Introduction

Russia’s growing involvement in the Middle East has created a colorful profusion of authors studying the different aspects of its regional presence.1 Their research offers interesting and deep insights into the Russian dialogue with the region, allowing readers to look at these ties from different angles.2 Amongst other topics, their studies inevitably address the issue of Moscow’s relations with the Gulf Cooperation Council (GCC), as this vector of Russia’s diplomacy possesses substantial importance within Moscow’s bigger strategy in the Middle East and clearly affects the overall situation in the region.3 Within this, the focus is mainly on the political aspects of Russia’s interaction with the GCC member states.

For instance, the analysis of these ties through the prism of Russia’s relations with the West and Moscow’s ambitions to play the role of a global player in the international arena has become a very popular way to approach the issue.4 When explaining the motives behind the Russian moves the majority of authors refer to the impact that the dynamics of Russia’s confrontation with the West has on Moscow’s dialogue with the GCC member states.5 In his study Mark Katz also argues that while Moscow’s decisions obviously play a role in whether its Middle Eastern policies have been successful or not, sometimes Moscow’s successes or failures are affected by policies pursued by the U.S. and other non-regional actors.6 This idea is further developed in the publications by Samuel Ramani who pays a lot of attention to the geopolitical factors affecting Russian-GCC relations.7

Yet, not all researchers share these views. Some of them argue that while the Kremlin’s geostrategic games in the region definitely play a very important role in Moscow’s decision-making with regards to the Gulf, the authors are often carried away by this explanation and fail to discuss other important drivers of Russian diplomacy in the region, such as domestic or economic factors. However, Moscow-based scholar Leonid Issaev, on the contrary, pays more attention to the role of Russia’s domestic policies in shaping Moscow’s approaches towards the region. He believes that Russian foreign policy towards the Gulf cannot be considered in isolation from the political processes going on inside Russia. Issaev insists that, on many occasions, it is not foreign policy priorities but domestic security concerns, disagreements inside the Russian political elite, and Kremlin’s propaganda needs, which play the role of key factors determining Russia’s decision-making process on the Middle East and the Gulf.8

Russia’s dialogue with Saudi Arabia in the OPEC+ is often considered within the framework of Moscow’s vision of the global energy markets, rather than from the point of its significance for the Russian dialogue with the region itself

Unfortunately, the economic dimension of Russia’s cooperation with the GCC has traditionally been overshadowed by the ongoing discussion on what political factors play the leading role in shaping Russia’s approaches to the region. Of course, there were attempts to analyze the impact of economic factors on Moscow’s cooperation with the region. Yet, the majority of studies either just touch upon the economic factors within the broader discussion of Moscow’s regional approaches or, on the contrary, concentrate attention on a narrow aspect of the economic cooperation (such as trade, investments, or coordination of efforts in the oil market).9 Even Russia’s dialogue with Saudi Arabia in the OPEC+ is often considered within the framework of Moscow’s vision of the global energy markets, rather than from the point of its significance for the Russian dialogue with the region itself.10 Under these circumstances, studies by the UAE-based scholar Li-Chen Sim represent a positive exception as she actively positions Russia’s priorities in the oil and gas sphere as one of the pillars of Moscow’s diplomacy in the Gulf.11

Theodore Karasik’s chapter “Russia’s Financial Tactics in the Middle East” published in 2018 in the collective monograph Russia in the Middle East is, probably, another outstanding study of Russia’s economic ties with the GCC that allows readers to look at this issue from another angle.12 In his paper, Karasik not only analyses the intricate structure of Russia’s financial and investment relations with the Gulf monarchies, but also shows how these economic ties relate to Moscow’s political goals. However, in both Karasik and Sim’s studies, their publications are focused on certain aspects of the Russian economic relations with the region. This article will try to adopt a more comprehensive approach. Instead of diving into the deep study of one of the aspects of these ties, it will offer a broader picture of the complex of economic interactions between the GCC countries and Russia by not only analyzing the current state of trade and investment relations between them but also through the discussion of the origins of Russia’s interest in cooperation with Saudi Arabia, the UAE and Kuwait within the framework of the OPEC+ and potential reasons for future divergence between Russia and the GCC member states in the hydrocarbon markets. Finally, special attention will be paid to the question of prospects for the further development of Russian economic relations with the Arab states of the Gulf.

Russian Trade with the GCC: Small but Important

Moscow’s involvement in the conflicts in Syria and Libya, its close contacts with the Palestinian authorities and Israel, as well as attempts to maintain good ties with the warring sides in Yemen, help to demonstrate to the United States and the EU Russia’s importance as a global player, thus compelling them to at least take its opinions into account and to keep communication channels with Moscow open. In other words, Russia’s presence in the Middle East advertises its capacity to project power and helps Moscow avoid international isolation. Russia can play troublemaker when necessary to show that ignoring its interests might be dangerous. In this respect, it considers its relations with the region as another (although very important) bargaining chip in its relations with the United States and the EU. However, Russia’s decision-makers do not see the region solely through the prism of relations with the West. The region is important to them in and of itself due to economic reasons. Russia’s economic goals in the region are twofold: Moscow considers the Middle East as an important source of investments and a market for some of its industries (above all arms manufacturing, agriculture, the nuclear sector, as well as oil, gas, and petrochemicals). Russia’s state budget depends on hydrocarbon exports. The Kremlin is concerned about a potential fall of the oil price to below $40 per barrel (as it would mean Moscow would be unable to both meet all budget needs and put money into its reserve funds), which compels Russia to cooperate actively with the Organization of the Petroleum Exporting Countries (OPEC), and its informal leader, Saudi Arabia. Russia’s hydrocarbon producers and service companies have also intensified their attempts to acquire stakes in energy projects in the region.

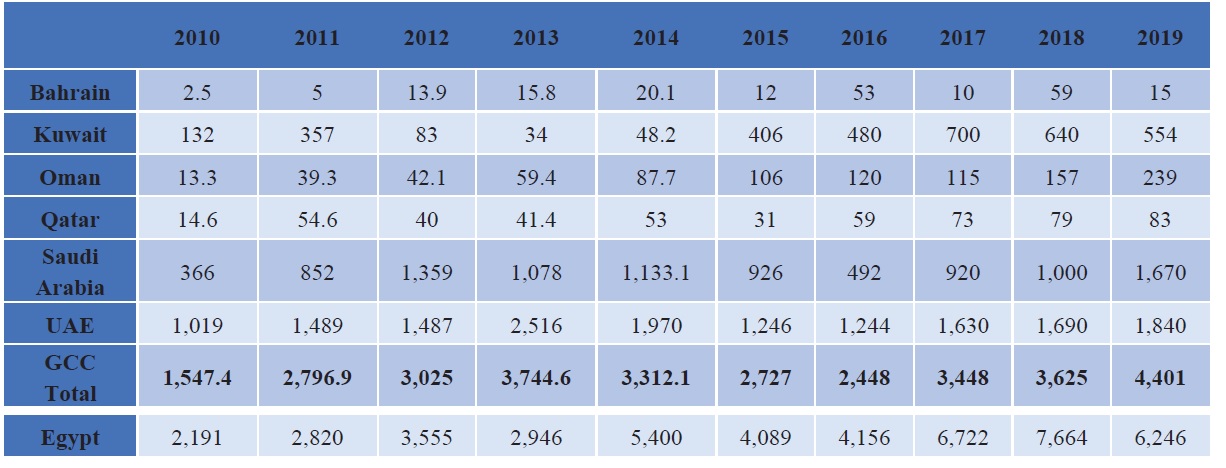

At first glance, the volume of Russia’s trade with the GCC might create the wrong perception of the minimal role of economic drivers in the development of the dialogue between Moscow and the region. Indeed, the GCC share in Russian foreign trade is less than 1 percent. In terms of sheer numbers, Russia’s trade with the Gulf might also seem unimpressive: for instance, for the last ten years, its aggregated volume only once managed to surpass that of Russian trade with Egypt, one of Russia’s main trade partners in the Arab world (Table 1).

Table 1: Russian Aggregated Volume of Trade with the GCC Member Countries and Egypt (2010-2019, $ million)

Source: The statistics of the Russian Federal Customs Service13

Source: The statistics of the Russian Federal Customs Service13

Moreover, there is a serious difference between the GCC member countries in terms of the volume of their trade turnover with Russia. While in the U.S. dollar terms it remains insignificant in the case of Bahrain, Qatar, and, to a lesser degree, Oman, Russian trade with Saudi Arabia, the UAE, and Kuwait has substantially grown since 2010, thus, reaching relatively good levels for the MENA countries.

During the last decade, items exported by Russian corporations to the region have also diversified, with the share of machinery sold to the GCC gradually rising

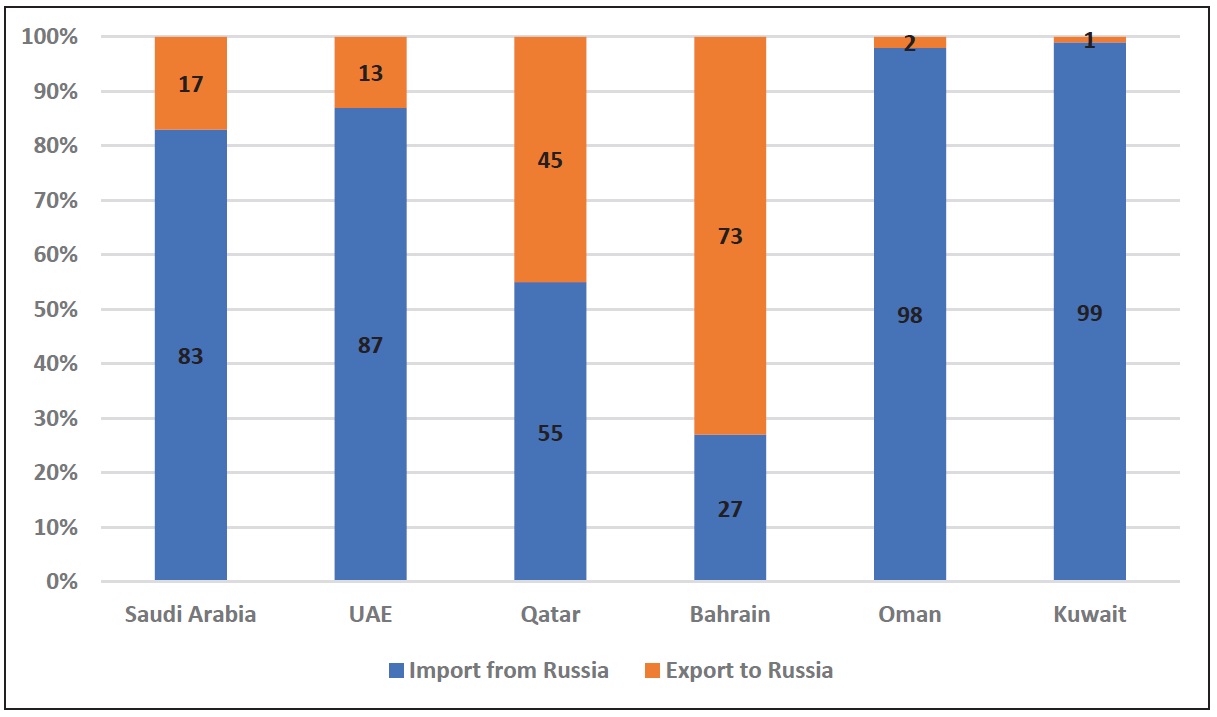

Yet, it is not the quantity, but the quality that matters. The fact that the trade balance is in favor of Russia makes Moscow see it as a small but reliable source of income that has been almost steadily growing for the last ten years (Graph 1). What is more important, the range of items exported by Russian companies is quite diversified (with the exception of Kuwait), thus offering a niche for different producers and goods – arms and military equipment, machinery, oil and gas, petrochemical, metallurgical and agricultural products.

Graph 1: Export-Import Ratio of Russian Trade with the GCC by Country (2019, %)

Source: The statistics of the Russian Federal Customs Service14

Source: The statistics of the Russian Federal Customs Service14

The region still holds great interest and, in some cases, even key importance for certain sectors, including the agricultural and military-industrial complexes, and the petrochemical, space, and oil and gas industries. As such, the UAE is an important buyer of Russia’s precious stones and metals whereas Saudi Arabia is one of the main consumers of Russian grain, sales of which are playing a significant role in Russia’s doctrine of export diversification. The region is also an important market for some small and medium-sized enterprises, for which trade with the Middle East often represents the main export market for their products.

During the last decade, items exported by Russian corporations to the region have also diversified, with the share of machinery sold to the GCC gradually rising. As such trade with the Gulf countries is helpful for the implementation of the government’s economic diversification strategy.

The UAE and Saudi Arabia are more focused on investments in local infrastructural projects that have regional rather than federal importance

Finally, after 2015, Russia’s increased arms sales to the Middle East became a separate driver of its regional engagement. Russia’s military assistance to Iraq in its struggle against ISIS in 2014 and subsequent support of the Assad regime in Syria with equipment and ammunition that led to Moscow’s direct involvement in the Syrian conflict in 2015 became an effective promotional exercise for the Russian military-industrial complex. Consequently, not only has the volume of Russian arms exports to the region increased, the importance of this market for the Russian arms producers has increased as well which in turn has heightened the incentives for Moscow to invest in building positive relations with the region. According to the official data, in 2018, the Middle East share in the Russian arms sales was equal to 48 percent (approximately $7.2 billion) against 37 percent in 2015 (up to $5.5 billion).15

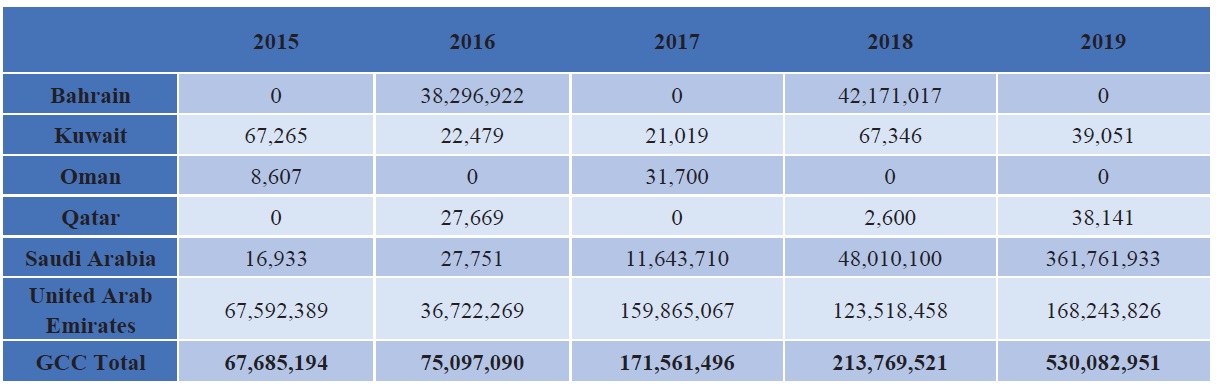

Currently, market analysts also argue that as an outcome of the demonstration of Russian arms capacities in Syria, Moscow managed not only to secure its presence in the traditional consumer markets such as Algeria, Egypt, and Iraq but also advance its presence in the arms markets of the countries traditionally less open for Russia such as the members of the GCC.16 The real volume and structure of Russia’s arms trade with the Gulf is unknown. The official reports of the Russian Federal Customs Service usually classify arms deals under so-called a ‘Secret Code Category’, which includes all imports and exports that the Russian authorities prefer not to declare. With regard to the Gulf, the official data of Russian customs’ confirms that during the period 2015-2020 Moscow was, indeed, exporting goods under the ‘Secrete Code Category’ to the GCC. If assumed that all these figures reflect the exports of arms only, it is possible to conclude that the region was not Russia’s main customer. The volume of export gains also has not matched that of the U.S. or EU. Yet, they have been growing rapidly since 2015 thus raising the importance of the Gulf market in the eyes of Russia’s arms traders (Table 2).

Table 2: Russia’s Exports under the Secret Code Category to the GCC Member Countries (2015-2019, $)

Source: The statistics of the Russian Federal Customs Service17

Source: The statistics of the Russian Federal Customs Service17

Russian media sources also confirm the fact of the rising importance of the Gulf as Russian arms consumers. Among other GCC players, the UAE has probably the longest experience of arms trade cooperation with Russia, and Russia’s arms producers are often guests at the IDEX arms fair.18 In 2017, Russia and the UAE signed a cooperation agreement in the military-industrial sector.19 And, yet, bilateral trade is just one of the elements of Russia’s cooperation with the GCC countries. Russia’s economic goals in the region are broader.

Russian-GCC Investment Cooperation: Economic Motivation with the Political Aftertaste

First of all, Russia considers the GCC as an important source of investments in Russia’s economy, giving priority to infrastructural projects. The Russian Direct Investment Fund (RDIF) serves as an entry gate for GCC investments to the Russian economy. It facilitates the deals between an Arab investor and a Russian recipient. Alternatively, it can establish joint funds with the Gulf States business and financial entities to invest in infrastructural projects inside Russia. The list of the RDIF partners includes Emirati Mubadala, DP World, Saudi Public Investment Fund, Saudi Aramco, Ayar International Investment Company, Qatar Investment Authority, Kuwait Investment Authority, and Bahraini Mumtalakat Holding Company. As of 2018, the share of the GCC countries in the RDIF investment projects (including potential) was estimated at 52 percent, specifically Saudi Arabia accounted for 22 percent, the UAE 18 percent, Qatar 8 percent and Kuwait 2 percent).20 For the last seven years, the volume of Saudi Arabia’s investments in Russia reached $2.5 billion, while the UAE’s and Kuwait’s is under $1 billion.21 Meanwhile, in terms of value, Qatar remains a leader with $13 billion of investments.22

The strategies of the GCC investors differ by country. Bahrain and Oman have no known presence in Russia while Kuwait keeps its activities low profile. Thus, in 2012, the Kuwait Investment Authority signed an agreement with the RIDF on the provision of $500 million (in 2015, this figure was doubled) for future investments in Russia’s economy through the so-called automatic co-funding scheme. The scheme implies that Kuwait investors can automatically participate in the RDIF’s projects covering up to 10 percent of necessary funds. However, there is no confirmed data on any investment projects in Russia.23

During the last ten years, the UAE has been actively investing in the development of the economic infrastructure of Chechnya and the urban development of its capital, Grozny

Qatar, the UAE, and Saudi Arabia are, on the contrary, much more active. Thus, in recent years Ayar International Investment Company participated in the reconstruction of St. Petersburg’s tram lines. The UAE monies were invested in the development of IT software for Russian oncology and maternity centers. Mubadala contributed to the development of medical clinics in Podolsk and Balashikha. It also funded the construction of logistic complexes for Novosibirsk and Moscow districts. Meanwhile, the PIF participated in the reconstruction of the petrochemical factory ZapSibNeftekhim in Tobolsk, the construction of hydropower plant in the Karelian district, and the transport infrastructure of St. Petersburg. As of early 2020, DP World was considering the purchase of a 49 percent stake in Vladivostok-based transport company Fesco.24

Doha lesser than the others relies on the RDIF in its investment activities and prefers buying shares in large companies such as Russia’s hydrocarbon giant Rosneft, one of Russia’s main banks VTB and Pulkovo airport in St. Petersburg (the main transport hub in the North-West of the European part of Russia). The UAE and Saudi Arabia are more focused on investments in local infrastructural projects that have regional rather than federal importance.25

Qatari, Emirati, and Saudi approaches to investment in Russia’s economy have their own pros and cons in terms of economic gains and political dividends. Thus, the Qatari strategy of investing in large companies definitely helps Doha to create its lobby of supporters at the very top of the Russian elite, at the federal level, and gain access to the projects with high returns. These investments are also immediately visible to the Russian central authorities, which also helps the Qatari government to gain additional esteem in the eyes of Moscow. The efforts of the UAE and Saudi Arabia might, at the first approach, seem less important both economically and politically as the size of their investments in a single project might be less than a hundred thousand dollars and have a low level of return. However, this perception is deceiving. In the long run, the positive effect from these investments can be higher. Thus, the aggregated value of these small projects, for the Russian economic development, appears greater than from the purchase of shares in Russia’s giants by a foreign investor. The participation in these projects also creates more deep-rooted political ties between the UAE, Saudi Arabia, and Russia, thus, opening options for participation in bigger and more profitable projects in the future.

First of all, small and medium investments at Russia’s regional level help to ease the financial burden on the shoulders of the Russian regional authorities and speed up the implementation of those projects that do not have enough federal support (i.e. funded either predominantly or solely from local budgets). This, in turn, creates a positive image of the Gulf states at the regional level and helps them to form quite a wide base of their supporters among the local elites who, in turn, might promote the interests of the GCC states in Moscow. It is not surprising that the UAE and Saudi investments are especially welcomed in the Northern Caucasus regions that cannot fund their needs without either external or federal support.26 This interaction also creates an important humanitarian dimension of Russian economic cooperation with the GCC when the Gulf investments in the local regional projects help to create additional job places or improve social infrastructure. Consequently, Moscow is additionally motivated to cooperate with the GCC as long as this cooperation creates opportunities to improve the socio-economic situation in traditionally poor regions and, subsequently, strengthen the country’s socio-economic and political stability. For instance, during the late spring-early summer 2020, the UAE provided humanitarian assistance to the North Caucasian districts of Russia severely hit by COVID-19. During the last ten years, the UAE has been actively investing in the development of the economic infrastructure of Chechnya and the urban development of its capital, Grozny. Among all, in 2017, the Sheikh Zayed Fund opened its office in Grozny with the aim to support the development of small and medium private enterprises. In terms of the economy, the value of the UAE activities is not high. For instance, during the period 2017-2027, the Shaikh Zayed Fund is to invest in Chechnya’s economy about $300 million (by 2020, the fund had invested up to $6 million in Chechnya’s private business).27 Yet, in terms of gains, this financial assistance definitely brings the Chechen elite closer to the Emirates while helping to improve the social situation inside this region.

Russian business is also interested in entering the GCC. There is a distinct interest for Russian companies to enter the agro-industrial and nuclear sectors of the GCC economies, and create joint ventures in the field of telecommunications, IT technologies as well as the mining and petrochemical sectors. As such, Russian economic interests are also becoming more diverse. Moscow also views long-term economic projects as a solid base for the further development of bilateral ties with the region. Russia’s activities in the nuclear sector are an example of politically driven economic steps. Nuclear projects require long-term post-construction service contracts and would bind the countries concerned to Russia. In the case of the GCC countries, such ties could help ensure long-term economic cooperation in the absence of progress in other areas.

Hydrocarbon Frenemies?

Russia’s relations with the GCC countries in the oil and gas field are not that straightforward. In the spring of 2020, the short-lived price war between Russia and Saudi Arabia demonstrated that, in spite of the deep interest in developing cooperation with Middle Eastern hydrocarbon producers put forward by Russia over the last four years, the alliances it has built remain fragile. Even positive bilateral dialogues with Middle Eastern exporters cannot offset challenges to Russia’s position in the global energy markets. The Kremlin is particularly worried about competition over the EU market.

It is often ignored by analysts that Russia and Saudi Arabia have periodically competed for oil markets in Asia and Europe in recent years. In 2018-2019, in spite of domestic production cuts, both increased their supplies to China in a competition for the available share of the country’s market that had been created by a decrease in Iran’s oil exports to China, growing domestic demand, and Beijing’s attempts to diversify its sources of hydrocarbon imports. In the first half of 2019, Russia became the largest oil exporter to China, but by the beginning of 2020 Saudi Arabia had taken over this position. Saudi Arabia has also been a competitor to Russia in other regions. Its decision in July 2019 to further discount oil sold to Europe caused concern in Russia. These concerns strengthened again when following the Russian March 2020 decision to leave the OPEC+ arrangement, Saudi Arabia declared its intention to provide European consumers with historically high discounts on its oil for April loaded cargoes. Moscow, however, equally never missed an opportunity to exploit the misfortunes of the Arab ‘partners.’ In September 2019 following the attack by Iranian proxies on the Saudi oil-refining infrastructure in Abqaiq and Khurais, Riyadh was temporarily unable to fulfill its export obligation to Asian countries. Russia immediately used this opportunity to position itself as a more reliable supplier to India in order to increase its share of the country’s market.

Since 2017, the petrochemical company Sibur has been discussing options for entering the project for the construction of the al Jubail petrochemical factory, conducted by Saudi Aramco and TOTAL

The EU’s attempts to decrease its dependence on Russian gas, which started in the mid-2000s, also caused the Kremlin to follow closely Qatar’s plans to increase its output of Liquefied Natural Gas (LNG). Yet, despite Middle Eastern countries being potential rivals in supplying the European and Asian oil and gas markets, Russia continues to prefer cooperation over confrontation and trying to establish good relations to ensure that it has a stake in energy projects in the region. Even during the period of the 2020 price war between Russia and Saudi Arabia (de facto supported by the UAE and Kuwait), Moscow was periodically repeating that it wants to resume the discussion regarding mutual investments into oil, gas, and petrochemical projects with the GCC member countries.28 Earlier on, in October 2019, the Abu Dhabi National Oil Company (ADNOC) awarded Russian company Lukoil a 5 percent share in the Ghasha concession (which consists of nine oil and gas fields). While Lukoil’s share is small its symbolic meaning is high. The Gasha concession became the first large hydrocarbon project in the UAE that includes the participation of a Russian company.29

Russia also continuously utilizes economic means to achieve political goals. The presence of Russian companies in the region in that context is occasionally useful to exert political influence. The company Rosneft is one example. In 2018, the government approved the purchase of 14.6 percent of the company (for €2.5 billion) by the Qatar Investment Authorities (QIA), which increased the latter’s share to 18.93 percent. However, it is not yet clear whether QIA was supposed to retain their stake in Rosneft in the long run: according to initial plans, QIA was to resell its share to a Chinese shareholder, who allegedly would then transfer this stake to private investors in Russia. For reasons that remain unclear, this scheme was not implemented and QIA, therefore, remains the final shareholder. The Russian government’s initial decision was aimed at strengthening ties with Qatar and opening up another channel of communication with its rulers. Here, Rosneft sometimes acts as an informal arm of Russian diplomacy, handling sensitive matters to which the Kremlin does not want to draw attention. For example, Rosneft head Igor Sechin visited Doha in March 2019 and delivered to Qatar’s emir, Shaikh Tamim Bin Hamad Al Thani, a personal message from President Vladimir Putin that allegedly contained suggestions for improving ties.30

Another factor that compels Moscow to prefer cooperation with the GCC countries over rivalry is that Russia wants GCC investors to participate in joint ventures to research, design, and produce oil, gas, and petrochemical equipment, given that current Western sanctions limit Moscow’s ability to import advanced Western technology. Russia pays special attention in this regard to cooperation with Saudi Arabia and the United Arab Emirates. In 2018, Saudi Aramco established cooperation with Moscow State University’s research center on the development of the upstream technologies. Since 2017, the petrochemical company Sibur has been discussing options for entering the project for the construction of the al Jubail petrochemical factory, conducted by Saudi Aramco and TOTAL. Saudi Aramco is also involved in negotiations with Rosneft and Lukoil over joint ventures in the petrochemicals sector. In 2018, the minister of energy, industry, and mineral resources said that Saudi Aramco was also ready to invest in the efforts of Rosneft and Lukoil to buy or build refineries in third countries.

In 2016, joint Russian-Saudi efforts led to the Vienna Agreement between OPEC and non-OPEC countries (so-called OPEC+) to decrease production in order to ensure a degree of stability as far as oil prices were concerned

Russia-Saudi attempts to establish cooperation in the oil, gas, and petrochemical sector have so far brought few results. Almost all discussed projects are still on paper. However, Russia’s cooperation with the UAE represents a different case: it is not accompanied by loud statements on intention and, consequently, it does not draw much unnecessary attention. The discussed projects are more of local importance but, at the same time, the results of these discussions are also more visible. For instance, on September 5, 2018, Gazprom Neft and Mubadala Petroleum (owned by Mubadala Foundation) officially sealed the deal on the purchase of 44 percent of shares of Gazprom Neft’s subsidiary –Gazprom Neft Vostok. By investing in Gazprom Neft Vostok, Mubadala Petroleum not only entered the Russian oil sector but received access to one of the largest Russian oil companies acting in Western Siberia, one of the traditional oil-producing regions. Both the UAE and Russian authorities believe that if the experience of the UAE investments in the Russian oil company appears successful, this deal will open up further access to the Russian oil and gas sector for the UAE money.31 From the practical point of view, the Emirati investments help Gazprom Neft Vostok to intensify the development of the tight oil fields in Western Siberia. This is extremely important for Moscow: the active development of the marginal oil-fields and tight oil reserves might allow Russia either to completely avoid or, at least, to slow down the fall of oil output that is expected to begin after 2021.32

The Rise and Fall of the OPEC+

The dependence of the Russian state budget on the exports of hydrocarbons and the Kremlin’s concerns about long-term low oil price compels Russia to cooperate actively with the OPEC, and in particular with Saudi Arabia. Russia’s decision to begin coordination of its output with OPEC producers can be considered historical. Until the mid-2010s, Moscow’s vision of its relations with the cartel was based on the principle of a free rider: while profiting from the OPEC attempts to regulate the market prices through the readjustment of oil during the 1990s-2000s, Russia showed no interest in coordination with this structure. The OPEC members, in their turn, never insisted on such cooperation.33 Nevertheless, by the mid-2010s, the new trends in the global oil market compelled Russia and OPEC to revise relations in order to protect their interests in the hydrocarbon market.

The roots of the problems encountered by the OPEC oil producers and Russia go back to the late 2000s. They are connected to two factors: the impact of the U.S. shale revolution on the global hydrocarbon market and the beginning of the global energy transition to non-carbon fuels. The shale revolution not only turned the U.S. into the largest producer and exporter of hydrocarbons but also stimulated the emergence of new strong market players in other parts of the world. Driven by these factors, the growth rates in global oil supply have been steadily surpassing growth in oil demand since 2011 causing the markets’ oversupply and destabilizing oil prices in recent years. Due to the specifics of shale oil production and high volumes of oversupply, neither the 2014-2016 price war between traditional and shale oil producers nor OPEC alone could remove the extra barrels from the market.

The high sensitivity of shale oil production to oil prices subsequently shortened the duration of oil price cycles and changed their amplitude: given the ability of shale oil producers to quickly increase output if encouraged by the positive market dynamics, the oil prices were unable to rise too high and/or for too long, forcing the GCC countries and Russia to forget about the era of ultra-high incomes. By 2016, this seriously undermined the role of OPEC which was only able to influence the price dynamics to a limited extent as any reduction in production volumes inevitably raised prices creating favorable conditions not only for the OPEC members, but also for other players to increase the output and, thus, to bring the prices down back again. The situation could be changed only through the increase in the number of the OPEC members in order to raise the potential share of production capacities to be excluded from the global output while decreasing the potential number of free-riders. Under these circumstances, the establishment of efforts for coordination with Russia, one of the largest oil producers in the world, seemed to be logical.

By late 2016, the Russian leadership also realized that this time, without active cooperation with OPEC it will be difficult to ensure stable budget incomes.34 In 2016, joint Russian-Saudi efforts led to the Vienna Agreement between OPEC and non-OPEC countries (so-called OPEC+) to decrease production in order to ensure a degree of stability as far as oil prices were concerned. The initial six-month OPEC+ deal has since been extended several times. It also led to the formation of a permanent forum-like structure with its own charter (signed in July 2019), which allows participants to coordinate and adjust their production policies.35

From Russia’s perspective, the arrangement proved beneficial as the oil price remained fairly high and stable at least temporarily. Thus, according to the Russian Minister of Energy, Aleksandr Novak, in 2019, the Vienna Agreement allowed Russia’s budget to accumulate about $32 billion.36 In December 2019, the deal was extended until April 2020. The announcement by Russia’s Minister of Energy Aleksandr Novak on March 6, 2020, to withdraw Russia from the Vienna Agreement after April 1, 2020 however revealed the fragility of the relationship. Moscow’s decision to stop the engagement was caused by the declining ability of OPEC+ to affect the global oil market. By March 2020, Russia accepted that the era of high oil prices had ended, an assessment clearly reflected in the Russian state budget planning that is built on the assumption of prices floating in the range $50-60 per barrel (likely closer to the lower end) until 2036.37 Moscow was also convinced that oil prices would drop below $50 per barrel over the coming four years before returning to the range $50-60 per barrel. Russia’s leadership further sensed the growing influence of non-OPEC+ members on oil prices as well as of forthcoming structural changes in market fundamentals that neither Russia alone nor OPEC+ can control.38

The continuing deterioration of Russia’s economy and the lack of financial resources remain one of the main factors limiting Moscow’s capacities to expand its presence in the region

In addition, Russia is nearing a psychological threshold in 2021-2022 when its oil output is expected to start falling from the current output of 11.4 million barrels per day to ultimately 6.3 million barrels per day in 2036.39 As part of its preparation, Russia has begun to look into the development of new oil-production projects, something that is however not possible under existing OPEC+ production limitations. Russia was thus tempted to adopt an ‘all to the market’ strategy to maximize exports and increase income while its oil output is still high. Businesses and politicians have been calling upon the Kremlin to further expand oil exports and had started to dub 2020 ‘Sechin’s year,’ referring to the fact that the chief executive of Rosneft, Igor Sechin, had come out strongly against the OPEC+ limits with his calls for Russia to leave the structure being heard by the Kremlin. At the same time, the Kremlin decided out of necessity to decrease the state budget’s dependency on oil in turn reflecting a degree of pessimism about the ability to maintain current oil output. Expected low prices, high upfront costs for the majority of new oil fields, and the lack of technologies and funds make one-third of Russian oil reserves unprofitable. Under these circumstances, the share of budget revenue from oil was expected to fall making Russia’s engagement with OPEC+ less important for its economy.

However, Moscow appears to have underestimated the potential consequences of its withdrawal from OPEC+. The Kremlin either expected that its move would scare other participants to accept Russia’s demands not to deepen production cuts or assumed that the negative impact of the collapse of the existing arrangement would ultimately not be that dramatic. Russia’s initial expectations were based on the assumption that the 2020 annual oil price would stay in the $40-45 per barrel range with the possibility of only a temporary fall below the $40 per barrel threshold. Even with the decline of Asian energy demand as a result of the COVID-19 pandemic, there was still the expectation that prices would return to the $50-55 range in 2021 as oil demand in China and other Asian nations resumes.40 Instead, Russia was overtaken by events and quickly found itself in a full-fledged oil war. As the COVID-19 implications intensified and GCC countries, foremost Saudi Arabia, decided to expand oil production in an effort to gain market share, oil prices soon found themselves well below the $40 per barrel threshold with no sense of any immediate recovery. This scared the Kremlin and resulted in Minister Novak calling OPEC+ members to keep their oil output within the limits observed in January-February 2020 less than a week after the initial announcement of the Russian withdrawal from the consortium.41 The pressure on world energy markets ultimately resulted in a new production being renegotiated in April 2020.

The Russian decision to pull out of the OPEC+ was also determined by domestic political considerations. By 2020, the Russian authorities began preparations for the end of Putin’s fourth term in power in 2024 and the necessity to extend his stay. This changed the regime’s priorities from satisfying the needs of the general population to ensuring the sustainability of the Kremlin’s alliance with powerful tycoons, including those controlling oil productions that would, in the end, either approve the figure of Putin’s successor or a change in the constitution that would allow him to stay in power for two more terms. As stated above not all of these power brokers were happy with the existing OPEC+ arrangement. In February 2020, Igor Sechin and Aleksandr Dyukov, the head of Gazprom Neft, voiced their clear resistance to further production cuts under the OPEC+ as this would go against their own development plans by limiting expected income.42

Russia’s economic relations with the GCC states have probably reached the maximum of their capacities with little chance to further improve their quality. Moscow is weak economically, which in turn, weakens its political leverages of influence

In general, Russia is still defining its strategy on how to deal with the consequences of the shale revolution and the beginning of the global energy transition for the oil and gas markets. Alternatives consist of either losing a share of the oil market but sustaining high oil prices by limiting output with other members of the OPEC+ agreement or fighting for market share at the expense of low oil prices. None of these options is ideal. It is important to keep in mind that Moscow’s participation in the OPEC+ was restored by external circumstances as the Kremlin could not foresee the depth of the negative impact of the COVID-19 on global oil demand. Yet, this also means that, following a stabilization of oil markets, Russian oil producers could try to leave the OPEC+ again.

Challenges for Russia - GCC Economic Relations

Yet, Moscow’s capacities to develop economic relations with the GCC have their natural limits. The continuing deterioration of Russia’s economy and the lack of financial resources remain one of the main factors limiting Moscow’s capacities to expand its presence in the region. The COVID-19 pandemic will further hit the Russian economy, seriously shrinking the volume of available resources. Growing technological backwardness is making Russia less appealing to Middle Eastern investors and limits the range of products it can trade. As argued by some experts, the low quality of equipment produced by Novomet became one of the reasons behind the Saudi decision to cancel the deal on the purchase of Novomet shares.43 The passive behavior of the Russian business community and the large share of the black market in the country’s economy additionally slows down the development of Moscow’s economic dialogue with the Middle East.

During the last several years, the Kremlin has tried hard to draw the attention of the GCC States to numerous promising investment projects in Russia. Yet, these attempts were in most cases unsuccessful or, have not yet brought results. The exchange of business delegations between Russia, on the one hand, and the GCC, on the other, is very active and accompanied by loud statements by officials from both sides on plans to invest billions of dollars in the Russian economy. However, when it comes to Russia, it is also market principles and not always political imperatives that determine the final decision of the GCC business community to move forward.

These principles underline that Russian projects, as well as the overall business environment, remain questionable and that other profitable alternatives exist in comparison. In 2017-2019, Saudi Aramco demonstrated interest in buying a share in the Arctic LNG-2 project in Russia, but, in the end, decided not to do this.44 One of the key reasons for the Saudi side to invest in the LNG industry is to get access to relevant technologies that could support Riyadh’s intentions to become an important player in the market of LNG supplies. However, Russia is at this stage developing its own technologies for natural gas liquefaction, meaning that Saudi investment would go into such development and not into accessing already existing technology. In addition, Saudi Arabia would also have to ensure that sanctions currently in place against Russia will not hamper and delay the development itself. Participation in, for example, U.S. LNG projects provide access to a more developed technological base with the result that Saudi Aramco chose to invest in the United States and openly pointed out to the Russian firm Novatek that there are more interesting, profitable and less risky projects and that in order to re-consider the Russian side would have to significantly revise its financial demands with regard to the purchase of the project shares. 45

Conclusion: Thinking about the Prospects for Cooperation

Russia’s economic relations with the GCC states have probably reached the maximum of their capacities with little chance to further improve their quality. Moscow is weak economically, which in turn, weakens its political leverages of influence. Nevertheless, limited chances for the qualitative evolution of Russia’s relations with the Gulf do not mean that there are no options for the further exploitation of those opportunities these ties provide at the current level.

Existing innate problems of Russia’s relations with the GCC might slowdown their development or even prevent them from coming to a new level

First of all, Moscow will definitely be interested in the exchange of information and coordination of efforts in the hydrocarbon markets. Moreover, the work here can be carried out at several levels at once (i) through the bilateral contacts at the government level; (ii) by broadening contacts between the Gulf companies and Russian business (Gazprom, Rosneft, Lukoil, and Novatek are clearly demonstrating interest in having closer contacts with the GCC); (iii) through the interaction within the international and regional organizations such as OPEC and the Gas Exporting Countries Forum (GECF).

Secondly, there are still options for the development of investment cooperation. Indeed, international sanctions and Russia’s economic issues might make the funding of large-scale projects risky and unappealing. Yet, apart from investments into Russia’s oil, gas and petrochemical sector, the GCC countries can continue their practice of funding local and regional infrastructural projects. These may not be as significant in terms of investment volumes and returns as the federal projects, but assistance to Russian regions will fully justify itself in terms of strengthening the Gulf influence in Russia and further changing the attitude of the Russian elites in favor of the GCC member states. Investments in local infrastructure are not usually affected by the anti-Russian sanctions. They also do not imply huge administrative costs and there is no big time gap between the discussion of these projects with the Russian authorities and their implementation. Meanwhile, the participation of foreign investors in large projects can be additionally hampered by Russia’s internal clan struggles and never-ending concerns by Russia’s security services about the vulnerability of national security.

Third, Russia might represent certain interests within the framework of the UAE and Qatar humanitarian diplomacy. GCC assistance to the development of various social projects in Russia will be very well received by the Russian authorities. At the same time, Russia will be interested in co-funding such projects in the post-Soviet republics if this is to bring additional points to Moscow in the eyes of the local elites. However, both in the case of investment and humanitarian cooperation, it is necessary to follow the principle of permanence. As demonstrated by the Emirati, Saudi and Qatari experience of investments in Russia, large but one-time investments are bringing less economic and political gains than protracted investments in smaller projects.

All in all, existing innate problems of Russia’s relations with the GCC might slowdown their development or even prevent them from coming to a new level. Yet, it does not mean either the absence of potential for further cooperation or that this potential should not be explored.

Endnotes

1. Authors such as Mark Katz, Vitaly Naumkin, Samuel Ramani, Theodore Karasik, Nicole Grajewski, Anna Borshchevskaya, Eugene Rumer, John Parker, Leonid Issaev, Stephen Blank, Aleksandr Shumilin, Dmitry Trenin, Yuri Barmin, Irina Zvyagelskaya, and Maxim Suchkov should definitely be followed. Among the most recent publications, collective monograph Russia in the Middle East, (Washington: Jamestown Foundation, 2018) edited by Stephen Blank and Theodore Karasik whose list of contributors includes a number of above-mentioned authors and a long-read Russia in the Middle East: Jack of all Trades, Master of None, (Washington: CEIP, 2019) by Eugene Rumer deserve special attention as, probably, the most comprehensive.

2. Mark Katz, Support Opposing Sides Simultaneously: Russia’s Approach to the Gulf and the Middle East, (Doha: Al Jazeera Center for Studies, 2018); Samuel Ramani, “Russia and the UAE: An Ideational Partnership”, The Middle East Policy, Vol. 27, No. 1 (2020); Alexander Shumilin and Inna Shumilina, “Russia as a Gravity Pole of the GCC’s New Foreign Policy Pragmatism,” The International Spectator, Vol. 52, No. 2 (2017); Li-Chen Sim, “Russia and the UAE Are Now Strategic Partners: What’s Next?,” LobeLog, (June 7, 2018), retrieved July 5, 2020, from https://lobelog.com/russia-and-the-uaeare-now-strategic-partners-whats-next/.

3. Such as, Eugene Rumer, Russia in the Middle East: Jack of all Trades, Master of None, (Washington: CEIP, 2019).

4. Samuel Ramani, “Russia’s Strategic Balancing Act in Yemen,” The Arab Gulf States Institute in Washington, (May 1, 2019), retrieved July 5, 2020 from https://agsiw.org/russias-strategic-balancing-act-in-yemen/.

5. Mazin Almaqbali and Vladimir Ivanov, “Russia’s Relations with Gulf States and Their Effect on Regional Balance in the Middle East,” RUDN Journal of Political Science, No. 2 (2018), pp. 536-547; Rumer, Russia in the Middle East; Becca Wasser, The Limits of Russian Strategy in the Middle East, (Washington: RAND, 2019).

6. Katz, Better than before: Comparing Moscow’s Cold War.

7. Ramani, “Russia’s Strategic Balancing Act in Yemen.”

8. Leonid Issaev and Alisa Shishkina, “Russia in the Middle East: In Search of Its Place,” in Wolfgang Muhlberger (ed.), Political Narratives in the Middle East and North Africa, (London: Springer, 2020).

9. Michael Bradshaw and Richard Connolly, “Preparing for the New Oil Order? Saudi Arabia and Russia,” Energy Strategy Reviews, 26 (2019).

10. Bradshaw and Connolly, “Preparing for the New Oil Order?”

11. Li-Chen Sim, “Moscow’s New Strategy in the Gulf,” About Energy, (August 27, 2019), retrieved July 5, 2020, from https://www.aboutenergy.com/en_IT/topics/topic-li-chen-eng.shtml.

12. Theodore Karasik, “Russia’s Financial Tactics in the Middle East,” in Theodere Karasik and Stephen Blank (eds.), Russia in the Middle East, (Washington: Jamestown Foundation, 2018), pp. 240- 264.

13. “The Statistics of the Russian Federal Customs Service,” retrieved July 5, 2020, from russian-trade.com.

14. “The Statistics of the Russian Federal Customs Service.”

15. Aleksey Nikolskiy, “Blizhnii Vostok Stanovitsya Krupneishim Rinkom dlya Rossiskikh Vooruzhenii [The Middle East Is Becoming the Largest Market for Russian Arms Sales],” Vedomosti, (February 18, 2019), retrieved July 29, 2020, from https://www.vedomosti.ru/politics/articles/2019/02/18/794445-blizhnii-vostok-stanovitsya-krupneishim-rinkom-vooruzhenii.

16. Andrey Frolov, “VTS Rossii so Stranami Blizhnego Vostoka i Severnoy Afriki: Sostoyanie i Perspektivy’ [Russia’s Military-Industrial Cooperation with the Countries of the Middle East: State and Prospects],” Noviy Oboronniy Zakaz, No. 4 (2019).

17. “The Statistics of the Russian Federal Customs Service.”

18. Frolov, “VTS Rossii so Stranami Blizhnego Vostoka i Severnoy Afriki: Sostoyanie i Perspektivy.”

19. “Pokupateley s Blizhnego Vostoka Zainteresovalo Rossiskoye Oruzhiye na IDEX [Buyers from the Middle East Demonstrated Interest in Russian Weapons at IDEX],” RIA Novosti, (February 22, 2017), retrieved July 29, 2020, from https://ria.ru/20170222/1488612608.html.

20. Aleksandra Galaktionova, Jirgala Jorgiyeva, and Ekaterina Yakunina, Investitcii v Infrastrukturu. Arabskiy Mir [Investments in Infrastructure: The Arab World], (Moscow: InfraOne, 2018), pp. 17- 20.

21. Margarita Shpilevskaya, “Glava RFPI: Sotrudnichestvo s Saudovskoy Araviey i OAE na Bespretcedentno Vysokom Urovne [Head of the RDIF: Cooperation with Saudi Arabia and the UAE Has Reached the Unprecedented Level] ,” TASS, (October 28, 2019), retrieved July 29, 2020, from https://tass.ru/interviews/7050882.

22. “Qatari Investments in Russia around $13bn, Says Official,” Gulf Times, (August 5, 2019), retrieved July 29, 2020, from https://www.gulf-times.com/story/638331/Qatari-investments-in-Russia-around-13bn-says-official.

23. Galaktionova, Jorgiyeva, and Yakunina, Investitcii v Infrastrukturu, 17-20.

24. Shpilevskaya, “Glava RFPI: Sotrudnichestvo s Saudovskoy Araviey i OAE na Bespretcedentno Vysokom Urovne”; “Emirates Giant DP World Seeks 49% Stake in Vladivostok Operator Fesco,” Russia Business Today, (January 27, 2020), retrieved July 29, 2020 from https://russiabusinesstoday.com/economy/emirates-giant-dp-world-seeks-49-stake-in-vladivostok-operator-fesco/.

25. Shpilevskaya, “Glava RFPI.”

26. See the Facebook Page of the Zayed Fund office in Chechnya retrieved from https://www.facebook.com/zayedfund/.

27. Madina Kalimullina, “Islamic Finance in Russia: A Market Review and the Legal Environment,” Global Finance Journal, 46 (2020).

28. Kiril Dmitriev, “RF i Saudovskaya Araviya Prodolzhat Razvivat Investpartnerstvo [Russia and Saudi Arabia Will Continue Investment Cooperation],” RDIF, (March 11, 2020), retrieved July 29, 2020, from https://rdif.ru/fullNews/4921/.

29. Shpilevskaya, “Glava RFPI.”

30. “Sechin Peredal Emiru Katara Poslaniye ot Putina [Sechin Delivered Putin’s Message to the Emir of Qatar],” Kommersant, (March 29, 2019), retrieved July 29, 2020, from https://www.kommersant.ru/doc/3925857 https://iz.ru/726221/eldar-kasaev/poleznye-partnery.

31. “Gazprom Neft i Mubadala Petroleum Razvivayut Tekhnologicheskoye Sotrudnichestvo [Gazprom Neft and Mubadala Petroleum Are Developing Technological Cooperation],” Gazprom Neft, (February 12, 2020), retrieved July 29, 2020, from https://www.gazprom-neft.ru/press-center/news/gazprom_neft_i_mubadala_petroleum_razvivayut_tekhnologicheskoe_sotrudnichestvo/.

32. “Gazprom Neft i Mubadala Petroleum Razvivayut Tekhnologicheskoye Sotrudnichestvo.”

33. Sergey Pravosudov, “Rossya Otkazalas Vstupit v OPEK [Russia Refused to Join the OPEC],” Nezavisimaya Gazeta, (September 28, 2020), retrieved from https://www.ng.ru/politics/2000-09-28/3_opek.html.

34. “Putin: Rossiya Tcenit Vklad Korolya Saudovskoy Aravii v Sotrudnichestvo [Putin: Russia Appreciates the Saudi King Input in Cooperation],” RIA Novosti, (October 14, 2019), retrieved from July 29, 2020, from https://ria.ru/20191014/1559769929.html.

35. The text of the Charter can be retrieved from https://minenergo.gov.ru/node/15216.

36. “Novak i MEA Otcenili Dokhody Rossii ot Sdelki OPEK v 2019 godu [Novak and IEA Estimated Russia’s Incomes from the OPEC Deal in 2019] ,” InvestFuture, (November 15, 2019), retrieved July 29, 2020, from https://investfuture.ru/news/id/novak-i-mea-ocenili-dohody-rossii-ot-sdelki-opek-v-2019-godu.

37. “Budgetniy Prognoz Rossiyskoy Federatcii na Period do 2036 goda [Budget Forecast of the Russian Federation till 2036],” Russian Ministry of Finance, (2019) retrieved July 5, 2020, from https://www.minfin.ru/common/upload/library/2019/04/main/Budzhetnyy_prognoz_2036.pdf.

38. “Budgetniy Prognoz Rossiyskoy Federatcii na Period do 2036 goda.”

39. “Chernoye Uzhe ne Zoloto [Black Is no Longer Gold],” Noviye Izvestiya, (October 4, 2019), retrieved July 5, 2020, from https://newizv.ru/article/general/04-10-2019/chernoe-uzhe-ne-zoloto-neft-stanovitsya-nerentabelnoy-ne-tolko-v-rossii-no-i-v-ssha.

40. “Chernoye Uzhe ne Zoloto.”

41. “Rossiya Vistupayet za Sokhraneniye Dobychi Nefti na Urovne I Kvartala’ [Russia Calls upon the Keeping of Oil Production at the Level of the 1 Quarter],” RNS, (March 11, 2020), retrieved July 5, 2020, from https://rns.online/energy/Rossiya-vistupaet-za-sohranenie-dobichi-nefti-na-urovne-I-kvartala--2020-03-11/?fbclid=IwAR1lwoJK_ZurL1xMk-ok-m-bDa-8x1LjX1L6fgeszKWUvTRVDjw7dgWhAGk.

42. Konstantin Simonov, “Protivniki Sdelki s OPEK vo Glave s Sechinym Usilili Pozitcii [The Opponents of the OPEC Agreement with Sechin in the Lead Strengthened their Positions],” Forbes, (May 15, 2019), retrieved July 5, 2020, from https://www.forbes.ru/biznes/376003-protivniki-sdelki-s-opek-vo-glave-s-sechinym-usilili-pozicii-prislushaetsya-li-k-nim.

43. Dmitri Kozlov, “Korolyam Tut ne Mesto” “[There Is no Place for Kings],” Kommersant, (March 16, 2020), retrieved July 5, 2020, from https://www.kommersant.ru/doc/4290336. According to other explanations, the key role was played by Sechin, a vocal critic of the Saudi-Russian rapprochement who made Novomet exit the deal.

44. “Arktik SPG-2 Mozhet Stat Chastyu Gazovoy Strategii Saudi Aramco [Arctic LNG-2 Can Become a Part of Saudi Aramco’s Gas Strategy],” Znak, (February 14, 2018), retrieved May 18, 2019, from https://www.znak.com/2018-02-14/arktik_spg_2_mozhet_stat_chastyu_gazovoy_strategii_saudi_aramco.

45. Kozlov, “Korolyam Tut ne Mesto.”