Expanded Southern Gas Corridor” covers an upgraded BOTAŞ network and TANAP. Caspian, Iraqi and EastMed gas shall dominate the growing Turkish market and further SEE and Italian markets via European pipelines (i.e. TAP) and interconnectors. An investment decision of 50 bn USD for the Southern Gas Corridor deal was secured by involving of Turkish state-owned energy companies on every stages of the project. For instance, without buying the gas of BOTAŞ from the Shah Deniz field, the netback and commercial model of the consortium would have collapsed. Turkey has already declared its readiness to exercise expansion of TANAP by growing volumes of Caspian, Iraqi and EastMed gas in AGC.

The EastMed gas would be marketed to shippers of EU consumers via The Gas-Pool with high netback returns. It is forecasted that due to the affordable upstream development cost, the Thrace delivery price of EastMed gas would be compatible with Russian gas.

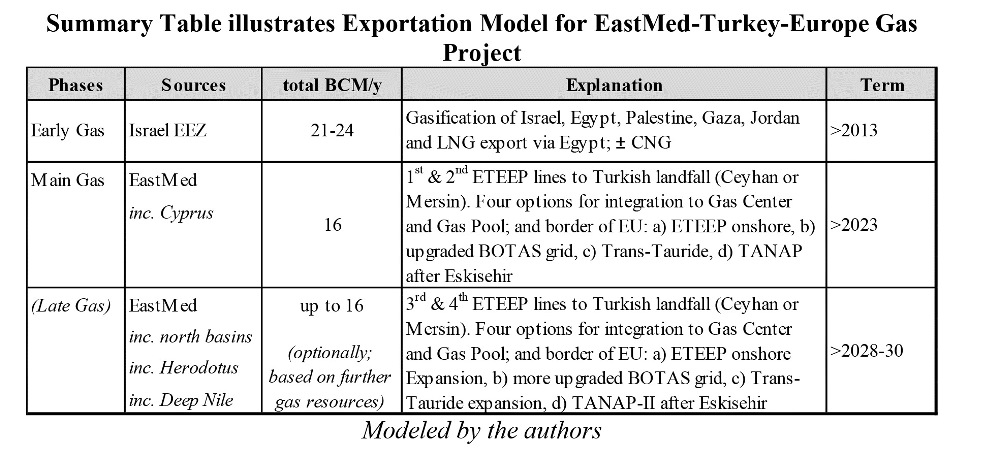

The project implementation schedule of The EastMed-Turkey-Europe Gas Project may be as follows: The Early Gas of the Project is also compatible with the ongoing commercialization efforts of nearly 21 BCM/y or slightly more volume of Israeli gas to Egypt, Egyptian LNG (export), Jordan, Palestine, Gaza and further Israeli demands. The binding contracts would be signed in H1-2015.

The FPSO of Leviathan will be commissioned in 2020. The Main Gas comprises formation of the Corridor through The Steering Committee, establishment of the Corporation, Upstream Hub and Full-Basin Development in 2015-16 as well as an investment decision on 2x24-inch Pipeline (or ultra-high-pressure 1x32-inch grid).

The second stage of the Leviathan field and the first stage of the Aphrodite field as well as integrated isolated reservoirs will supply an additional 16 BCM/y through the pipeline starting from 2023. The Leviathan FLNG plans shall be scrapped. Besides gas, an oil pipeline for deep oil or condensate pipeline would be also exercised in the Corridor projection. A further 16 BCM/y gas volumes from adjacent basins, the deep level of the basin, and the northern section would result from third or fourth 2x24-inch (or another 32-inch) pipeline(s) additions (optionally Late Gas) to the Pipeline.

Schematic Illustration Showing the Realization of the EastMed Gas Corridor and EastMed-Turkey-Europe Gas Project

Modeled by the authors

Most recently, U.S. Vice President Joe Biden officially proposed the construction of a gas pipeline from Israel, Egypt and Cyprus, via Turkey and Greece, to the European gas network. This proposal (which directly supports the model proposed above) has political gains at the same time: it isolates Egyptian gas from the Arab markets and links it to the Israeli exports. The goals also include the unification of the Republic of Cyprus, and the provision of new gas supplies via an expansion of the Southern Gas Corridor to Europe to halt its dependence on Russian gas.79

Schematic Illustration Showing Expansion of Southern Gas Corridor of EU

Discussion of the EastMed-Turkey-Europe Gas Project

Besides the major political challenging points, the technical potential and affordability of the Model can be further assessed by (i) forecasting the European Gas Supply Balance towards the 2020s, (ii) formulating a projection of Turkish gas market demand, (iii) analyzing the competition capability/available room for EastMed gas in European and Turkish markets, and (i) calculating the probable netback analysis for EastMed LNG supply to Asian markets.

All of the specific European gas scenarios indicate a strong supply gap and the need for new gas sources for the 2020s. Different reference sources (e.g. Statoil Energy Perspective 2040, BP Energy Outlook 2035, ExxonMobil Outlook 2040, etc.) indicate a huge supply gap of gas (and up to 300 BCM/y import, >200 BCM/y additional source needs) towards the period between 2020 and 2035 due to declining domestic production rather than the demand-growth rate. Moreover, although the renewable energy strategy and energy efficiency efforts of EU are still important (but marginal), natural gas, as the greenest of the fossil fuels, will maintain its pole position as the dominant energy fuel for Europe in the near future.

On the other hand, the most critical factor in the European gas environment could be the status of European Union-Russian Federation relations. Although there are severe historical, geopolitical, legal and intense economical disputes on the issue of oil-indexed Russian gas supply to Europe, the downstream European gas market has to get actually 70 percent or 85 percent of annual contracted Gazprom volumes rather than all. Therefore Europe has a chance to secure additional and more feasible alternative gas sources to replace 30 percent to 15 percent of its Long-Term Gazprom contracts. Finally, based on various Oxford Institute for Energy Studies (OIES) 2014 reports, the core OECD European countries’ contract obligation to Gazprom will be diminished to around 100 BCM/y towards the 2030s. Therefore, more new gas sources will be nominated for EU gas competition.

The main competitors of EastMed Gas for the EU can be simply analyzed and summarized in the following table:

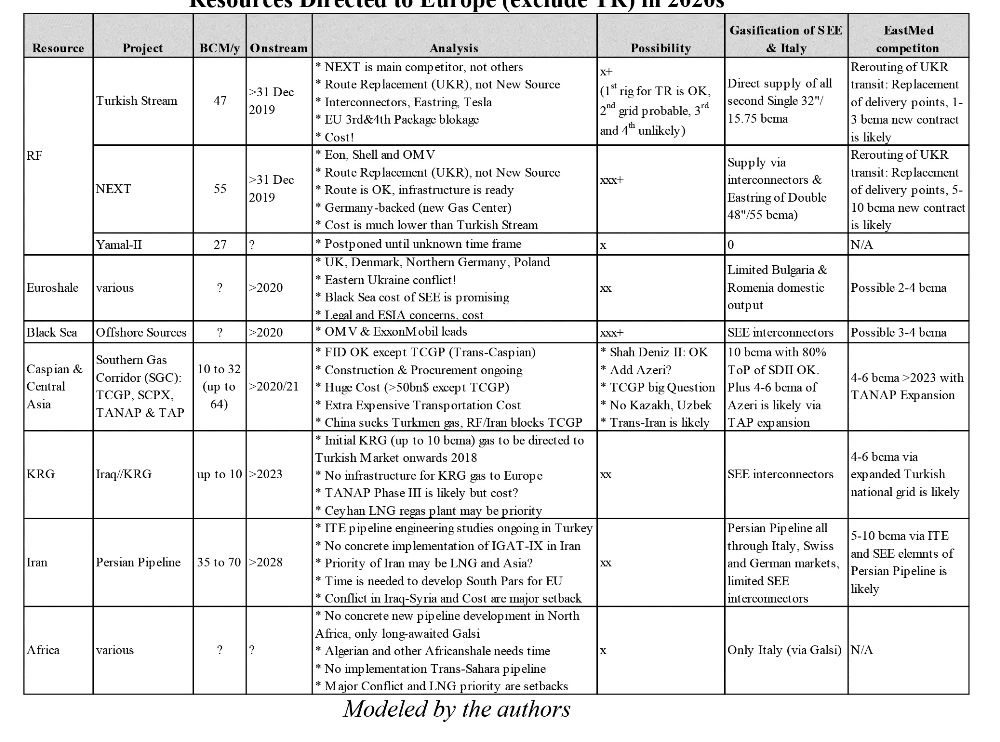

Simple Analysis on Main Gas-to-Gas Competition (except LNG) of EastMed Gas Resources Directed to Europe (exclude TR) in 2020s

Based on the figure, EastMed gas will enter gas-to-gas competition with around 100 BCM/y new gas sources plus additional LNG cargoes for fulfilling the European supply gap. According to recent news, the NEXT (Nord Stream Extension) Project will be more favorable than the massive transit Turkish Stream volumes or the marginal volumes of the second grid of Turkish Stream, the small increments of Iraq/KRG and the Caspian volumes, the small inputs of SEE domestic supplies, and the offshore and Euroshale gases which are the main nominees for the replacement of ongoing contracts with Russia. However, the NEXT Project is targeting the northern and central European market and does not have a direct effect on the Southern European market.

Therefore, the EastMed Main and Late Gas phases will be possible for the gasification of the region via Turkey with feasible and affordable netback values. On the other hand, the growing and expanded Turkish Gas Market is the base case target for EastMed gas. It is generally expected that Turkey will need an additional 25 BCM/y from new concrete gas sources towards 2030 if all ongoing contracts (52 BCM/y based EMRA official announcements) will be renewed. But only 6 BCM/y of that amount was secured by the Shah Deniz Phase II contract of BOTAŞ. So, the Gazprom- dominated Turkish gas market indicates huge new contract competition in the short to mid-terms. Based on the Model, EastMed Gas Resources shall probably enter the gas-to-gas competition with at least 26.75 BCM/y of additional gas volumes for the Turkish Market beyond 2020.

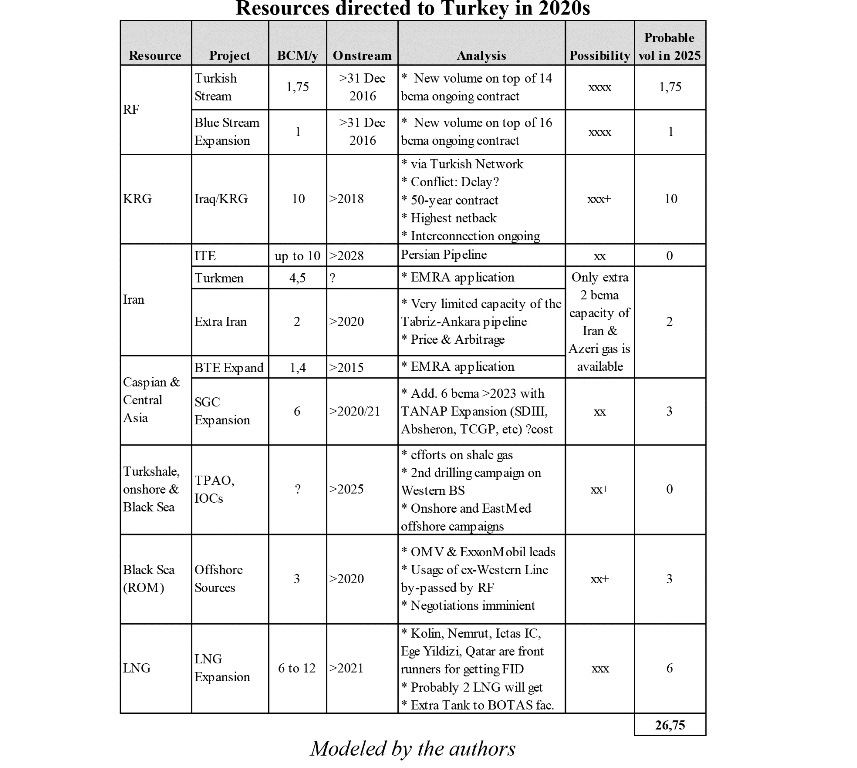

Simple Analysis on Main Gas-to-Gas Competition (except LNG) of EastMed Gas Resources directed to Turkey in 2020s

The future and possible gas imports to Turkish market are simply analyzed in the table above. This data is in addition to the existing 52 BCM/y in long-term oil-indexed contracts and the already signed 6 BCM/y Shah Deniz Phase II volumes via TANAP. Although the sources and quantities of these new, prospective imports are very controversial, the authors considered the most discussed options currently circulating in energy oriented circles; EastMed gas could enter in 2020s with 2,75 BCM/y of new Gazprom, 10 BCM/y of Iraq/KRG, maximum 2 BCM/y of Iran, Trans-Iran and additional BTE gas (due to lack of sufficient infrastructure on the Tabriz-Ankara line), around 3 BCM/y of new Caspian volumes via TANAP Expansion, 3 BCM/y of offshore Black Sea input and new 6 BCM/y LNG contracts via a new LNG terminal (probably on the Aegean cost). Therefore there is plenty of room for economically and technically feasible EastMed gas in Turkey beyond 2020. The Main and Late Gas phases of the Model are completely identical with the facts and figures of the Turkish gas Market requirements in the mid-term.

The EastMed gas resources are a new frontier for the global market

Finally, given the reality of dipped LNG prices (lower than eight USD/MMBtu in Asia on mid-June 2015), and the huge LNG liquefaction investments of Australia, a new gas bonanza in Eastern Africa, upcoming U.S. shale-to-LNG efforts, robust Qatar and newest player Iran, an EastMed LNG export option to Asia via FLNG is absolutely non-feasible and non-economical. The tight European LNG market might also be a target for EastMed gas via future Egyptian LNG trains, but U.S. loads, RF LNG campaigns, stronghold Statoil as well as West Africa LNG investments make this option non-commercial.

Conclusion

The EastMed gas resources (1.2 TCM proven and more than 2.4 TCM yet to be found in the Levant basin and more in the Nile basin) are a new frontier for the global market. However, geopolitical, technical, legal and financial challenges, as well as recently plunged oil prices have hit commercialization efforts hard. LNG is too complicated, FLNG is not affordable, and CNG technology is too young for an EastMed-style sophisticated solution. The exportation of a limited amount of EastMed gas solely to domestic markets is unfeasible, based on the mature market condition.

As the leading-edge of the basin, Israel is severely struggling to implement upstream investments. An anti-trust investigation on Noble-Delek, along with export limitations, reduced global gas demand, and technical difficulties are major setbacks for Israel. The objection of the most feasible market and transit option of Turkey,81 poses another big challenge for both the GCA and the Israeli government. Moreover, signed non-binding LoIs have now turned into question marks due to the ongoing, indefinite status of the gas projects of the EastMed.82

Ongoing marketing studies of EastMed “Early Gas” are compatible with the export model through Turkey. Based on the forecasted model, the first phase of the EastMed gas (around 21 BCM/y) shall solely be dominated by Israeli fields and be directed to domestic demand and the Egyptian LNG trains of the region. After that, the second phase (Main Gas) shall be represented by consolidation, Upstream Hub development, formation of the Corporation and the Steering Committee and application of stages of the Pipeline. 16 BCM/y gas shall be marketed via the first twin leg (or single 32-inch) of the pipeline starting from 2023. The third phase (Late Gas) shall optionally be represented by further consolidation, gas addition from the adjacent and northern sector of the EastMed basin, and the construction of new twin pipelines (or a second 32-inch grid) to/through Turkey.

The TRNC-GCA and Israel-Palestine/Gaza conflicts are the backbone of the geopolitical black holes of the EastMed region, alongside the ongoing Syrian civil war. Turkey (and TRNC) and Greece (and the GCA) will probably be requested to settle the EEZ and sovereignty disputes by the main global players and organizations. The relief of Israel-Palestine/Gaza conflicts will probably be concluded in mid-term. Therefore Turkey is the key for resolving of two problematic issues due to its main supporter position for TRNC and Palestinian rights. Otherwise, the problems may be accelerated by ongoing radical terrorism, and turned into a regional supernova explosion.

Meanwhile, Turkey initiated and fully supported the EU’s Southern Gas Corridor concept. Turkey always respects the commercial feasibilities of the projects and, if they are viable, fully supports them (like TANAP). The stabilization and gas-related economic benefits shall build the main consensus between the parties. The build-up nature of the Project is the only win-win solution for the each party starting from 2023. 16 BCM/y or more EastMed gas would be delivered to Turkey as well as the EU border at most competitive prices. Therefore, Turkey will definitely be the core of this proposed model in terms of its geographic position, transit nature, pipeline experience, world-class economy, power, history, and gas-waiting market conditions.

Endnotes

- “Soğuklar Doğalgaza Rekor Kırdırdı,” Milli Gazete, (10 January 2015), p. 5.

- BP Statistical Review, 2014.

- “Doğal Gaz Aylık İthalat Bilgileri,” T.C. Enerji Piyasası Düzenleme Kurumu, retrieved December 18,

2014, from http://www.epdk.org.tr/index.php/dogalgaz-piyasasi/lisans/12-icerik/dogalgaz-icerik/1128-

dogal-gaz-ithalat-bilgileri#2013-yili-aylik-ithalat-miktarlari - Gareth M. Winrow, “The Southern Gas Corridor and Turkey’s Role as an Energy Transit State and Energy Hub,” Insight Turkey, Vol. 15, No. 1, (Winter 2013), pp. 145- 63.

- USGS, “Assessment of Undiscovered Oil and Gas Resources of the Levant Basin Province, Eastern Mediterranean,” Fact Sheet 2010-3014 World Petroleum Resources Project, (March 2010).

- Ibid.

- Alain Bruneton, Elias Konofagos and Anthony E. Foscolos, “Cretan Gas Fields – A new perspective for Greece’s hydrocarbon resources,” Pytheas Market Focus, (30 March 2012).

- Ministry of Energy and Water Resources, Petroleum and Natural Gas Prospecting, retrieved December 15, 2014, from http://energy.gov.il/English/Subjects/OilAndGasExploration/Pages/GxmsMniPetroleumAndNaturalGasProspecting.aspx

- BG Group, retrieved December 10, 2014, from http://www.bg-group.com/OurBusiness/WhereWe

Operate/Pages/AreasofPalestinianAuthority.aspx - “Delek Group, Holdings, Energy and Infrastructure,” retrieved December 12, 2014, from http://www.delek-group.com/Holdings/EnergyInfrastructure/DelekEnergy.aspx

- “Noble Energy, Operations, Eastern Mediterranean,” retrieved December 12, 2014, from http://www.nobleenergyinc.com/Operations/International/Eastern-Mediterranean-128.html

- “Israel’s Leviathan Gas Reserves Estimate Raised by 16 pct,” Reuters, retrieved December 12, 2014, from http://www.reuters.com/article/2014/07/13/israel-natgas-leviathan-idUSL6N0PO08Q20140713

- Platts LNG Daily, (May 23, 2013).

- Israel National News, (December 14, 2014).

- Guy Katsovich, “Pelagic gas field estimated at 6.7 TCF,” Globes, (June 3, 2012).

- “Enerji IQ Turkish Energy Market Report Biweekly,” No: 2014-15/38, (December 9, 2014).

- “Noble Energy, Operations, Eastern Mediterranean,” retrieved December 15, 2014, from http://www.nobleenergyinc.com/Exploration/Recent-Discoveries-130.html

- “Delek Group Announces Consolidated Results for the First Quarter of 2012,” Press Release, (May 30, 2012), retrieved December 15, 2014, from http://ir.delek-group.com/phoenix.zhtml?c=160695&p=irol-newsArticle&ID=1700654&highlight=Cyprus

- “Strong International Interest as Cyprus’ Hydrocarbon Bidding Round Closes,” Cyprus News Agency, (May 11, 2012).

- Roudi Baroudi, Euro Med Oil & Gas Exploration & Production Summit, (September 25, 2012).

- “Turkey’s TPAO, Shell Sign Exploration Deal,” Reuters, retrieved December 20, 2014, from http://uk.

reuters.com/article/2011/11/23/turkey-shell-idUKL5E7MN1AA20111123 - Hakim Darbouche, Laura El-Katiri and Bassam Fattouh, “East Mediterranean Gas: What Kind of a Game-Changer?,” Oxford Institute for Energy Studies (OIES), NG71, (December 2012), p. 37.

- Seth Cropsey and Eric Brown, “Energy: The West’s Strategic Opportunity in the Eastern Mediterranean,” Hudson Institute, (December 2014), p. 47.

- “Israel Defense Forces: Greece-U.S.-Israel Joint Military Training,” Jewish Virtual Library, retrieved December 19, 2014, from http://www.jewishvirtuallibrary.org/jsource/Society_&_Culture/nobledina.html

- “Enerji IQ Turkish Energy Market Report Biweekly,” No: 2014-15/38, (December 9, 2014).

- Ibid.

- Ibid.

- Ibid.

- NewsBase Middle East Oil and Gas (MEOG), 2014 Annual Review (October 2014), pp. 20-21.

- Various news retrieved December 15, 2014; CyprusPhileNews, December 8, 2014; Famagusta Gazette, September 28, 2014; Cyprus Mail, September 26, 2014; Ekathimerini, September 26, 2014.

- “Shell’s Record-Breaking Prelude Takes to the Water,” BBC, retrieved December 26, 2014, from http://www.bbc.com/news/technology-25213845, (December 4, 2013).

- “Enerji IQ Turkish Energy Market Report Biweekly,” No: 2014-15/38 (December 9, 2014).

- NewsBase Middle East Oil and Gas (MEOG), Week 50 (December 16, 2014), pp. 6-7.

- Ibid.

- Christis Enotiades, “East Med’s Natural Gas Comparative Advantage Lies in Regional Markets,” Cyprus Gas News, (November, 2014), retrieved December 12, 2014, from http://www.coselle.com/resources/news/east-med%E2%80%99s-natural-gas-comparative-advantage-lies-regional-markets

- NewsBase Middle East Oil and Gas (MEOG), Week 50 (December 16, 2014), p. 6-7.

- Osman Kalfaoğlu, “Doğalgaza İlgi Azalıyor,” Kıbrıs Gazete, (December 19, 2014), p. 1.

- “Enerji IQ Turkish Energy Market Report Biweekly,” No: 2014-15/33 (September 9, 2014).

- Walid Khoudouri, “Will Arab Countries Buy Israel’s Natural Gas?,” Al-Monitor, (December 23, 2014), from http://www.al-monitor.com/pulse/business/2014/12/israel-infiltration-energy-sector.html#

- Ibid; “Egypt Amends Oil, Gas Deals with BP, RWE,” Natural Gas Asia, retrieved December 25, 2014, from http://www.naturalgasasia.com/egypt-amends-oil-gas-deals-with-bp-rwe-14302.

- “Israel Threatens to Revoke Leviathan Gas Development Deal,” Reuters, retrieved December 22, 2014, from http://www.reuters.com/article/2014/12/22/natgas-israel-leviathan-idUSL6N0U63C120141222

- Gal Luft, “Israel’s Gas Dream-The End is Night,” Natural Gas Europe, (December 23, 2014), retrieved December 25, 2014, from http://www.naturalgaseurope.com/israel-anti-trust-threat-impairs-gas-dream?

utm_source=Natural+Gas+Europe+Newsletter&utm_campaign=305e2e26ea-RSS_EMAIL_CAMPAIGN

&utm_medium=email&utm_term=0_c95c702d4c-305e2e26ea-287982765. - Ibid.

- NewsBase Middle East Oil and Gas (MEOG) Monitor, Week 2, Issue 508, (January, 2015), pp. 4-5.

- Walid Khoudouri, “Will Arab Countries Buy Israel’s Natural Gas?,” Al Monitor, (December 23, 2014), retrieved December 25, 2014, from http://www.al-monitor.com/pulse/business/2014/12/israel-infiltration-energy-sector.html##ixzz3MtDFkBrC

- Globes, February 14, 2013.

- “Turkey ‘Would Not Accept’ Greece-Egypt Mediterranean Deal,” Hurriyet Daily News, (December 9, 2014), retrieved December 10, 2014, from http://www.hurriyetdailynews.com/turkey-would-not-accept-greece-egypt-mediterranean-deal-----.aspx?pageID=238&nID=75390&NewsCatID=345

- “Greek PM: Turkey Must Respect Cyprus’ Right to Search for Offshore Oil and Gas,” Penn Energy, (February 2, 2015), retrieved February 2, 2015, from http://www.pennenergy.com/articles/pennenergy/2015/02/greek-pm-turkey-must-respect-cyprus-right-to-search-for-offshore-oil-and-gas.html?cmpid=EnlDailyPetroFebruary32015&cmpid=EnlUpstreamFebruary42015

- Ayla Gürel et al., “The Cyprus Hydrocarbons Issue: Context, Positions and Future Scenarios,” PCC Report, PRIO Cyprus Center, (2013).

- Elias Hazau, “Gas Finds Always ‘Hit and Miss’,” Cyprus Mail, (December 23, 2014), retrieved December 10, 2014, from http://cyprus-mail.com/2014/12/23/gas-finds-always-hit-and-miss/

- “Second Cyprus Offshore Licensing Round Participants and License Applications,” Middle East Economic Survey (MEES), (October 26, 2012).

- Hazau, “Gas Finds Always ‘Hit and Miss’,”

- Ayla Gürel et al., “The Cyprus Hydrocarbons Issue: Context, Positions and Future Scenarios,” p. 112.

- “Kıbrıs Doğalgazını Mısır’a İhraç Etme Görüşmeleri Hızlanıyor,” Dünya, (November 27, 2014), p. 10.

- “Doğalgaz İçin Beş Maddelik işbirliği,” Kıbrıs Postası, (November 27, 2014), p. 26.

- “Egypt, Greece and Cyprus Pledge Energy Cooperation”, Natural Gas Europe, retrieved November 10, 2014 from http://www.naturalgaseurope.com/egypt-greece-and-cyprus-pledge-energy-cooperation

- “Mısır’a Doğalgaz Satmaya Odaklandılar,” Kıbrıs Gazete, (August 29, 2014), p. 18.

- Platts European Gas Daily, Vol. 19, No. 249, (December 23, 2014), p. 7.

- Retrieved December 22, 2014, http://www.hurriyet.com.tr/ekonomi/27819121.asp

- CyprusPhileNews, November 8, 2014.

- Karen Ayat, “Total Reconsidering Presence in Cyprus,” Natural Gas Europe, (January 22, 2015), retrieved January 22, 2015, from http://www.naturalgaseurope.com/total-cyprus-east-med-gas-difficulties?utm_source=Natural+Gas+Europe+Newsletter&utm_campaign=8ec2102050-RSS_EMAIL_CAMPAIGN&utm_medium=email&utm_term=0_c95c702d4c-8ec2102050-287982765

- Simone Tagliapietra, “Towards a New Eastern Mediterranean Energy Corridor? Natural Gas Developments between Market Opportunities and Geopolitical Risks,” Nota Di Lavoro – FEEM, (2013).

- “Boru Hattı Fizibilite Çalışması İçin 4 Milyon Euro,” Star Kıbrıs, (December 11, 2014), p. 21.

- “EU Urges Feasibility Study for Importing Israeli Natural Gas,” Bloomberg Business, retrieved

December 9, 2014, from http://www.businessweek.com/news/2014-12-09/eu-urges-feasibility-study-

for-importing-israeli-natural-gas - Karen Ayat, “Israel Proposes an East Med Gas Pipeline,” Natural Gas Europe, (November 24, 2014), retrieved November 24, 2014, from http://www.naturalgaseurope.com/israel-proposed-an-east-med-pipeline?utm_source=Natural+Gas+Europe+Newsletter&utm_campaign=4dfaee8572-RSS_EMAIL_CAMPAIGN&utm_medium=email&utm_term=0_c95c702d4c-4dfaee8572-287982765

- Retrieved December 15, 2014, from http://www.coselle.com/resources/news/east-med%E2%80%

99s-natural-gas-comparative-advantage-lies-regional-markets - Mehmet Melikoğlu, “Vision 2023: Forecasting Turkey’s Natural Gas Demand between 2013 and 2030,” Renewable and Sustainable Energy Reviews, (2013), Elsevier, pp. 393-400. See also David Tonge, Ceren Uzdil and Feza Şanlı, “Trends and Outlook for Turkish Gas and Power”, IHS Energy Insight Briefing Conference, IBS Research & Consultancy, Istanbul, (May 29, 2013), and Gareth Winrow, “Realization of Turkey’s Energy Aspirations: Pipe Dreams or Real Projects”, Turkey Project Policy Paper, No. 4, (April 2014), Center on the United States and Europe at Brookings, p. 26.

- Gulmira Rzayeva, “Natural Gas in the Turkish Domestic Energy Market: Policies and Challenges,” Oxford Institute for Energy Studies, OIES Paper NG82, (February, 2014).

- İbrahim Said Arinç, “Natural Gas Geopolitics of Turkey”, Ph.D. Thesis Durham University, (2014).

- Simone Tagliapietra, “Towards a New Eastern Mediterranean Energy Corridor? Natural Gas Developments between Market Opportunities and Geopolitical Risks,” Nota Di Lavoro – FEEM, (2013).

- Ibid.

- Enerji IQ Turkish Energy Market Report Biweekly, No: 2014-15/38, (December 9, 2014).

- NewsBase Middle East Oil and Gas (MEOG), Week 3, (January 21, 2014), pp. 6-7.

- Matthew J. Bryza, “Eastern Mediterranean Natural Gas: Potential for Historic Breakthroughs among Israel, Turkey and Cyprus,” Turkish Policy Quarterly, (Fall 2013), pp. 35-44.

- “Boru Hattı Türkiye’den Geçebilir,” Haberal Kıbrıs, (January 1, 2014), p. 1.

- “Turkish Energy Company Set to Build Pipeline for Israeli Natural Gas,” Daily Sabah, (May 15, 2014),

p. 5. - “Zorlu, İsrail Gazını Denizaltından Ceyhan’a Getirecek,” Dünya, (May 22, 2014), p. 20.

- İbrahim Said Arinç, “Natural Gas Geopolitics of Turkey”, Ph.D. Thesis Durham University, 2014.

- Walid Khoudouri, “Will Arab Countries Buy Israel’s Natural Gas?,” Al Monitor, (December 23, 2014), retrieved December 25, 2014, from http://www.al-monitor.com/pulse/business/2014/12/israel-infiltration-energy-sector.html##ixzz3MtDFkBrC

- İbrahim Said Arinc, “Natural Gas Geopolitics of Turkey,” Durham University, PhD Thesis, (2014).

- “TPAO to Continue Cyprus Exploration,” Upstream Online, retrieved January 6, 2015, from http://

www.upstreamonline.com/live/1387931/TPAO-to-continue-Cyprus-exploration?utm_source=

Upstreamonline+Daily+Newsletter&utm_campaign=37412f90ee-DailyNewsletterUSA_07_01_2015&utm_medium=email&utm_term=0_3d794df7ec-37412f90ee-302778449 - “Ürdün İsrail ile Doğalgaz Anlaşmasını Askıya Aldı,” Salom, (January 7, 2015), p. 8.